World's Best Market Shows Why Politics Matters: Taking Stock

World's Best Market Shows Why Politics Matters: Taking Stock

(Bloomberg) -- Well, this is something you haven’t heard in awhile: Greek political developments are buoying equities.

The nation’s stock index was already one of 2019’s top performers globally even before the European Union elections, but the crushing defeat of Alexis Tsipras’s populist party and prospect of a snap election has filled the rally with fresh fuel.

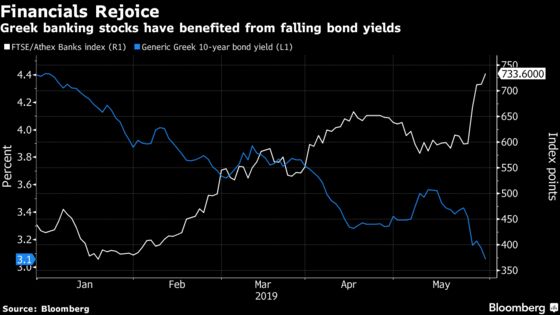

With the ASE Index surging the most in four years this week and bringing the year-to-date return to about 30% in dollar terms, Greece is proving a stark reminder of how much investor appetite for Europe hinges on political developments.

Greece is emerging as an unlikely poster child among European markets that are torn by major crises, such as Brexit and the Italian debt spat. Divided politics and the rise of populist parties are some of the key reasons international investors stay away from European equities, an asset that is the world’s most popular short trade.

“Greece, the first European country to succumb to populist pressure, also became the first to reject it, elevating investor optimism,” said George Lagarias, chief economist at Mazars Financial Planning Ltd. “Part of the move in stocks is the closure of the ‘populist discount,’ the discount investors required to hold Greek stocks under a populist government.”

Whereas European equity funds are suffering from almost non-stop outflows, fans of Greek assets include Goldman Sachs Group Inc. and Jefferies as strategists embrace the strongest economic expansion since 2007 and bet on political reform.

“A key driver of the good year-to-date returns in the Greek equity market is an impressive pickup in cyclical growth momentum in recent months, which has been sadly lacking elsewhere in the euro-zone,” said Jon Cunliffe, chief investment officer at Charles Stanley in London, which oversees about 24 billion pounds ($30 billion) in assets. “The presence of a large cash buffer, which should cover upcoming bond redemptions over the next two years, is also a supportive backdrop."

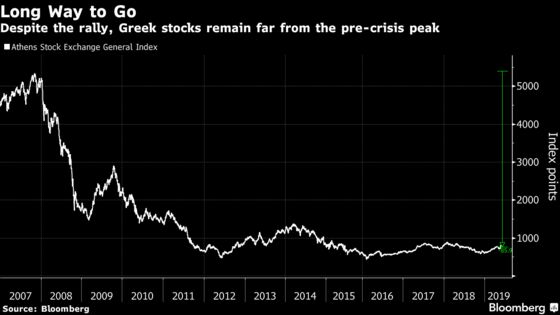

Despite this year’s formidable rally, the ASE Index remains about 85% below its 2007 peak. The challenges facing Greece are significant as the sovereign debt load stands at 181% of national income and the banking sector is still struggling with non-performing loans.

But at least in the short term, investors are focusing on the nation’s economic growth and optimism that a new government led by the center-right New Democracy party could bring market-friendly change. Such an administration would lead to a drop in bond yields, which would ease financial conditions and spur further economic growth, according to Goldman Sachs’s Silvia Ardagna.

“The new government is less likely to undo some structural reforms that have been undertaken in the past,” said Ardagna, who has a positive near-term outlook on Greece. “The risk of higher labor costs, less labor market flexibility and an erosion of wage competitiveness would diminish under a New Democracy-led government."

Ahead of the open, Euro Stoxx 50 futures are down 1%, tracking a drop in U.S. futures after President Donald Trump said he will place tariffs on all goods coming from Mexico.

SECTORS IN FOCUS TODAY:

- Watch stocks exposed to Mexico, including AB InBev: Trump vowed to impose a 5% tariff on Mexican goods, potentially rising as high as 25% by October.

- Watch trade-sensitive sectors overall: Trump and Chinese President Xi Jinping could potentially meet next month at the G20 Summit in Osaka, South China Morning Post reports, citing former governor of the People’s Bank of China Dai Xianglong. However, he said Beijing is not optimistic about achieving breakthroughs in trade talks.

- Watch stocks exposed to China: the country’s manufacturing sector slowed more than expected and further signs of stress in the labor market appeared.

- Watch Italian shares: La Repubblica reports that Finance Minister Giovanni Tria is set to issue a 10-page response to the EU letter on Italy’s finances on Friday as scheduled, in which he’ll say that Italy’s debt is manageable and sustainable.

COMMENT:

- “Financial markets price Fed rate cuts more aggressively amid strong trade headwinds,” Citi strategists write in a note. “This looks excessive relative to Citi’s base case of a patient Fed. We do not believe in a monetary policy insurance cut and fiscal policy insurance is most effective.”

COMPANY NEWS AND M&A:

- L&G to Sell General Insurance Ops to Allianz for GBP242m Base

- ArcelorMittal CFO Calls on EU to Solve China Steel Surplus

- Santander to Sell 50.01% of Global Seguros for EU82M: Expansion

- TSMC’s Liu Says Too Early to Assess Impact of U.S. Huawei Ban

- Credit Suisse CEO ‘Very Skeptical’ of Cross-Border M&A: L’Agefi

- Fiat Chrysler Requests Meeting With Nissan, MMC CEOs: Nikkei

- Corteva Says ‘Science Will Prevail’ for Bayer in Roundup Claims

- ERG Has No Interest in Buying Vedanta’s Zambia Assets

- Saipem Says Brazil Authority Opens Probe on 2011 Petrobras Pact

- Latecoere Is Open To Merger Of Equals, CEO Tells Le Figaro

- Wizz Air Full-Year Net Income 2.2% Above Estimates

- En+ Group 1Q Adjusted Ebitda $579 Mln Vs. $929 Mln Y/y

NOTES FROM THE SELL SIDE:

- Kingspan initiated at overweight with co. seen primed for margin boost following two years of cost pressure, while Rockwool set at underweight with pricing power likely to erode, Morgan Stanley says in note.

- Naturgy continues to offer an attractive valuation along with its commitment to a buyback, Macquarie says in note as it reiterates an outperform stance, the only positive rating remaining among analysts tracked by Bloomberg.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 374.5 (61.8% Fibo); 382.8 (50-DMA)

- Support at 368.7 (200-DMA); 365.5 (50% Fibo)

- RSI: 38.3

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,403 (61.8% Fibo); 3,408 (50-DMA)

- Support at 3,309 (50% Fibo); 3,269 (200-DMA)

- RSI: 40.4

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Axel Springer upgraded to hold at Berenberg

- Bunzl upgraded to buy at Goldman; PT 27 Pounds

- Equinor upgraded to buy at HSBC; Price Target 212 Kroner

- Mediaset upgraded to overweight at JPMorgan; PT 3.10 Euros

- Tatneft GDRs upgraded to hold at VTB Capital; PT $63

DOWNGRADES:

- None reported.

INITIATIONS:

- Boohoo rated new buy at Panmure Gordon; PT 3.08 Pounds

- Joules rated new buy at Panmure Gordon; PT 3.65 Pounds

- Kingspan rated new overweight at Morgan Stanley

- Rockwool rated new underweight at Morgan Stanley

- Superdry rated new sell at Panmure Gordon; PT 4.02 Pounds

- Ted Baker rated new hold at Panmure Gordon; PT 15.25 Pounds

MARKETS:

- MSCI Asia Pacific little changed, Nikkei 225 down 1.6%

- S&P 500 up 0.2%, Dow up 0.2%, Nasdaq up 0.3%

- Euro up 0.03% at $1.1132

- Dollar Index down 0.05% at 98.09

- Yen up 0.66% at 108.9

- Brent down 1.3% at $66/bbl, WTI down 1% to $56/bbl

- LME 3m Copper up 0.2% at $5865/MT

- Gold spot up 0.3% at $1293/oz

- US 10Yr yield down 4bps at 2.17%

MAIN MACRO DATA (all times CET):

- 10am: (IT) 1Q F GDP WDA YoY, est. 0.1%, prior 0.1%

- 10am: (IT) 1Q F GDP WDA QoQ, est. 0.2%, prior 0.2%

- 10am: (SP) March Current Account Balance, prior -2.8b

- 11am: (IT) May CPI EU Harmonized YoY, est. 0.9%, prior 1.1%

- 11am: (IT) May CPI EU Harmonized MoM, est. 0.2%, prior 0.6%

- 11am: (IT) May CPI NIC incl. tobacco YoY, est. 1.0%, prior 1.1%

- 11am: (IT) May CPI NIC incl. tobacco MoM, est. 0.2%, prior 0.2%

- 12pm: (IT) April PPI YoY, prior 3.7%

- 2pm: (GE) May CPI MoM, est. 0.3%, prior 1.0%

- 2pm: (GE) May CPI YoY, est. 1.6%, prior 2.0%

- 2pm: (GE) May CPI EU Harmonized MoM, est. 0.3%, prior 1.0%

- 2pm: (GE) May CPI EU Harmonized YoY, est. 1.4%, prior 2.1%

To contact the reporter on this story: Ksenia Galouchko in London at kgalouchko1@bloomberg.net

To contact the editors responsible for this story: Celeste Perri at cperri@bloomberg.net, Jon Menon, Blaise Robinson

©2019 Bloomberg L.P.