What Central Banks Did This Week as the Virus Hit Global Markets

What Central Banks Did This Week as the Virus Hit Global Markets

(Bloomberg) -- Global central banks stepped up their crisis-fighting this week in a campaign to keep markets functioning and economies growing as the coronavirus looks increasingly likely to tip the world into its first recession since the financial crisis.

Among the tools deployed: Interest-rate cuts, asset purchases, currency interventions and liquidity injections.

Markets reacted just as aggressively. Trading volatility spiked to levels not seen since the financial crisis as the S&P 500 Index’s historic bull run came to an end and signs of illiquidity emerged across debt markets. Even the $17 trillion U.S. government-bond market wasn’t immune, with the gap between prices bid and sellers’ offers widening sharply. Meanwhile, the dollar staged its biggest jump in 12 years, climbing to a three-year high, as investors piled into haven assets.

With more action likely next week, here’s a rundown of what happened this week:

The U.S. Federal Reserve

Just over a week since cutting interest rates in an emergency move, the Fed offered markets trillions of dollars in liquidity to counter signs of dysfunction. It said it would provide temporary loans to banks in coming weeks to relieve strains as investors sold government bonds to raise cash.

The Fed will also purchase a broader range of government securities than just short-term Treasury bills to make sure the liquidity reaches elements of the market which need it most. Next up? Wall Street economists now say it’s very likely Fed policy makers will cut their benchmark interest rate by 100 basis points to zero when they gather next Wednesday. They may even move before.

Treasuries whipsawed across the week, with yields on the 30-year bond seeing their widest weekly range in two decades. The promise of increased cash injections came as U.S. stocks suffered their sharpest one-day plunge since 1987.

The Bank of Japan

It offered the market up to 2.2 trillion yen ($20.7 billion) in cash injections in three different operations on Friday, while snapping up stock funds for the sixth time this month. It also pledged to maintain liquidity and keep markets stable this month.

The yen weakened versus all of its major peers on Friday as domestic stocks tumbled. Japan’s currency is still up this year against all of its G-10 counterparts except the Swiss franc.

Officials convene next Wednesday and Thursday with people familiar with the matter saying they are likely to show a more aggressive stance on buying assets such as exchange-traded funds. Whether the BOJ will raise its 6 trillion yen ($58 billion) ETF-purchasing target remains unclear and could depend on the severity of market conditions at the time of the meeting, the people added.

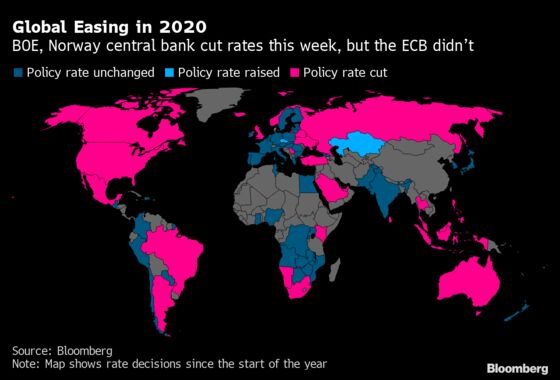

European Central Bank

The ECB tried a nuanced approach. It promised to buy more bonds, and enhanced a loan program with terms that effectively amount to an interest-rate cut for banks that use it to pump money into the economy.

But it didn’t cut its deposit rate further below zero, which disappointed investors, and President Christine Lagarde drew criticism for comments which sent Italian bonds into a tailspin and had to be clarified.

European stocks also buckled and the euro weakened before stimulus announced by Germany boosted risk appetite Friday. Yields on the German 30-year bond surged the most in a decade on the prospect of fiscal action.

Bank of England

The Bank of England started Wednesday early by unveiling stimulus including its first emergency rate cut since the financial crisis. It delivered a half-point reduction to take the key rate to 0.25%, introduced a new program to provide easy and cheap credit, and reduced a special capital buffer to give banks even more room to lend.

It acted on the same day the U.K. government announced its budget, giving a sense of coordination that investors wanted. Incoming Governor Andrew Bailey made clear it has space if it needs to do more.

The pound swung between gains and losses on the day, and ended the week down 5.9% against the dollar, the most on a closing basis since 2009.

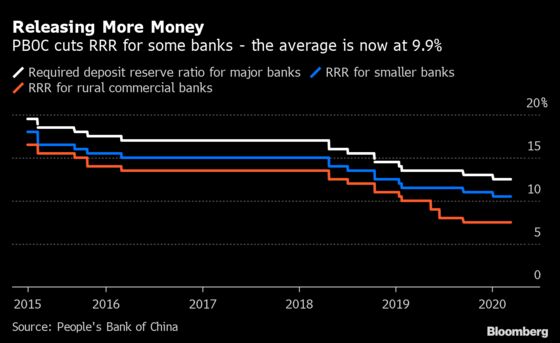

People’s Bank of China

The world’s number-two economy cut the amount of cash that banks have to set aside as reserves. It offered discounts to commercial lenders’ reserve ratios of a half or 1 percentage point from their original level. Joint-stock banks will get an additional reduction of 1 percentage point, and together the cuts will release 550 billion yuan ($79 billion) of liquidity, the PBOC said.

Bank of Canada

It surprised on Friday by cutting rates by half a percentage point as its economy is hit by the virus and falling oil prices. It said it “stands ready” to act again and also announced a new facility to acquire money market instruments used by small- and medium-size businesses. That was the second rate cut in two weeks, and on Thursday it had announced it planned to volley billions of dollars into markets. Eyes are now turning to Prime Minister Justin Trudeau’s government for a fiscal effort.

Reserve Bank of Australia

Having also cut interest rates this month, on Friday it injected A$8.8 billion ($5.5 billion) in its open-market operations, the most in at least seven years.

Reserve Bank of India

Keen to keep the rupee stable, it plans to add 250 billion rupees ($3.4 billion) through short-term repurchase operations after announcing Thursday a $2 billion injection into the foreign-exchange market.

Brazil

Its central bank used a wide array of market interventions this week to support one of the worst performing currencies in the world. In one week, policy makers intervened using auctions of lines, swap, roll-overs and dollars in spot markets, accumulating sales of around $17 billion through separate auctions. Next week will also come to effect a measure announced on Feb. 20 that freed up to 135 billion reais ($28.2 billion) in reserve requirements and other prudential measures, allowing increased liquidity to banks.

Sweden’s Riksbank

It lent up to 500 billion kroner ($51 billion) to banks to maintain the supply of credit to companies. The measure “should be regarded as a form of insurance that enables Swedish companies –- particularly small and medium-sized enterprises –- to feel secure that the credit supply will not fail,” said Governor Stefan Ingves.

Norges Bank

It also acted outside of its normal calendar on Friday to cut its benchmark to 1% from 1.5%. It said it’s “monitoring developments closely and is prepared to make further rate cuts.”

The Bank of Korea

It said it’s considering a special meeting to tackle wild swings in the foreign-exchange market. The bank also said it would take steps to stem excessive foreign exchange movements.

Bank of Indonesia

Its central bank bought 6 trillion rupiah ($405 million) of government bonds on Friday to prop up financial markets, adding to 8 trillion rupiah of bonds purchased Thursday.

Paraguay

Its central bank made a surprise quarter point cut, reducing borrowing costs to 3.75% from 4% at a meeting that took place 10 days before the scheduled date.

Bank of Mexico

Banco de Mexico expanded the maximum amount that could be issued under an existing non-deliverable forward hedge program to $30 billion from $20 billion on Monday after a steep sell-off in the Mexican peso. In an effort to increase liquidity and stabilize peso volatility, Banxico acted again on Thursday, auctioning $2 billion in hedges.

Colombia

Colombia’s central bank said it will auction 30-day non-deliverable forwards, and won’t directly sell reserves. They say this is to provide liquidity at a time of volatility, rather than an attempt to influence the value of the peso.

--With assistance from Michelle Jamrisko, Theophilos Argitis, Matthew Boesler, Jeffrey Black, Yinan Zhao, Miao Han, Toru Fujioka, Yoshiaki Nohara, Yuko Takeo, Emily Barrett, Mario Sergio Lima and Matthew Bristow.

To contact Bloomberg News staff for this story: Simon Kennedy in London at skennedy4@bloomberg.net

To contact the editors responsible for this story: Simon Kennedy at skennedy4@bloomberg.net, Fergal O'Brien

©2020 Bloomberg L.P.

With assistance from Bloomberg