Steady U.S. GDP Could Mask Weakening Consumption

Steady U.S. GDP Could Mask Weakening Consumption

(Bloomberg) --

On the surface, U.S. economic growth last quarter is projected to look decent and little changed from the prior period. But the main figure could mask a misfire in the economy’s chief engine: the consumer.

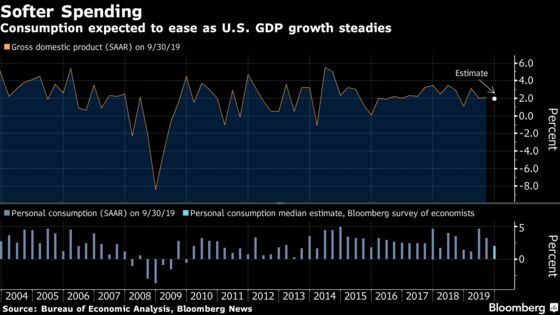

Gross domestic product probably climbed at an annualized 2% rate in the fourth quarter, compared with 2.1% in the prior period, according to the median forecast in a Bloomberg survey of economists before the Commerce Department’s report on Thursday.

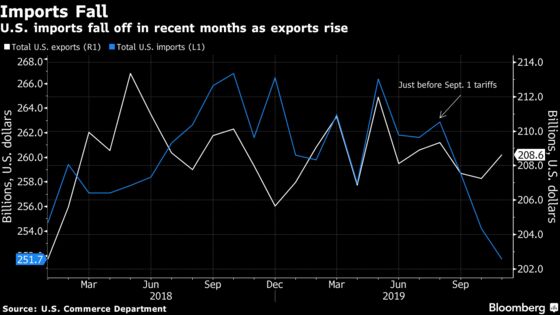

However, the principal sources of fuel for the top-line number -- a narrower trade deficit, driven almost entirely by a drop in imports, and stronger residential investment -- likely helped offset a pullback in personal consumption.

Household spending, coming off the best consecutive quarters since late-2014 to early 2015, kept economic growth on pace last year through stiff headwinds including a corporate investment slowdown, the U.S.-China trade war and the grounding of Boeing Co.’s 737 Max plane. But in the fourth quarter, economists forecast personal consumption rose just 2%, down from 3.2% in the third quarter and 4.6% in the second.

A downshift in spending is in line with economists’ expectations for a moderating growth picture that makes achieving President Donald Trump’s goal of 3% economic growth more challenging ahead of the November election. Year-over-year GDP growth is forecast to slow to 1.8% in the fourth quarter of 2020, down from 2.3% in 2019 and 2.5% in 2018.

While still a solid pace, the question of 2020 becomes: “Can the consumer continue to sustain the expansion while we’re in this soft patch of business spending?” said Brett Ryan, senior U.S. economist at Deutsche Bank AG. “The fourth-quarter GDP data may call that into question.”

Several economists lowered their tracking estimates of GDP Wednesday after a Commerce Department report showed the merchandise trade deficit widened more than expected in December while inventories missed forecasts.

Consumer spending, which accounts for about 70% of GDP, is always an important driver of growth, but two consecutive quarters of falling business investment have shifted the responsibility of keeping the expansion afloat squarely on the back of American shoppers.

Fed Policy

While consumers and the economy had the benefit of three Federal Reserve rate cuts in 2019, the central bank’s policy makers kept borrowing costs steady at their meeting Wednesday and have signaled they will be on hold the rest of the year. Still, traders are increasingly projecting an interest-rate cut this year given the quickly spreading coronavirus in China that has the potential to disrupt demand.

A healthy labor market -- characterized by the lowest unemployment rate in a half century and rising participation -- and elevated consumer sentiment should underpin spending in the months ahead, but the waning effects of tax cuts along with moderate wage gains may limit consumption.

What Bloomberg’s Economists Say

“Top-line GDP growth should raise few concerns even if it slowed slightly in the final quarter of last year. Yet a large contribution from faltering imports would imply a weakening underlying composition of growth. Nonetheless, the Fed will maintain its assessment that the economy is in ‘a good place,’ and save its ammunition in case of a more critical slowdown in economic activity.”

-- Yelena Shulyatyeva, Andrew Husby, Eliza Winger and Carl Riccadonna

At the same time, while consumer spending on goods and services may have cooled in the fourth quarter, Americans were busy buying homes. After more than a year of weighing on growth, a housing rebound is expected to soften the blow from another quarter of lackluster nonresidential investment.

Like the overall GDP reading, the strength stems more from the figure’s accounting than actual strength in the underlying fundamentals. Exports have increased slightly but remain broadly unchanged while imports have sharply dropped, particularly because of swings in tariffs.

Offsetting a weaker consumer are “lower imports, which is generally not a wonderful sign in terms of the vitality of the domestic economy,” said Joshua Shapiro, chief U.S. economist at Maria Fiorini Ramirez Inc. “When the economy is strong and demand is strong, imports tend to grow, not shrink.”

The partial trade agreement signed earlier this month has the potential to stimulate corporate investment once again and shift some of the heavy lifting away from consumers.

All in all, despite the variety of headwinds the economy faced last year, “we continue to see economic growth chug along,” said Sarah House, senior economist at Wells Fargo & Co. “Consumers are still in pretty good shape.”

--With assistance from Chris Middleton.

To contact the reporters on this story: Reade Pickert in Washington at epickert@bloomberg.net;Max Reyes in New York at mreyes125@bloomberg.net

To contact the editors responsible for this story: Scott Lanman at slanman@bloomberg.net, Vince Golle

©2020 Bloomberg L.P.