World’s Top Pension Fund Bet Big on Front End of Treasury Market

GPIF, which manages 150 trillion yen ($1.4 trillion), provided a detailed breakdown of its portfolio for the first time ever.

(Bloomberg) -- Japan’s Government Pension Investment Fund had billions of dollars in short-term U.S. Treasury debt when the pandemic hit early this year, leaving it with a pile of money to reinvest as the global recession dragged on.

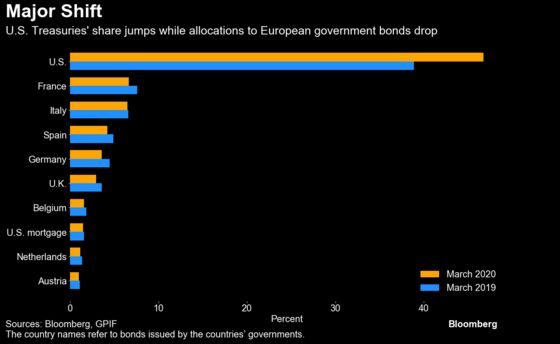

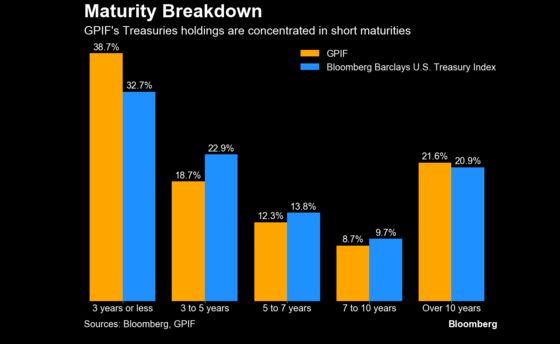

GPIF, as the world’s biggest pension fund is known, boosted its Treasuries holdings to almost 50% of its foreign bond portfolio in the year through March 31, with almost 40% of that amount concentrated in maturities of three years or less, a surprisingly high number for an institution that has to match long-term liabilities.

These figures come from a Bloomberg analysis of the more than 8,000 foreign debt securities that were divulged when GPIF, which manages 150 trillion yen ($1.4 trillion), provided a detailed breakdown of its portfolio for the first time ever.

With the release of such data not due again until next year, it’s difficult to know how GPIF changed its portfolio over recent months. But just as the fund was ahead of the massive influx of investors into money-market funds and short-term debt as the pandemic unfolded, it could also lead the way out.

While Treasuries found favor with the fund, the share of sovereign debt in the portfolio from France, Germany, Spain and the U.K. all dropped, according to Bloomberg’s analysis.

Strategists in Tokyo suggest the fund will wait for yields on American corporate bonds and government agency debt to rise before shifting some of the holdings.

“GPIF may be parking funds in Treasuries as a substitute for cash until it allocates them to other assets such as credit,” said Masahiko Loo, a fixed-income portfolio manager at AllianceBernstein Japan. “The fund is probably making itself more flexible with holdings from the shorter-end of the market.”

Popular Strategy

While GPIF hasn’t commented on the possibility of buying U.S. corporate debt, only saying it wants more foreign bonds to add to its $330 billion holdings, many Japanese life insurers have said credit is attractive given how sovereign yields have plunged.

Sitting in the short-end of the market has been a popular strategy with many, with money-market mutual funds growing to $4.6 trillion. Likewise, as rate-cuts and economic uncertainty led investors to hoard short-tenor debt and sell longer ones, the gap between 5- and 30-year Treasury yields widened by more than 60 basis points this year to the peak in June.

But, should the GPIF start to shift, it could set off a cascade of similar flows by other Japanese funds, some of the biggest buyers of overseas debt, which track its model.

The GPIF doesn’t comment on specific details about its activities related to its investment decisions, said Naori Honda, director and spokesperson at the fund.

Treasury Binge

The latest data show how GPIF has been on a Treasury-buying binge, raising its allocation to 46.8% of its foreign bond portfolio for the fiscal year ended March, up from 38.9% in the prior period.

Some 38.7% of its $152 billion investment in Treasuries is in maturities of three years or less. This is 6 percentage points higher than the weighting in the Bloomberg Barclays U.S. Treasury Index. The GPIF didn’t provide a comparable tenor breakdown for the fiscal year ended March 2019.

It is likely much of the increase in the holdings came while yields for two- and 10-year debt were both above 1.5%, before the dramatic rally in February and March propelled them to record lows.

The heavier flow into Treasuries came at the cost of GPIF’s European holdings. The proportion allocated to France, Italy, Spain, Germany, the U.K., Belgium, the Netherlands and Austria dropped to a combined 27.6% from 31.5%.

“High nominal yields may have been the key driver” for the increase in Treasuries holdings, said Prashant Newnaha, a senior strategist at TD Securities in Singapore. “Perhaps the GPIF was positive on the dollar, and expected trade-war frictions and risk-off sentiment to be supportive” of Treasuries, he said.

Treasuries, without currency-hedging costs, gave Japanese investors a 10% return for the 12 months ended March 31 -- the best performance since 2015, according to a Bloomberg index. Ten-year notes yielded an average of 1.83% in the U.S. during the period, compared with 1.56% in Italy and minus 0.02% in France.

Pressure may grow on the fund to change tack.

From late April, the most popular Wall Street Treasury trade has been a play on the widening Treasury yield gap, with the Federal Reserve anchoring short-end yields with near-zero rates and its bond purchases.

Fed Speculation

That strategy is getting unwound amid increasing speculation that the central bank will step up purchases of longer-dated bonds.

Still, what GPIF has articulated suggests it will continue to focus on foreign debt. Overseas bonds were the only major asset class to generate a positive return in the three months through March, when stocks led an 11% drop in the value of its total investments.

Foreign bonds without currency hedges comprised about 22% of GPIF’s investments on March 31, versus its target of 25%. That left it with about 4.3 trillion yen more to buy, according to calculations by Bloomberg, before accounting for market moves and new money in the past four months.

“Although our foreign bond holdings are below the policy allocation, it doesn’t mean we will rush to buy immediately,” GPIF President Masataka Miyazono said earlier this month. “We recognize diversification of foreign bond investment as an issue, but we will carefully consider our next step while closely watching the impact from the coronavirus, market and currency developments.”

The fund’s next investor update, for the quarter through June 30, is due in August.

©2020 Bloomberg L.P.