Bank Indonesia Should Get a Star for Good Behavior

(Bloomberg Opinion) -- Bank Indonesia put in the hard work. Time for at least some reward.

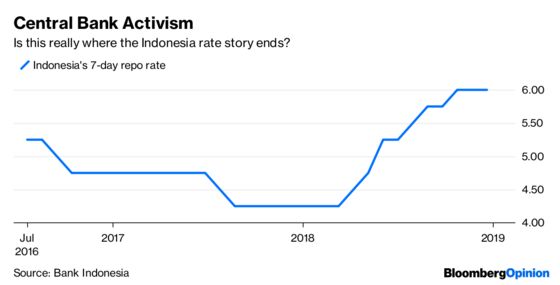

The work was a concerted, consistent and not-at-all hysterical approach to the slide in emerging markets in 2018. That meant six interest-rate increases to stem the rupiah's losses.

The message was transparent: Because the Federal Reserve was hiking every quarter, Indonesia needed to prevent a rout in the currency. There was a refreshing lack of ambiguity about whether BI was responding to the U.S. And it worked. The rupiah went from being one of the worst-performing emerging-market currencies in the third quarter of 2018 to one of the best by the end of the year.

The reward is likely to be a breather in rate hikes followed, just maybe, by cuts. The idea of axing rates is controversial, given the country's large current-account deficit and the notion that the rupiah will be vulnerable through 2019. And who knows whether the Fed is done or just opening the turret and peering about.

But think about it: If Bank Indonesia followed the Fed up despite anemic local inflation, wouldn't BI want some dividend for what's at least an intermission in America?

It might not even matter much if the Fed resumes at the end of the year. BI has been pretty nimble in the past and professed few qualms about changing tack. After all, Indonesia was reducing rates in 2017. The flip to tightening happened without too much egg on face.

To be sure, BI Governor Perry Warjiyo didn't sound much like a dove on Thursday. At a press briefing after the bank kept the benchmark rate at 6 percent, Warjiyo said the policy stance is still “hawkish.” Officials will be “preemptive and forward looking,” he added.

Yet a day earlier, Warjiyo went at least part way there. He told legislators that rates are just about at their peak. Once you start talking like that, it begs the question of what's next. With inflation low, and the external threat abating, the focus can turn more squarely on the domestic terrain.

In the face of the emerging-markets slump, Indonesia could have blamed shady cabals or so-called interest-rate lobbies, as Turkey did. It could have shot rates to 40 percent, as Argentina did. Or it could have made ill-timed comments about land distribution, as South Africa did. None of the above. Indonesia was a model student, earning praise from the International Monetary Fund. That's especially impressive given how disastrous the 1997-98 Asian financial crisis was for the country.

Some investors are paying attention. After tumbling past 15,000 per dollar, the rupiah has steadied, appreciating 3.6 percent in the final quarter of last year. It's added another 1.5 percent in the month to date. That’s some reward.

The beauty of couching your policy in terms of the Fed is it makes the rhetorical task of flipping that much easier. If your patron changes, you change.

Indonesia's economy hasn't suffered terribly from higher rates. As Bank of America Merrill Lynch notes, nominal bank lending rates actually fell a bit even as the official policy rate climbed. Gross domestic product has been pretty stable, growing around 5 percent the past few years. That pace will hold in 2019, BI forecasts.

For all the deference to the U.S., there are reasons closer to home to fret about the outlook. Like most countries in Asia, Indonesia counts China as far and away its biggest trading partner. The Middle Kingdom's economy is faltering and authorities are taking steps to shore up growth. And there’s that trade war.

BI has adjusted quickly before and can do so again. It wasn’t that long ago that an era of synchronous global monetary tightening was supposed to be upon us. Now that seems old hat.

What's a few months to Warjiyo, anyway?

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.