What's Got U.S. Inflation So Depressed? Just Asking for the Fed

What's Got U.S. Inflation So Depressed? Just Asking for the Fed

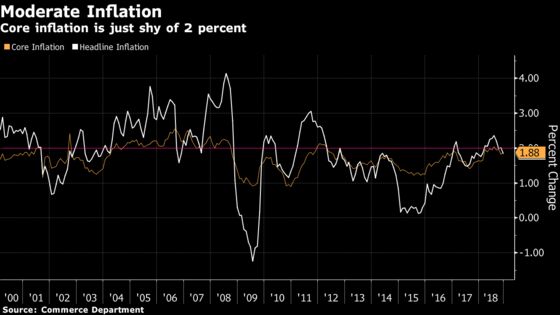

(Bloomberg) -- The Federal Reserve has been tightening monetary policy since 2015 to keep inflation in check. Low unemployment would spur businesses to pay more and raise prices, the logic went, so it was important to head off economic overheating.

That conventional wisdom is looking a little shaky.

Price gains have lingered below the Fed’s 2 percent goal despite years of super-low unemployment and Chairman Jerome Powell said on Jan. 30 that the risks of too-high inflation have “diminished.” He noted that market-based inflation expectations have moderated and suggested that gains might actually slow before they accelerate again.

Weaker gains give the Fed room for renewed patience -- it signaled it will pause interest-rate increases amid tremulous global growth and tighter financial conditions -- but they’re also puzzling economists from Washington to Wall Street. With joblessness hovering around a nearly five-decade low, why isn’t the theoretical relationship rearing its head?

University of Texas at Austin’s Olivier Coibion and co-authors Yuriy Gorodnichenko and Mauricio Ulate say the U.S. simply hasn’t hit full employment. Labor slack still comes with a side of weak price pressure, they argue in a new National Bureau of Economic Research working paper, and inflation is slow because would-be workers remain on the margins.

(You’re reading Bloomberg’s weekly economic research roundup.)

The shortfall owes to “economic slack not just in the U.S. but in most advanced economies.” While the unemployment rate -- which measures people who are working or looking -- is historically low, the ratio of those at work relative to the overall population is still lagging pre-crisis levels. As a result, the researchers estimate that the unemployment gap in both the U.S. and a broader group of 18 nations stands at around 1 percentage point compared to pre-recession full-employment years.

Laurence Ball at Johns Hopkins University and Sandeep Mazumder blame a different culprit entirely: price gauges. They say policy makers should watch a weighted median of industry inflation rates -- a measure that strips out a lot of volatility. “The Phillips curve shows up clearly when core inflation is measured more precisely,” they write in a recent working paper. Fix the metric, and the breakdown disappears.

For more on this topic:

|

A weak price response to a stronger job market isn’t unique to the U.S. Researchers in Europe also ask whether old relationships hold.

A fresh European Central Bank working paper takes a look at one key part of the labor market-price relationship: the link between wages and prices. They find that higher pay precedes higher prices in four euro-area economies, but the pass-through is lower in periods with low inflation. The effect is also dependent on what’s driving labor costs up, with demand-driven increases more likely to boost prices.

Also worth a read this week:

Low interest rates may be driving market concentration, Princeton University’s Atif Mian and Ernest Liu and the University of Chicago’s Amir Sufi argue in this working paper. While theory would suggest rock-bottom interest rates inspire businesses to invest money, the economists point out that it’s important to take strategic competition and market structure into account.

The idea? Lower rates will inspire leading firms to invest even more than lagging firms so that they can solidify their productivity advantage. As the star company wins out, laggards actually lose incentive to invest. The prediction holds up in data stretching back to 1962, the authors write.

“The model provides a unified explanation for why the decline in long-term interest rates has been associated with rising market concentration, reduced dynamism, a widening productivity-gap between leaders and followers, and slower productivity growth,” they find.

New York University’s Hunt Allcott and Stanford University co-authors Matthew Gentzkow and Chuan Yu find that misinformation is shifting toward Twitter. They measure the diffusion of content from 569 fake news websites and 9,540 fake news stories on Facebook and Twitter between January 2015 and July 2018. They find that interactions with false content rose steadily on both platforms through the end of 2016, but have since fallen on Facebook. Misleading tweets have still been on the rise.

That said, Facebook is still home to more interaction with misleading information: the ratio has simply declined from 45-to-1 at the start of the study period to 15-to-1 at the end.

To contact the reporter on this story: Jeanna Smialek in New York at jsmialek1@bloomberg.net

To contact the editors responsible for this story: Alister Bull at abull7@bloomberg.net, Jeff Kearns

©2019 Bloomberg L.P.