Why China Has Chickened Out of Another Bank Seizure

(Bloomberg Opinion) -- When a lender suffers from a run on deposits or a funding crisis, one solution is a central-bank takeover. The People’s Bank of China, however, is finding that option has shut.

Two months after the PBOC seized Baoshang Bank Co., China’s first such move in two decades, regulators have another troubled situation on their hands. On Sunday, Bank of Jinzhou Co., a small regional lender in the rust belt province of Liaoning, got a partial bailout from three state-owned asset managers. A unit of Industrial & Commercial Bank of China Ltd., as well as distressed debt managers China Cinda Asset Management Co. and China Great Wall Asset Management Corp., agreed to buy at least 17% of Jinzhou’s shares.

The deal certainly isn’t cheap, for a bank whose books are so muddled that it still hasn’t been able to disclose its 2018 financials. ICBC’s asset-management unit agreed to purchase a 10.8% stake for as much as 3 billion yuan ($440 million), putting the acquisition tag at 0.54 times book, using Jinzhou’s latest available balance-sheet data. At this price, ICBC and Cinda could easily buy better assets: Hong Kong banks, for instance, are valued in the same neighborhood. What’s more, Jinzhou’s book value could be even lower, with more than 40% of its assets tied up in opaque wealth-management products that may have to be written down.

So why isn’t the PBOC seizing Jinzhou as well? The central bank certainly has the institutional setup for more takeovers. Since the Baoshang event, the central bank established a deposit insurance fund, similar to the Federal Deposit Insurance Corp., to protect savers. The central bank also has the bandwidth. Jinzhou is hardly a bigger burden than Baoshang – with $113 billion of assets as of June 2018, the lender is just 30% larger than its rescued peer. Because the PBOC never entertained quantitative easing on the scale of the Federal Reserve, its balance sheet remains pretty clean.

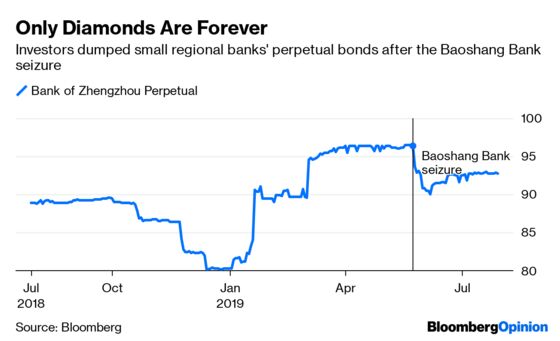

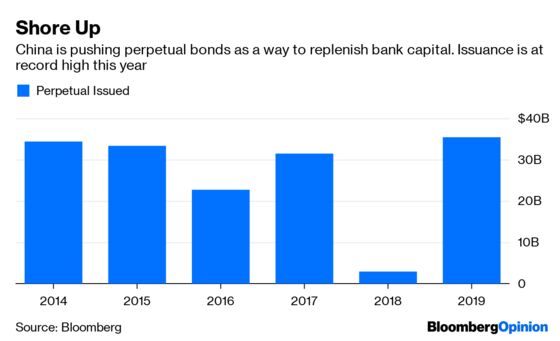

One consideration may be the stability of the perpetual-bond market. This year, the PBOC has pushed banks to tap this funding channel to replenish their capital. Banks have already issued more than $35 billion of such bonds, a record high, since Bank of China Ltd. kicked off a spate of borrowing in late January.

The trouble is, these bonds are only as good as equity in a bankruptcy – in other words, worthless. Dollar-denominated perpetuals issued by small lenders such as Jinzhou, Bank of Zhengzhou Co., Huishang Bank Corp. and Bank of Qingdao Co. all tumbled after the Baoshang seizure. Derailing Beijing’s grand plan for bank recapitalization would be a big no-no.

Jinzhou’s problems are also bubbling at a politically sensitive time, just ahead of the 70th anniversary of the founding of the People’s Republic of China. Unlike Baoshang – a subsidiary of conglomerate Tomorrow Holding Co., whose founder Xiao Jianhua was abducted from Hong Kong’s Four Seasons Hotel in 2017 – Jinzhou’s ownership is scattered among several private businesses. China’s enterprises are already wary of President Xi Jinping’s administration: Despite Beijing mouthing support for the sector, state affiliates still tend to benefit disproportionately from the government’s largess. Wiping out private businesses’ equity stakes wouldn’t be a good look right now.

The PBOC tried to do the right thing with the Baoshang takeover. But now, fearful of market jitters, the central bank is chickening out. Instead, China has resorted to the old trick of a national team rescue, which does little to break the implicit guarantee of state support. At this rate, investors in China’s $13 trillion bond market have little hope of pricing in the appropriate risks.

The PBOC even established a new facility, called the central bank bill swap, encouraginginsurers and asset managers to buy and hold perpetual bonds.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.