Rate-Cut Fervor Sees Funds Favoring India's Short Bonds

Traders are boosting odds RBI will add to last week’s rate cut

(Bloomberg) -- India’s shorter-maturity bonds are set to outperform as traders boost the odds the central bank may cut interest rates again as soon as its April meeting.

That’s one of the reasons asset managers such as DHFL Pramerica Asset Managers Pvt. and HDFC Standard Life Insurance Co. favor the front-end of the yield curve. At the same time, escalating concern about Prime Minister Narendra Modi’s plan to sell almost $100 billion of debt is damping the appeal of longer maturities.

“The RBI rate cut and expectations of a further reduction will support the short end,” said Puneet Pal, deputy head of fixed income at DHFL Pramerica Asset Managers Pvt. in Mumbai, who favors debt due in four years or less. Meanwhile, the “demand-supply dynamics are likely to deteriorate going ahead, negating a big move down in long-term yields.”

The odds for more rate cuts is rising as inflation slows, with Reserve Bank of India Governor Shaktikanta Das pointing to the CPI to justify a surprise 25 basis-point reduction last week. Consumer-price growth fell to 2.05 percent in January, well below the RBI’s medium-term target of 4 percent.

Demand for shorter-maturity bonds is also higher amid concern of a repeat of the cash crunch seen last year following the default of Infrastructure Leasing & Financial Services Ltd. With liquidity tightening anyway toward the end of the fiscal year in March, another default may create a squeeze.

Default Fears

“The crisis that began after the IL&FS default in September is not over yet,” said Pankaj Pathak, fixed-income manager at Quantum Asset Management Co. in Mumbai. “The widening of spreads between corporate and sovereign yields reflects a lack of confidence in the credit market.”

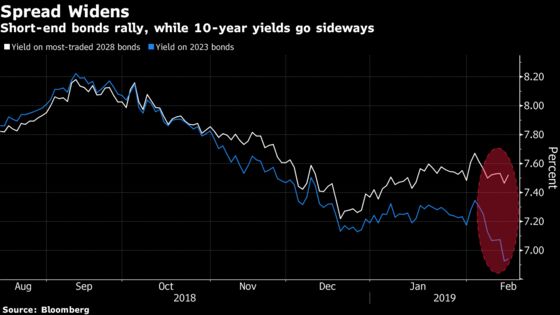

Funds switching to shorter maturities has seen yields on three-year bonds slide 24 basis points this month to 6.91 percent, while those on five-year notes have tumbled 29 basis points. At the same time, benchmark 10-year yields have climbed eight basis points to 7.36 percent.

Concern about a supply overhang for longer maturities increased after Modi’s government announced a record 7.1-trillion-rupee ($99.8 billion) borrowing program on Feb. 1. The sales are in addition to states issuing more paper to fund shortfalls resulting from the waiver of some farm loans.

Adding to the uncertainty are questions over the central bank’s plans to extend bond purchases. RBI will cut back buying to between 1.8 trillion rupees to 2 trillion rupees in the year starting April, from an estimated 2.7 trillion rupees so far this fiscal year, according to HSBC Holdings Plc.

“The market is concerned about the quantum and pace of bond purchases for next year,” said Lakshmi Iyer, head of fixed income at Kotak Mahindra Asset Management Co. in Mumbai. “That’s the reason why we’re not seeing as enthused a rally, especially in the 10-year benchmark.”

Here are some other comments from mutual fund and insurance managers:

Bajaj Allianz Life Insurance Co. (Sampath Reddy, chief investment officer)

- RBI policy has a dovish undertone, and is therefore positive for bonds. However, concerns remain on the fiscal front and higher bond supply. There could also be some pressure on yields if there’s a credit crunch or a further rise in oil prices

- Continue to prefer the shorter to medium term part of the yield curve

Kotak Mahindra Asset (Lakshmi Iyer, head of fixed income)

- Support in the form of an open-market operation in February and reasonable liquidity in the system is keeping short-bond yields supported. That’s going to be the anchor factor for yields because there’s not going to be supply in that segment

- In the government bond space, the sub-10 year segment is proving to be a better bet in this scenario

Quantum Asset (Pankaj Pathak, fixed-income fund manager)

- Continue to choose safety over credit, and liquidity over spreads and returns, for investing in 2019

- Long-term bond yields are expected to head higher. The front-end of the yield curve is the most attractive, namely 1-to-5 year bonds -- especially high-quality state-run companies that are trading at attractive spreads

HDFC Standard Life (Badrish Kulhalli, head of fixed income)

- Supply concerns will temper the decline of the sovereign yield curve. This fiscal year’s borrowing has been raised and next year’s is also large. We expect some steepening of the yield curve. Shorter-term bonds look attractive

DHFL Pramerica Asset (Puneet Pal, deputy head for fixed income)

- Credit spreads are expected to remain elevated with risk aversion likely to persist over the next 3 to 4 months

Canara Robeco Asset Management Co. (Avnish Jain, head of fixed income)

- We increased maturity of our duration funds as rates are expected to remain benign in the near term as RBI OMOs support yields

- We favor corporate over sovereign paper as spreads are attractive

- Investors are likely to get superior risk-adjusted returns from high-quality corporate bonds. They should look at short- and medium-duration corporate bond funds

Tata Asset Management (Murthy Nagarajan, head of fixed income)

- Expect short- and medium-term rates to come down 25 to 35 basis points and the long end rates to be range bound due to supply pressures

- The new 10-year bond yield is expected to trade 7.2%–7.5% in the coming months

- Corporate bonds spread is expected to widen due to risk aversion and continuous supply of paper

To contact the reporters on this story: Subhadip Sircar in Mumbai at ssircar3@bloomberg.net;Kartik Goyal in Mumbai at kgoyal@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Ravil Shirodkar, Nicholas Reynolds

©2019 Bloomberg L.P.