Worst Isn’t Over for Chinese Bonds as Supply Surge Looms

Worst Isn’t Over for China Sovereign Bonds as Supply Surge Looms

(Bloomberg) --

A wall of maturing debt will soon add more strain to China’s sovereign-bond market, already under pressure from a global sell-off and rising inflation.

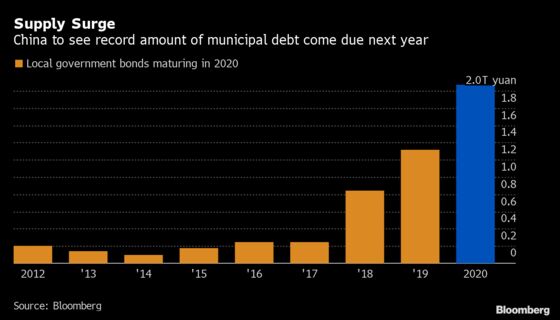

More than 2 trillion yuan ($283 billion) of local-government notes will mature in 2020, according to Bloomberg-compiled data -- a record and 58% more than this year’s level. This means fresh debt to refinance the borrowing could start hitting the market shortly. A report Tuesday said the southern province of Guangdong may sell notes as early as November.

The 10-year yield rose 3 basis points to 3.33% as of 3:48 p.m. local time. Futures on the debt fell 0.4% to the lowest in nearly five months while the cost on 12-month interest rate swaps jumped 5 basis points to 2.92%. The yield on China Development Bank’s three-year bonds due January 2022 rose 10 basis points to 3.25%.

China’s government bonds have been sliding for nearly two months, with selling momentum accelerating and the 10-year yield hitting the highest since May. A flood of new supply is likely to exacerbate the weakness, especially as inflation-adjusted yields are barely above zero -- a rarity for emerging markets.

“The large amount of supply that will be rolled over will weigh on China’s sovereign bonds,” said Ken Cheung, chief Asia FX strategist at Mizuho Bank Ltd. Also dimming the bull case for bonds year are eased recession fears at home and lower expectations of central bank stimulus, he added.

China will grant part of a special bonds quota in advance to ensure that the funds raised can be used early in the year, Deputy Finance Minister Xu Hongcai said in September. So-called special bonds have mostly been used for infrastructure spending, and the national limit could be raised from 2.15 trillion yuan.

The State Council, China’s cabinet, in June expanded the sectors that funds raised via the special bonds can be put toward. For 2020, they will include transport, energy, agriculture and forestry, vocational education and medical care. Overall fixed-asset investment has slowed this year amid pressure from the U.S. trade war.

| Read More: |

|---|

Beijing’s decision to avoid conducting aggressive stimulus measures -- even as the economy grows at the slowest pace since the early 1990s -- has spooked bond investors. The central bank has held off from adding liquidity this week, instead allowing large short-term cash injections to mature. That’s effectively drained 500 billion yuan from the financial system.

Some analysts said the central bank could instead use a targeted tool to inject one-year cash, which it refrained from doing Wednesday. Rising consumer prices, fueled by the surging cost of pork, are seen capping how much liquidity Beijing can provide without further stoking inflation.

China is rolling out more debt to help boost the spending needed to contain its economic slowdown. Sales of local-government notes could reach 5.5 trillion yuan in 2020, said Qi Sheng, an analyst at Zhongtai Securities Co. That amount would be 28% more than this year, data compiled by Bloomberg show.

“The snowball of Chinese local government debt will definitely get bigger and bigger,” Qi said.

To contact Bloomberg News staff for this story: Livia Yap in Shanghai at lyap14@bloomberg.net;Jing Zhao in Beijing at jzhao231@bloomberg.net

To contact the editors responsible for this story: Sofia Horta e Costa at shortaecosta@bloomberg.net, Kevin Kingsbury, Philip Glamann

©2019 Bloomberg L.P.

With assistance from Bloomberg