What The End Of Hong Kong’s Easy Money Era Means For Home Prices

Hong Kong’s home prices rose more than 170 percent in the past decade making the city the world’s least affordable.

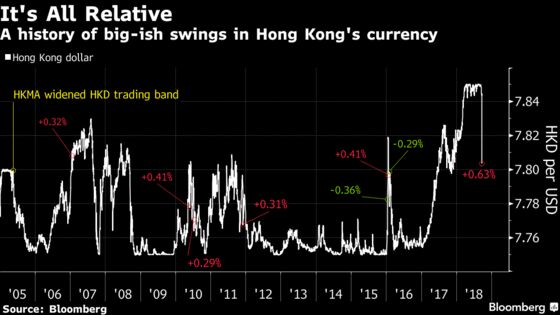

(Bloomberg) -- A shock jump in Hong Kong’s currency is signaling a decade-long liquidity party is finally coming to an end. That may be bad news for the city’s housing market.

The Hong Kong dollar surged as much as 0.6 percent on Friday, its biggest gain in 15 years. While traders gave differing reasons for the move, the common theme was concern that the city’s borrowing costs will catch up with those in the U.S. as the Federal Reserve continues to hike rates.

A currency peg with the U.S., open financial borders and a booming economy meant Hong Kong property was one of the greatest beneficiaries of ultra-low lending costs in the wake of the global financial crisis. Home prices rose more than 170 percent in the past decade making the city the world’s least affordable. Citigroup Inc. and CLSA Ltd. are among those warning of a reversal on expectations that mortgage servicing costs will rise.

"The market has underestimated the pace of interest rate increases in Hong Kong," said Kevin Lai, chief economist for Asia ex-Japan at Daiwa Capital Markets Hong Kong Ltd. This “will bring pressure to the property market and leveraged home buyers."

After trading at the weak end of the band for months, prompting repeated interventions by the city’s de facto central bank, the Hong Kong dollar rocketed into the stronger half of the spectrum on Friday.

The three-month interbank rate, known as Hibor, was last at 2.125 percent, its highest level in almost a decade. A narrowing spread with U.S. Libor is making a previously profitable trade of selling Hong Kong dollars to buy higher yielding U.S. assets less appealing.

"The short-Hong Kong dollar carry trade has come to an end," said Ken Peng, an investment strategist at Citi Private Bank in Hong Kong. "Friday’s move suggests borrowing costs in Hong Kong have tightened a lot and will tighten further."

The Hong Kong Monetary Authority said in emailed comments that while it didn’t want to comment on Friday’s movement in the currency, "market participants generally view the elevated interbank interest rates as a contributing factor."

While residential prices in Hong Kong’s secondary market have climbed 16 percent over the past 12 months, according to Centaline Property Agency, developers have begun to offer perks such as free rail tickets to accelerate sales. Some are selling apartments at discounts, and others aren’t providing mortgages due to concern that rising borrowing costs may increase defaults. Financial Secretary Paul Chan said this month he sees signs the market is cooling.

Record Highs

Predicting declines in Hong Kong’s property market hasn’t been a profitable exercise in the past, with a home-price slump in 2015-2016 quickly followed by new record-highs. But expectations are growing that banks will increase the so-called prime rate, which caps the costs of mortgage repayments for many homeowners, for the first time since 2006.

"We expect banks to hike prime rate twice this year by a total of 50 basis points, as Hibor rises with a shrinking liquidity pool and Fed hikes," said Frank Lee, acting chief investment officer for North Asia at DBS Bank (HK) Ltd. "It will hurt property market sentiment."

--With assistance from Katrina Nicholas and Shawna Kwan.

To contact the reporters on this story: Tian Chen in Hong Kong at tchen259@bloomberg.net;Emma Dai in Hong Kong at edai8@bloomberg.net

To contact the editor responsible for this story: Richard Frost at rfrost4@bloomberg.net

©2018 Bloomberg L.P.