Bank of Israel Clings to Currency Interventions With Rates Held

Wharton Professor Turned Central Banker Falls for Weaker Shekel

(Bloomberg) --

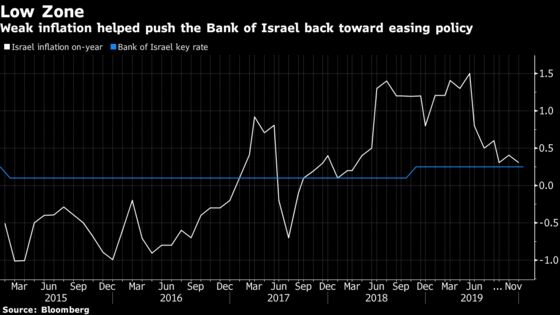

The Bank of Israel prolonged its interest-rate pause to over a year after almost doubling the pace of foreign-currency purchases and pinning much of the blame for weak inflation on gains in the shekel.

With Israel struggling for years to keep price growth within its target band of 1% to 3%, the central bank is reviewing whether the goal is still appropriate, Governor Amir Yaron said, repeating a theme he’s sounded before. Policy makers left their key rate at 0.25% earlier on Thursday, as forecast by every economist surveyed by Bloomberg.

“The Bank of Israel is prepared to prevent excessive appreciation of the shekel, by purchasing foreign exchange whenever necessary, and particularly to the extent that we assess that the appreciation is the result of relatively short-term financial factors,” Yaron said at a news conference.

Reluctant to cut borrowing costs for the first time since 2015, the Bank of Israel wants to preserve a sliver of policy space before rates approach zero again or potentially enter negative territory, a relatively untested option that other countries are starting to abandon. It also needs to tread carefully at a time of unprecedented political paralysis in Israel and with the Middle East in the grip of turmoil.

The central bank’s research department lowered its outlook slightly for inflation and economic growth, and now predicts that Israel’s main rate will be unchanged or down to 0.1% in one year.

“It will be necessary to leave the interest rate at its current level for a prolonged period or to reduce it,” the central bank said in a statement, maintaining its previous guidance. “Furthermore, the Committee is taking additional steps as necessary to make monetary policy more accommodative.”

Rates, Intervention

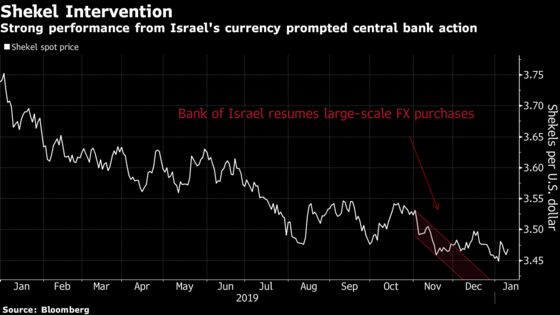

When Yaron took over in December 2018, his intent was to deliver a measured tightening and to let the market determine the shekel’s exchange rate. But its steady strengthening, largely attributed to the country’s current-account surplus and foreign investment, prompted the central bank to restart purchases of foreign currency, first begun under its former leader Stanley Fischer.

After hardly intervening all year, the Bank of Israel bought $3.6 billion during the last two months of 2019, embarking on the biggest intervention in nearly a decade that raised its reserves to a record.

It’s barely dented the shekel, however, which has appreciated against the dollar both in November and December and was the fifth-best performer globally against the dollar in 2019. Israel’s currency was 0.3% weaker versus the greenback as of 5:46 p.m. in Tel Aviv.

But although inflation remains stuck below the central bank’s target range, Israel’s economy topped its forecast with growth of 3.3% in 2019 and unemployment is around all-time lows. Consumer prices rose just an annual 0.3% in November.

The updated staff forecasts show inflation at 1% this year and the economy growing 2.9%.

The central bank also needs to navigate a period of political tumult and uncertainty for Israel, which remains without a government after two inconclusive elections last year. Another vote is coming up in early March, and until then the country remains without a permanent budget -- a predicament that policy makers have warned could have “a contractionary effect” on the economy.

As the focus remains on steering Israel’s currency weaker, the central bank has also examined negative rates and even large acquisitions of government bonds to get in the way of the shekel’s appreciation and bring inflation closer to the target, according to Andrew Abir, a voting member of the monetary committee and market operations director.

“If the shekel will stay strong as it is, the probability for non-sterilized dollar purchases is not very low,” Ori Greenfeld, chief economist at Psagot Investment House Ltd. in Tel Aviv, said in a note. “A step in this direction is similar to a cut in the effective rate.”

--With assistance from Harumi Ichikura and Yaacov Benmeleh.

To contact the reporters on this story: Ivan Levingston in Tel Aviv at ilevingston@bloomberg.net;Alisa Odenheimer in Jerusalem at aodenheimer@bloomberg.net

To contact the editors responsible for this story: Lin Noueihed at lnoueihed@bloomberg.net, Paul Abelsky

©2020 Bloomberg L.P.