Why India’s Airlines Struggle to Take Off

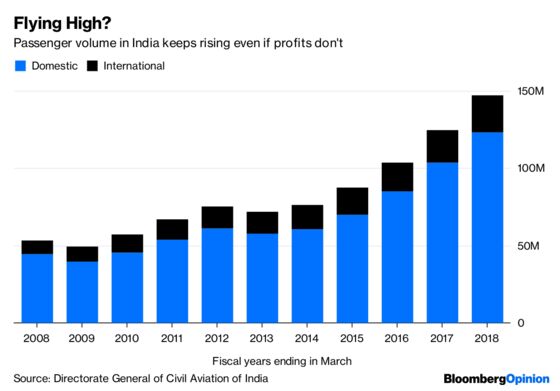

Over the past four years, passenger growth in India has been rapid, yet almost every Indian airline is struggling.

(Bloomberg Opinion) -- Anyone puzzled by how the Indian economy manages to grow swiftly while somehow failing to be prosperous could do worse than look at the state of India’s airlines. Over the past four years, passenger growth in India has been rapid: The number of flights taken has increased between 15 and 20 percent per year. Demand growth this year is likely to be the highest in the world. Yet the industry itself hasn’t benefited. Almost every Indian airline is struggling.

Consider Jet Airways Ltd., the oldest private airline in India. It’s suffered losses for three consecutive quarters now; its cumulative current liabilities have climbed to $2.2 billion. The airline is struggling to pay its pilots and has reportedly failed to make payments to the owners of its leased aircraft. It’s even been difficult for it to pay its airport fees. Another airline, SpiceJet Ltd., has been in the red for two quarters and is also delaying its payments to the Airports Authority of India. And even the market leader, the much admired IndiGo, declared a quarterly loss recently for the first time since going public in 2015.

It is easy, perhaps, to blame the fragility of this sector on variables beyond airlines’ control. When the price of fuel goes up, Indian airlines make losses; when the rupee depreciates, Indian airlines make losses. And, of course, aviation worldwide is famously crisis-prone. But there’s something special, surely, about Indian aviation, which seems to be in a nosedive even as demand is growing faster than anywhere else.

The truth is that the sector has also been weakened thanks to a combination of errors by both the private sector and, crucially, the government. Companies have lobbied as if their lives depended on it; governments have intervened as if their reelections depended on it. The consequence is that, for decades now, market forces have been stifled in the sector.

Even Jet Airways has profited in the past off government action. The airline, which is 24 percent owned by Abu Dhabi-based Etihad PJSC, benefited hugely from a controversial decision by the Indian government to multiply the number of seats permitted between Indian airports and the giant Gulf hubs of Dubai and Abu Dhabi. This gentle treatment was notably different than that handed out to Jet’s biggest domestic rival for a decade, Vijay Mallya’s Kingfisher Airlines, which was denied the right to stop and refuel its long-haul flights in the Gulf — something that would have sharply reduced its fuel bills and perhaps kept it flying longer. (Kingfisher collapsed in 2012, and Mallya is now in exile in London, where he is fighting extradition requests from an Indian government that accuses him of absconding with money from state-controlled banks.)

Government intervention is also stifling the future of the sector. Connecting smaller Indian towns and making short-haul flights profitable is central to Indian aviation’s hopes for the future. Yet Prime Minister Narendra Modi has insisted on a populist and uneconomic $35 price cap for such flights. Few airlines have been interested — and those that were discovered that metropolitan airports would prefer to give their scarce landing slots to bigger and more remunerative jets. Unsurprisingly, the new scheme to connect smaller airports seems to have crashed before it took off, with airline licenses being cancelled left and right.

And then, of course, there’s the elephant in the sky: the state-owned Air India, which lumbers along adding to its losses. Every year, the overstaffed and inefficient airline puts taxpayers deeper in debt. Worse is its malign influence on the sector as a whole. After all, it’s tough for any private airline to raise fares when one of its competitors seems to have no real budget constraint and can keep fares at whatever seems politically acceptable.

Jet is looking for investors now. Etihad — which is bleeding cash itself — might have to step up. Nobody else looks really interested, and definitely not unless they win a controlling stake; nobody was interested in buying Air India either when the government put it up for sale earlier this year. The Tata Group, which already runs one airline — Vistara — has reportedly been interested in both, but that’s because the group has had an obsession with airlines ever since Tata Airlines was nationalized in the 1950s and turned into Air India. Unless you are a little obsessed or have already invested in the sector, who’s going to want to run an airline in India?

The troubles of its aviation business are a microcosm of how the Indian economy works. From the outside, everything should be going its way — strong demand, smart companies, sound fundamentals. But a combination of private sector overconfidence and government intervention means that it’s just too difficult to make sustained profits here.

To contact the editor responsible for this story: Nisid Hajari at nhajari@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mihir Sharma is a Bloomberg Opinion columnist. He was a columnist for the Indian Express and the Business Standard, and he is the author of “Restart: The Last Chance for the Indian Economy.”

©2018 Bloomberg L.P.