When the Bond Market Turned ‘Sinister,’ Fed Raced to Fix It

When the Bond Market Turned ‘Sinister,’ the Fed Raced to Fix It

(Bloomberg) -- It was mid-February when trading of U.S. Treasuries, arguably the most important assets in the global financial system, started to go haywire. Soon, alarm bells were ringing at the Federal Reserve.

Benchmark yields were moving at breakneck speeds and would drop more than a full percentage point by early March. Investors went on to aggressively sell off-the-run Treasuries, securities that are older than the recently auctioned notes and bonds which set benchmark rates. Volatility was surging as liquidity disappeared, forcing dealers to take on more positions than they possibly could move through markets.

While past episodes of Fed bond-buying were meant to stimulate the economy, the purchases this time were motivated more by an urgent need to fix this crucial market that suddenly found itself in chaos. It was practically an existential crisis for the Fed. Without a properly functioning Treasury market, the central bank’s ability to implement monetary policy is crippled.

“While liquidity has clearly been an issue before, the Fed acted with such scale and quickness because this time it started to become a much more sinister dynamic,” said Joshua Younger, head of U.S. interest-rate derivatives strategy at JPMorgan Chase & Co. “There wasn’t just intermediation frictions and illiquidity, there was also a large scale de-leveraging episode and the broader issue that the economy needed more cash than the markets could provide.”

For years, investors have warned of risks lurking in Treasuries. Bids and offers always seemed abundant -- except when you needed them most. Those concerns, back-of-mind worries for many, suddenly became a living nightmare as the ability to trade Treasuries deteriorated to the worst conditions since 2008 and the securities stopped working as a haven and hedge.

The turmoil quickly caught the attention of the central bank’s full bench of resources -- from its open-market operations desk in New York, with its seasoned leader Lorie Logan, to its Washington division directors and Chairman Jerome Powell himself. Daleep Singh, head the NY Fed’s markets division, is a former Treasury Department acting assistant secretary for financial markets.

“In the Treasury market, following several consecutive days of deteriorating conditions, market participants reported an acute decline in market liquidity,” Fed officials detailed in the record of their emergency March 15 gathering, released Wednesday. “A number of primary dealers found it especially difficult to make markets in off-the-run Treasury securities and reported that this segment of the market had ceased to function effectively.”

The Fed, like investors, was no stranger to the dangers brewing in the market, especially since Oct. 15, 2014, when Treasuries convulsed with no apparent trigger. Fed researchers in 2015 cited problems related to the growing share of liquidity provided by non-dealer market players like principal trading firms and hedge funds, many of which run fast-moving computerized strategies.

This time, the functioning of the market was threatened by an economic shock like nothing else seen in modern history. That created an unprecedented level of uncertainty about the path of policy and the outlook for inflation that is so crucial to pricing bonds.

Flight to Cash

Fed officials watched as markets were rocked by widespread deleveraging and sales of all manner of assets. Huge flows into government money market funds showed investors were fleeing to the safety of cash and cash-like instruments.

Part of the leverage unravel came amid the blow-up of the popular “basis trade” used by hedge funds, which normally is a relatively low-risk money-making strategy that wagers on the difference between prices of cash Treasuries and futures. Difficulties in trading off-the-run Treasuries was another major focal point, since those securities make up some 90% of the $17 trillion market.

Market watchers at the Fed kept an eye on the ICE BofA MOVE Index, an options-based gauge of implied volatility in Treasuries, as it lurched higher to levels last seen in the wake of the global financial crisis more than a decade ago.

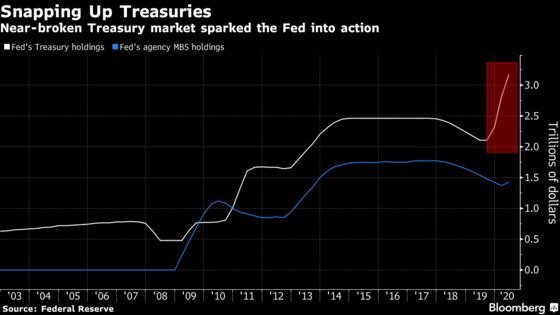

Reacting both to the economic shock and chaos in bond markets, the Fed responded with historic force. In an emergency move on Sunday, March 15, the central bank cut its benchmark rate by a full percentage point. At his press conference that day, Powell singled out the Treasury market as vital to the transmission of monetary policy and announced plans to buy at least $500 billion in notes and bonds to restore order, as well as at least $200 billion in mortgage-backed securities.

Surprise Action

“When stresses arise in the Treasury market, they can reverberate through the entire financial system and the economy,” he said.

A week later, the central bank got even more aggressive. In a surprise move before U.S. markets opened on Monday, March 23, the Fed removed earlier limits on the amounts of Treasuries and mortgage-backed securities it would buy.

Since then, the scale of the Fed’s bond-buying already dwarfs purchases made in the wake of the last financial crisis. It bought nearly $1 trillion in Treasuries by April 1. Combined with its purchases of mortgage-backed securities, the Fed’s balance sheet now tops $5.8 trillion, up from less than $4.2 trillion in late February. The central bank has scaled back its buying to about $50 billion a day now.

The dramatic efforts are paying off. A key gauge of Treasury liquidity known as market depth, or the ability to trade without substantially moving prices, has normalized after plunging to levels last seen in the 2008 crisis, according to data compiled by JPMorgan.

Swings in rates have narrowed following weekly fluctuations in the 10-year yield that averaged about 50 basis points and included some of the biggest one-day moves ever. The MOVE Index, which peaked at an 11-year high of almost 164 on March 9, has settled down to 72, less than 10 points above its 2019 average.

Mortgage debt prices have risen and their yields’ spread over Treasuries has narrowed. Bid-to-offer spreads in Treasuries -- a measure of the cost to trade -- are coming down too.

Restoring order to the market adds stability to the entire global financial system. Treasury yields anchor more than $50 trillion in global dollar-denominated fixed-income securities, while also providing the risk-free rate that serves as a yardstick against which countless investments are measured.

“The Treasury market is the benchmark for global capital markets,” said Julia Coronado, co-founder of MacroPolicy Perspectives LLC in New York, adding that it underpins the reserve currency status of the dollar. “A deep and liquid Treasury market that everybody trusts is of utmost importance. If that goes away, then everything goes away. It is the building block.”

The Fed is also giving access to dollars through multiple swap agreements with other central banks. It’s using emergency powers to become the market maker or even creditor of last resort. It also provided banks regulatory relief by excluding U.S. debt from supplementary leverage ratio rules, a move that makes holding Treasuries more appealing.

Debt to Swell

It’s all about “market functioning” now, said Priya Misra, global head of interest rate strategy at TD Securities. And with debt supply rising, Fed buying will be even more crucial, she said.

Congress’s economic stimulus effort is on course to send America’s budget deficit above 20% of gross domestic product, levels last reached in World War II. Annual net debt issuance is expected to swell to more than $2 trillion. Fed purchases limit how much of that hits the market and adds to already bloated dealer balance sheets.

Still, equilibrium has yet to be completely restored, which means the Fed can’t stand down yet.

“Markets are still fragile so if the Fed were to pull back, the same dynamic could happen again quite easily,” said Tiffany Wilding of Pacific Investment Management Co. “And we are nowhere near markets that are functioning normally at this point.”

©2020 Bloomberg L.P.