(Bloomberg Opinion) -- China’s $13 trillion bond market seems calmer this year, with fewer defaults than 2018. Underneath the surface, though, is a churning current that threatens to swallow investors who aren’t careful.

The case of Xiwang Group Co. is one such cautionary tale. Just days ago, this distressed industrial conglomerate in the northeast province of Shandong thought it could borrow for peanuts. The company, whose business operations span corn-oil processing to steel manufacturing, tried to raise 450 million yuan ($63.5 million) at a coupon range of 7.5% to 8.5%. The deal was scrapped Wednesday. Meanwhile, the company warned in a filing of “uncertainty” about its ability to repay a short-term 1 billion yuan note due Oct. 24.

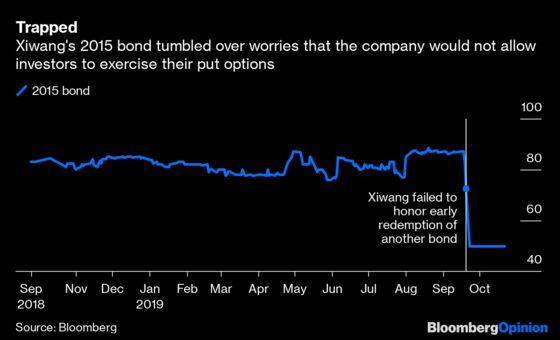

It wasn’t supposed to happen this way. The company had told institutional investors who’d bought into a 2015 bond, which has a put option due in December, that it didn’t have the money to repay the principal as expected. Instead of forcing Xiwang to renege on its promises, the company reasoned, creditors would be better off if it rolled over the debt to a new bond instead. After all, recovery rates from struggling private businesses have been poor. This new offering seemed like a clever maneuver that would let Xiwang have it both ways.

That hardball backfired. The new offering diverged too deeply from the prevailing market rate: Xiwang’s 2015 issue, which pays a 7.4% coupon, last traded at 50 cents on a dollar.

There could be a silver lining, however: It seems investors are holding out hope that Xiwang, a private enterprise, will get a government bailout. Shandong province has a history of helping out its prized non-state sector, which accounts for more than half of its gross domestic product. As recently as last week, LVMH wannabe Shandong Ruyi Technology Group Co. got a partial rescue from a local government financing vehicle. In the third quarter, Xiwang received 3 billion yuan of cash from a provincial government fund that aims to help private enterprises with liquidity issues.

Xiwang, with about 50 billion yuan in assets, would have to repay public investorsas much as 7.7 billion yuan over the next year if its creditors exercise their put options. The firm sat on just 1.4 billion yuan of cash as of June, and generates about 4 billion yuan of operating cash flow a year. Meanwhile, its most liquid assets have already been pledged out for loans, including a 50% stake in Shenzhen-listed Xiwang Foodstuffs Co. and 74% of Hong Kong-listed Xiwang Property Holdings Co. So are billions of yuan worth of land, factories and equipment.

Some of Xiwang’s trouble stems from the fact that it frequently uses cross-guarantees, a common practice among Chinese state and private companies to secure more credit. The trouble is, things can unravel quickly when one of those guarantors itself gets stuck, as some of Xiwang’s riskier partners have. But the company’s track record of good social citizenship could mean Xiwang can curry enough favors to buy itself out of any mess.

Back in 2017, nudged by the local government, Xiwang became the trustee of aluminum maker Qixing Group Co. — one of its cross-guarantee partners — which went into bankruptcy after reneging on 7 billion yuan of obligations. Xiwang lost about 250 million yuan along the way. As of March, it guaranteed 624 million yuan of credit, which is now overdue, for the sole state-owned power supplier of Zouping county, where Xiwang is headquartered. So it isn’t a stretch to think those favors will be returned with a bailout. Even with the Qixing bankruptcy, another government affiliate picked up the bulk of what the company owed in 2018.

But time is of the essence: Xiwang is already on the verge of throwing in the towel. The company, which was widely expected to redeem another bond, spooked the market last month when it didn’t promptly disclose with stock regulators its intent to accept investor requests to exercise their put option. Xiwang ended up repaying retail investors 300 million yuan one day late. As for institutional investors, the only concession they got from the company was more frequent put options. Such shenanigans only reinforces what traders now term the “Shandong implicit guarantee,” or the expectation that companies there will honor their obligations to retail clients first.

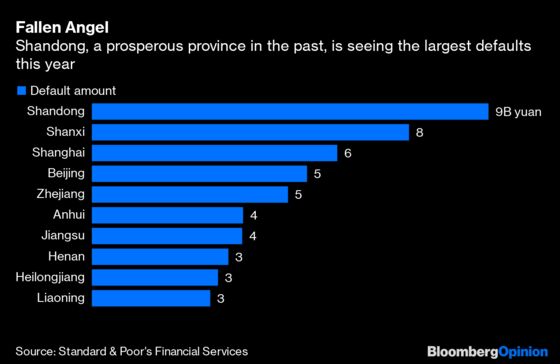

But even if Shandong is willing to help, is it able? Already the hitherto prosperous province has the largest number of defaults this year. The region was hit particularly hard by the U.S.-China trade war because of its reliance on the industrial sector.

China’s total number of new defaults comes in at 26 so far this year, compared with 38 in 2018, data compiled by Goldman Sachs Group Inc. show. But this number is deceptively low. Troubled China Inc. has taken to various creative tactics, such as side deals with institutional investors, to avoid the official default label. Xiwang, despite all its woes. still boasts an AA+ credit rating.

As Xiwang shows, there’s a big backlog of troubled companies staving off default with temporary solutions. The day of reckoning is coming.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.