Where to Look in China’s Data Dump for Any Signs of a Rebound

Where to Look in China’s Data Dump For Any Signs of a Rebound

(Bloomberg) -- China’s economy is on track for its worst performance this year since the 1970s due to the coronavirus shutdowns, though data for the first quarter should be watched closely for signs of how quickly it can bounce back.

The median estimate of economists surveyed by Bloomberg sees gross domestic product contracting 6% in the three months to March, though forecasts range from -16% to growth of 3.6%.

First quarter GDP data, year-to-date investment, plus retail sales, industrial output and unemployment figures for March will be released at 10:00 a.m. on April 17.

The economy’s gradual restart reached 90% of normal levels by the end of the March, according to Bloomberg Economics estimates. Under the hood, investment, industrial output, retail sales and employment are all poised to suffer sharp declines, though any positive surprises could point to the basis for recovery in the rest of the year.

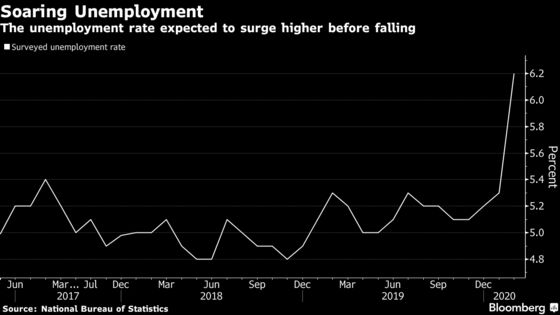

Rising Joblessness

China’s job market is likely facing the most challenging situation in decades.

The jobless rate is highly correlated with the pace of economic growth and keeping unemployment in check has been identified as a top priority for the government.In February, the urban unemployment rate jumped to 6.2%, the highest since the gauge was introduced in 2016, compared with 5.3% in January and 5.2% in December.

Morgan Stanley expects the rate to peak at 7.5% in the coming months, before gradually moderating to 5.5% by year end. That translates into as many as 80 million people losing jobs in the near term, they wrote in a report on April 9. Avoiding those job losses depends heavily on the outlook for the manufacturing sector, and government’s efforts to get firms to retain workers through the downturn.

Plunging Investment

Economists estimate that fixed-asset investment plunged by 15% in the first three months of this year, which is actually an improvement from the Jan.-Feb. period.

There is likely to have been a strong pullback in both infrastructure and manufacturing investment. Restrictions on people’s movements and lockdowns meant that there was a labor shortage after the Lunar New Year and that impeded the resumption of work in both sectors, as well as in construction.

A slump in demand, first domestically and then externally, is also likely to feed back to the manufacturing sector through a reduction in orders. At the same time, infrastructure investment likely received a boost in March from the government’s push to resume construction and efforts to channel more funds to the sector via special bond sales.

What happens with property investment will be another indicator to watch. Lackluster property sales and weak home prices likely curbed developers’ ability and enthusiasm to expand investment, and so far the government and central bank haven’t cut rates and loosened restrictions on property buying as they did during the global financial crisis. But if the economic downturn continues they may well look to this sector to drive growth again.

Reluctant Consumers

As China shifts further to a consumption-driven economy, the mood of the spending public becomes ever more vital to maintaining the pace of expansion. Consumption contributed 57.8% of GDP in 2019.

That mood will have been pretty grim in the first quarter. Retail sales likely dived 10% in March and 12.5% for the whole three-month period, Bloomberg’s survey showed, with the collapse in passenger car sales illustrating the problem. Lost jobs, shrinking salaries, still high consumer inflation and a reluctance to go outside and spend all contributed to the drop.

In the first two months of the year, online sales only helped offset part of the losses, and much now depends on government efforts to rekindle enthusiasm to shop and dine out as lockdowns in various cities ease.

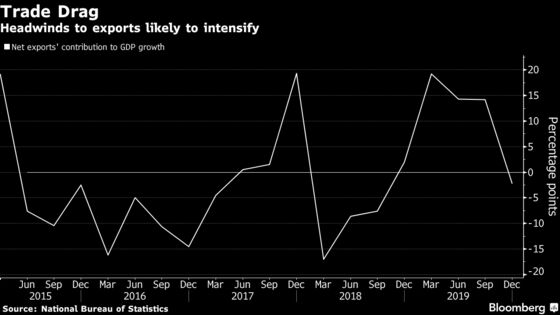

Slumping Exports

Net exports do not play the consistently supportive role for Chinese growth as they once did. So far this year trade has been hit by a double whammy of reduced production capacity at home and waning external demand due to virus containment measures.

As the virus continues to spread among China’s major trading partners, the export outlook remains dire and the drag may become heavier throughout the rest of the year.

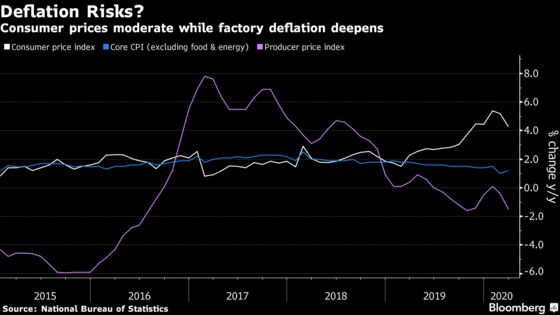

Disinflation to Deflation Risks

Even before the outbreak of Covid-19, prices were diverging across the economy, with consumer inflation still high due to rising food prices but the price of goods at the factory gate back in deflation. That difference makes it harder for policy makers to act, as high consumer inflation limits the room to ramp up monetary stimulus, but slumping factory prices reduce corporate profits and hurt pricing power.

The GDP deflator will give a broad view of price pressures across the economy, and some indication of how much room there is for expanding stimulus.

China’s efforts to prop up growth have remained subdued so far. What tomorrow’s data shows about the scale of the damage in the first quarter and any signs of recovery will shape the extent and ambition of China’s stimulus response.

©2020 Bloomberg L.P.

With assistance from Bloomberg