(Bloomberg Opinion) -- Don’t sweat the line-in-the-sand stuff. China's currency will probably weaken beyond 7 per U.S. dollar because economic conditions warrant it and the policy response encourages it. Even in China, fundamentals can't be ignored indefinitely.

Despite the parlor game among some market participants about the desire or ability of the People's Bank of China to keep the yuan above that level, it lacks long-term perspective: China’s growth is slowing and the exchange rate ultimately will reflect that.

As the economy slackens, officials have been easing fiscal and monetary policy. In these circumstances, it's natural for a currency to soften, as it has in the past year, with a drop approaching 8% versus the dollar. This cooling expansion reflects trends underway long before President Donald Trump took office.

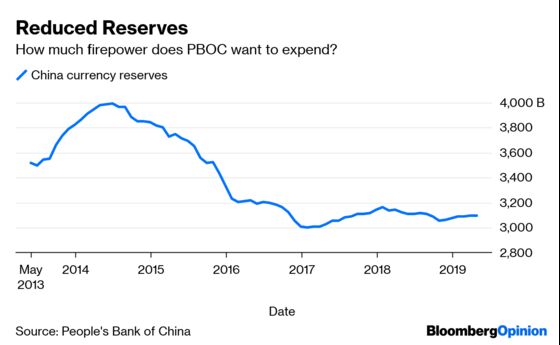

The era of double-digit growth is behind China: Its workforce is receding; and authorities have been trying to crack down on excess lending and the debt it racks up. Tariffs imposed by the White House are a further squeeze and sanctions against technology firms have been eroding confidence. I doubt the PBOC is much interested in expending too much more capital fighting this trend. Massaging it? Yes. Making sure things don't get wild and crazy? You bet.

Since China ended the yuan’s peg to the dollar in 2005, the currency has moved up and down, albeit with the central bank’s blessing. The exchange rate roughly responds to the same kind of economic and financial pressures as other major currencies. Sure, Beijing will nip and tuck monetary policy, prevent capital flight and prevent too much financial dislocation. Verbal broadsides against speculators of the kind delivered over the weekend by Guo Shuqing, the head of China’s banking and insurance regulator, are part of the tool kit. It will be about the velocity of the move below 7 and its timing, not the level itself.

This isn't to trivialize the issues at stake. The Chinese state plays a much bigger role in commerce and markets than in Europe or Japan. A freely traded yuan, in the manner of the euro or yen, is a pipe dream for now. (Even for these currencies, big, round numbers have come and gone. In Japan, 100 yen per dollar was once the line in the sand, and I remember when $1.20 per euro, and even $1.40, was a big deal.)

Fretting about how Trump might respond is also fruitless: China will get abuse whatever it does. Being branded a currency manipulator in the Treasury's semi-annual report is hardly more consequential than tariffs and punitive steps against Huawei Technologies Co.

When I sent a Bloomberg News headline on July 21, 2005 that China ended its peg, people were so caught up in its prospects for appreciating that they overlooked the fact it could weaken, too. The mantra from the U.S. and its allies, as well as many investors, was that flexibility is good because China can respond more easily to shifts in its economy.

Flexibility, in truth, was code for the yuan moving only one way: stronger. In theory, that would chip away at the competitive advantage of Chinese industry, though officials were loath to say so explicitly. Now, almost a decade and a half later, flexibility means letting the yuan weaken.

China was right then to go with the flow, albeit with some fits and starts. It would be right now, too. Flexibility covers all manner of sins.

Japan used to intervene frequently in the market to cushion swings in the yen, but has been largely absent the past decade. For most of the euro’s life,ECB action has been virtually non-existent.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.