IMF Joins Powell and Lagarde Urging Governments to Keep Spending

The IMF calls for more public spending to complete the economic recovery from the coronavirus pandemic.

(Bloomberg) -- The International Monetary Fund said more public spending will be needed to complete the economic recovery from coronavirus, joining central bankers and finance leaders who are urging governments to set aside fears about mounting debt for now.

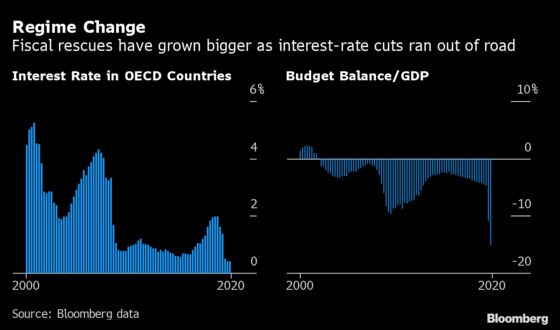

The Fund, historically a champion of budget restraint, on Wednesday published its most detailed study of the pandemic’s impact on public finances. It said global government debt will “make an unprecedented jump” this year, but it’s “not the most immediate risk. The near-term priority, instead, is to avoid premature withdrawal of support.”

That case was made with growing urgency by central bankers heading into this week’s IMF annual meeting. European Central Bank chief Christine Lagarde kicked off the online-only event by saying her biggest concern is that fiscal aid to workers and businesses may get phased out too abruptly.

A parade of Federal Reserve officials led by Chair Jerome Powell lined up last week to make the same argument with regard to the U.S., where talks on the next dose of pandemic stimulus have been deadlocked for months in Congress. Fed officials said their own tools, such as another round of bond-buying, won’t be as effective as government spending.

The message from the most powerful central banks is increasingly clear: there are limits to what monetary policy can do to help in the short run. Fiscal authorities -– who can borrow at rock-bottom interest rates, and possess tools better-suited to deliver a rapid and targeted boost -- will have to finish the job.

Powell and Lagarde are pushing back against the “myth of the omnipotent central bank” capable of fixing any problem in the economy, said Paul Donovan, global chief economist at UBS Wealth Management in London. “They can’t always solve it,” he said. “This is not a credit crunch. Cutting the cost of credit isn’t going to stimulate the economy.”

Governments already injected some $12 trillion of stimulus, according to IMF estimates, widening their budget deficits by an average 9 percentage points of GDP, and putting global public debt on track to pass 100% of GDP for the first time in 2022. Even so, the global rebound shows signs of losing momentum.

“You cannot prematurely withdraw any of this policy support, but you can only do it as circumstances improve,” Jose Vinals, chairman of Standard Chartered Plc, told Bloomberg TV. “A lot of fiscal support will still be needed, next year as well, and perhaps beyond that.”

What Bloomberg’s Economists Say...

“The key lesson for governments to learn from their handling of the first phase of the crisis -- be nimble, go all in.”

--Jamie Rush. Read the full GLOBAL INSIGHT

The fiscal rescue added 3.7 percentage points to global growth in 2020, according to JPMorgan Chase & Co. –- preventing the coronavirus rout from being roughly twice as bad. But JPMorgan economists expect that boost to turn into a drag next year, as stimulus gets choked off in a repeat of “policy missteps” that hobbled recoveries after the 2008 crash.

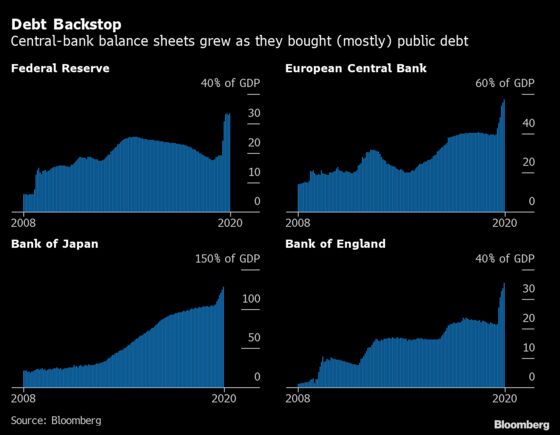

Central banks have supported public spending by buying up swaths of the debt that governments issue. They typically insist bond purchases are aimed at pushing inflation up to target levels, and don’t amount to monetary financing of budget deficits.

Read More: Bloomberg Economics on the hidden costs of monetary financing

Some warn that such policies could tie the hands of central banks when it’s time to raise interest rates –- and undercut their autonomy in the longer run.

Excessive government debt could mean “a central bank is de facto forced into making its decisions dependent on their impact on public finances,” Swiss National Bank President Thomas Jordan said last week.

Powell’s vocal engagement in the U.S. debate has reportedly drawn objections from several Republican senators opposed to bigger government outlays. It’s gotten even some supporters worried.

“I’m a little uncomfortable with how explicit the Fed has been in talking so bluntly about fiscal policy, even though I completely agree with what they’ve been saying,” Adam Posen -- a former BOE policy maker and now president of the Peterson Institute for International Economics -- said on a recent conference call.

The worry is that central bankers, who’ve often had to beat back political encroachments into their own monetary-policy turf, can put their independence at risk by straying outside it.

But Fed officials are driven by awareness that they’re short of ammunition, according to Bill Dudley, head of the New York Fed for a decade through 2018.

“They are reaching diminishing returns in terms of how their tools affect the economy,” said Dudley, now a scholar at Princeton. “It’s not that they can’t do more, but doing more wouldn’t do much. That’s precisely why they are talking about the need for fiscal policy.”

©2020 Bloomberg L.P.