World Is Stuck With the Dollar as the Reserve Currency

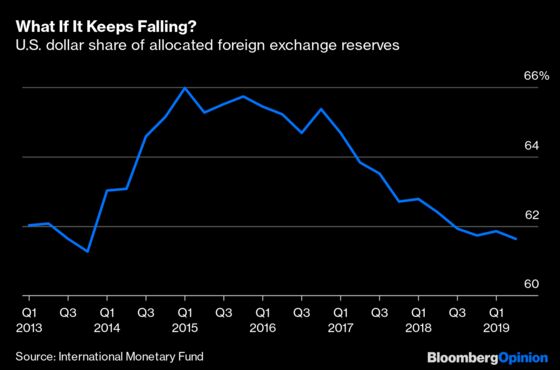

(Bloomberg Opinion) -- The U.S. dollar’s position as the world’s reserve currency might be weakening. In the last few years, the fraction of global reserves denominated in dollars has been inching down:

This follows a longer-term slide; at the turn of the century more than 70% of reserves were in dollars. Meanwhile, central banks are buying more gold, which could signal a lack of confidence in the dollar or the global monetary system more generally.

If the dollar loses its status as the reserve currency, it would be a major shift in the global economy the likes of which only happens once or twice a century. What happens then is anybody’s guess. The result could be chaos if it’s mismanaged; but if it’s handled well, the loss of the reserve currency could be healthy for the U.S. and the world. Indeed, given the U.S.’s waning economic dominance, the consequences of keeping the dollar as the sole reserve currency could be worse.

Because the dollar is the reserve currency, central banks around the world hold large amounts of dollar-denominated assets, mostly U.S. government bonds. They hold these reserves for a number of reasons: to maintain exchange-rate pegs, to insure against capital outflows and to facilitate international trade.

In the 19th century, countries held their reserves in gold or in British pounds (which were backed by gold). But after World War I the U.S. accumulated a large share of the world’s gold, meaning that holding dollars became the next best thing to holding the yellow metal itself. This arrangement was formalized in the Bretton Woods Agreement of 1944, when the dollar became the world’s official reserve currency and the U.S. promised to hold large amounts of gold. In the early 1970s, all connection between the dollar and gold was severed, but the U.S. remained the reserve currency of choice.

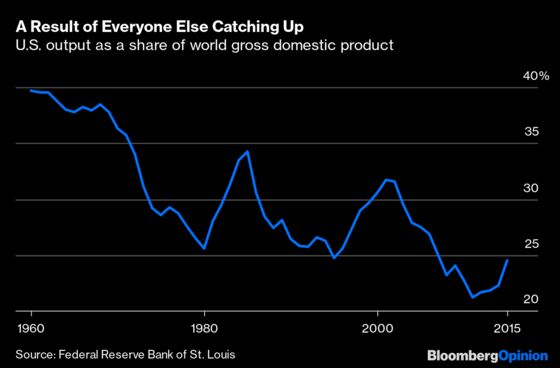

So why is dollar dominance slipping now? One long-term reason is the rise of the euro as an alternative reserve currency. A more recent factor is China’s increasing desire to diversify its foreign-exchange holdings to reduce its vulnerability to shifts in U.S. policy amid the trade war. But in the long term, the shrinking U.S. share of world economic output is the biggest threat to the dollar’s status. In 1960, the U.S. represented about 40% of the world economy but that has shrunk to less than a quarter:

As poorer nations catch up to rich ones, they face pressure to diversify and hold less of their growing reserve stockpiles in the currency of one decreasingly important country. It’s no coincidence that the 1980s, when the dollar dipped below half of global reserves, were a time when it looked as if the U.S. might be economically eclipsed by a rising Europe and Japan. That didn’t happen, but this time it might.

Economists have a hard time predicting the effects of a shift away from the dollar, because this is to some extent uncharted territory. One theory says that American borrowers would be forced to pay higher interest rates, causing the U.S. economy to suffer. Now, in order to acquire dollar reserves, foreigners essentially are forced to lend money to either the U.S. government or to U.S. companies. That demand for U.S. assets can bid down the price of loans within the U.S. But former Federal Reserve Chair Ben Bernanke argues that the U.S. no longer enjoys this so-called exorbitant privilege, noting that other countries’ real interest rates are almost as low. Bernanke could be wrong -- those other countries’ rates might be held down by their slow population growth, while the faster-growing U.S. benefits from reserve status instead. But in a world already awash in capital, the extra effect of reserve status is probably not that much.

Another theory says that the U.S. would benefit. Less demand for the dollar would cause the currency to depreciate; that would cut the price of U.S. exports and make imports more costly, reducing the trade deficit. That could ultimately lead to a more balanced global economy. It could even potentially help the U.S. become more competitive in manufacturing and other high-value export industries. But as Paul Krugman has noted, reserve-currency status might not be that big a factor because a number of other countries have run big trade deficits in recent decades as well.

In the end, a shift to a basket of world currencies might be the healthiest outcome. If the euro, yen and yuan were to join the dollar as international reserve currencies, it would mean a safer and more stable global economy. And it would enable the world’s major economies to compete on a more-or-less level playing field.

The problem is, the other major economies may be either unwilling or unable to help bring about that outcome. The euro-zone crisis cast doubt on that currency’s long-term dominance, while China shows no inclination to abandon capital controls and make the yuan fully convertible.

Reserve-holding countries may thus be stuck with the dollar. And the U.S. and its central bank may be stuck with the unenviable task of stabilizing a global economy that increasingly dwarfs it in size.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2019 Bloomberg L.P.