World Economy Faces New Fiscal Cliffs Amid Pressure for Spending

The world’s major economies poured money into the fight against the coronavirus slump but are now facing major choices.

(Bloomberg) -- The world’s major economies poured money into the fight against the coronavirus slump, and now they’re edging toward what may be a more complex policy choice: when and how to turn off the spigots.

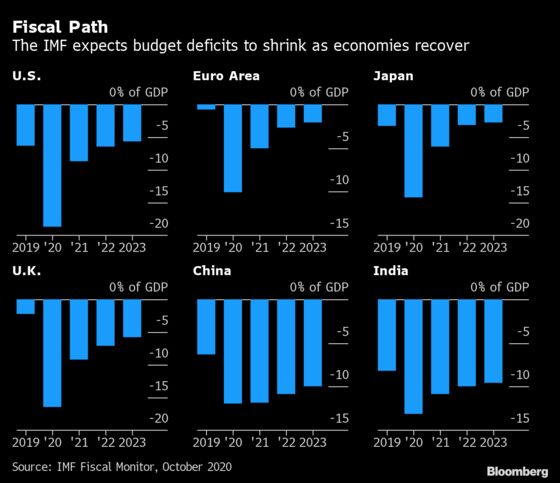

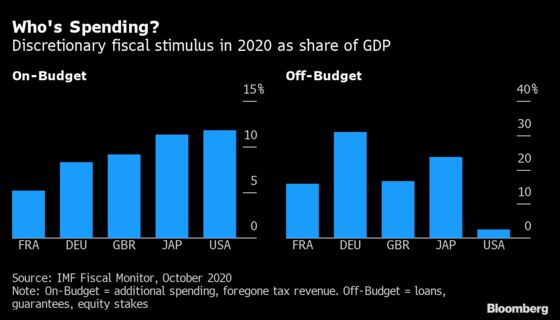

Governments have pledged some $12 trillion in spending this year, the International Monetary Fund estimates. While the fund says it’s too early to cut off the support, it warns record debt levels will eventually pose a challenge for policy makers.

The biggest economies are generally still in the spending camp, though budget deficits are forecast to start narrowing in 2021. Financial markets show no signs of balking, with borrowing costs at record lows almost everywhere. Yet, from some U.S. Republicans to sound-money advocates in Germany, debt concerns are starting to get voiced.

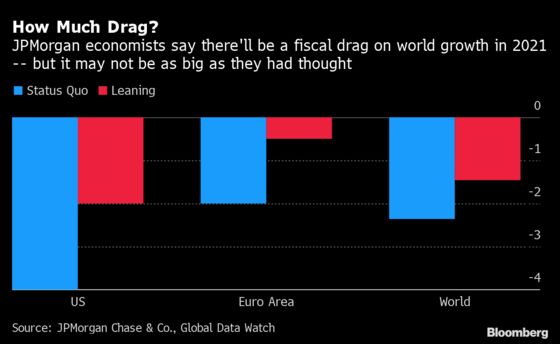

Some retrenchment looks inevitable. JPMorgan Chase & Co. says there’ll be a fiscal drag on the world economy next year -– but it may be less severe than expected, as momentum in the U.S. and Europe shifts toward extending aid.

Here’s a roundup of the fiscal outlook in the world’s biggest economies.

U.S.

Treasury Secretary Steven Mnuchin all but called time Wednesday on the months-long attempt to get a stimulus bill through Congress before the Nov. 3 presidential election. That means more support for the unemployed, small business and local authorities will likely have to wait until a new Congress is seated in January.

But expectations for a fiscal boost in 2021 have been growing along with Democratic challenger Joe Biden’s poll lead over President Donald Trump, and the likelihood that Democrats could sweep Congress too.

In that scenario, analysts say pandemic measures worth at least $2.2 trillion –- the amount Democrats have been pushing for -- would likely speed through the legislature. With a divided Congress like the present one, post-election stimulus will face a tougher path whoever wins the White House.

Euro Area

In Europe, the cliff-edge is still some way off -– with more budget support in the pipeline. National governments have extended early-pandemic programs, which offered generous loans, credit guarantees and wage support, and almost 1.8 trillion euros ($2.1 trillion) of joint European aid, a breakthrough for the bloc, is still waiting for disbursement.

Finance ministers have been told to keep policy expansionary in 2021, and to gradually replace emergency aid with longer-term measures that will help foster a low-carbon, digital economy. At the same time, a recent debt crisis hasn’t been forgotten, and Southern European countries, with high unemployment and debt even before the pandemic, know they’ll be under particular scrutiny from investors.

Japan

Japan’s government debt is on track to reach 266% of GDP this year, according to the IMF. But it hasn’t caused obvious problems for the economy, and new Prime Minister Yoshihide Suga says there’s no hard limit to how much he can borrow.

For now, Suga still has several trillion yen from a second extra budget to help support the pandemic economy. If the third-quarter rebound proves weaker than expected, speculation of another top-up will likely mushroom.

Before Suga took over, the government had already pushed back the cliff edge for its furlough program by three months, to the end of the year.

U.K.

The U.K. is already trying to scale back stimulus -– and finding it’s hard going, especially in the middle of a menacing new wave of coronavirus cases. Chancellor of the Exchequer Rishi Sunak has said early-pandemic spending levels aren’t sustainable, suggesting tax increases in the medium term.

The government said last month it would replace an across-the-board furlough program -– which supported more than 9 million jobs, at a cost of almost 40 billion pounds ($52 billion). The new, more targeted plan was expected to trigger a jump in unemployment.

Since then, Sunak has had to backpedal –- announcing additional wage support for workers at companies that are forced to shut down under new lockdown rules. The government has also deferred a deadline for businesses to apply for government-backed loans, and eased the terms for paying sales taxes.

China

Far from facing a fiscal cliff, China’s government is finding it hard to spend the trillions of yuan in fiscal firepower that it has set aside to bolster what is already a steady economic recovery. The IMF expects China to keep more of its fiscal stimulus in place over the next few years, compared with developed economies.

The government is selling a record amount of bonds this year to pay for stimulus. Much of that is at the local level, with 3.75 trillion yuan ($558 billion) earmarked to help regional authorities develop infrastructure.

India

Like China, India is forecast by the IMF to run relatively large budget deficits through 2023.

With its economy set to shrink by more than major emerging-market peers this year, the government is rolling out additional fiscal stimulus, more recently targeted at consumers, the bedrock of the economy. However, much of the support so far has fallen short of expectations and hasn’t given the economy the immediate boost it needs.

Fiscal room is also shrinking following a plunge in government revenue, forcing authorities to borrow a record amount this year. That surge in debt has pushed India’s credit rating closer to junk.

©2020 Bloomberg L.P.