Yield Curve Control Is Turning Australia Into a Carry Trade Haven

Thanks to Australia’s yield-curve control policy, its bonds have the steepest curve among major sovereign markets.

(Bloomberg) -- While bets on steepening yield curves are growing in popularity, money can also be made in countries that already have one and that’s drawing investors Down Under.

Thanks to Australia’s yield-curve control policy, its bonds have the steepest curve among major sovereign markets, according to two- and 10-year note data compiled by Bloomberg. Investors can exploit that difference by borrowing at lower shorter-term rates and investing higher up the curve.

For example, a trader could employ a “carry-and-roll” strategy, borrowing over a short time period at relatively cheaper rates and putting the proceeds into longer-term higher-yielding bonds. Players then earn “carry” from the bond’s coupon and “roll” from its capital appreciation as the note slides down the curve toward maturity. The steeper the yield curve the greater the opportunity.

“What I have learned from Australia is that a yield curve control policy targeting short-term yields can steepen the curve from time to time and make the debt attractive,” said Akira Takei, a Tokyo-based global fixed-income money manager at Asset Management One. “Investing in a bond market where the curve is steep like Australia generally turns out to be a winning bet.”

The spread between two- and 10-year Australian bonds was 60 basis points Tuesday, compared to around 49 basis points in the U.S. and just 18 basis points in Japan. A carry-and-roll strategy works best if rates stay little changed, and differs from so-called curve steepener bets where traders expect longer-dated yields to continue to rise.

Australia’s steeper curve is a result of two factors. The first is increased bond issuance to fund the government’s fiscal stimulus, which exerts upward pressure on longer-dated bond yields. The second is the Reserve Bank of Australia’s yield curve control policy that keeps three-year yields anchored at 0.25%.

Japanese investors in particular are jumping at the opportunities in the Australian market. Funds from the Asian nation bought $6 billion of Aussie debt in May, the most in data going back to 2005, according to the Ministry of Finance’s balance-of-payments report earlier this month.

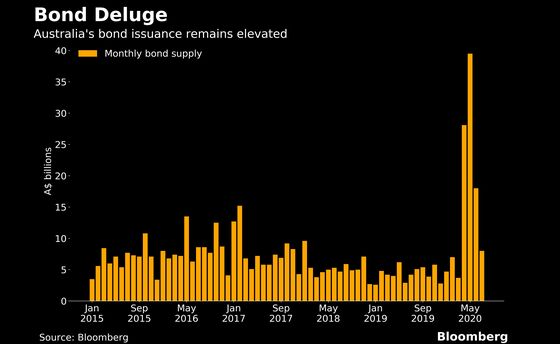

Like other major markets, the Australian government has ramped up bond sales to fund record stimulus measures to cope with the coronavirus pandemic. It already had two record-breaking debt sales this year. On Tuesday, it sold A$17 billion ($12 billion) of bonds maturing in 2025, which saw demand rise from hedge funds and central banks.

“The relative steepness of the ACGB curve has attracted strong investor demand,” strategists at Australia & New Zealand Banking Group Ltd. including David Plank wrote Wednesday. That should limit the upside in the nation’s 10-year yield relative to U.S. Treasuries, they said.

©2020 Bloomberg L.P.