VW Warns Trade War Gloom Is Getting ‘Scary’ as Car Sales Slow

VW Warns Trade War Gloom Is Getting ‘Scary’ as Car Sales Slow

(Bloomberg) --

Volkswagen AG and other carmakers warned that trade tensions risk dragging the global economy into a recession as the fallout starts to hit consumers.

The gloom of the U.S. and China’s tit-for-tat tariffs cast a shadow over the Frankfurt Auto Show this week, where carmakers were seeking to whip up interest in critical new electric models. The geopolitical volatility adds another layer of uncertainty to an industry in the midst of a radical overhaul as the end of combustion-engine era looms.

“We come now into a situation where this trade war is really influencing the mood of the customers, and it has the chance to really disrupt the world economy,” Volkswagen Chief Executive Officer Herbert Diess said in an interview with Bloomberg TV. “China is basically a healthy market, but because of the trade war, the car market is basically in a recession. So that’s a new situation. That’s scary for us.”

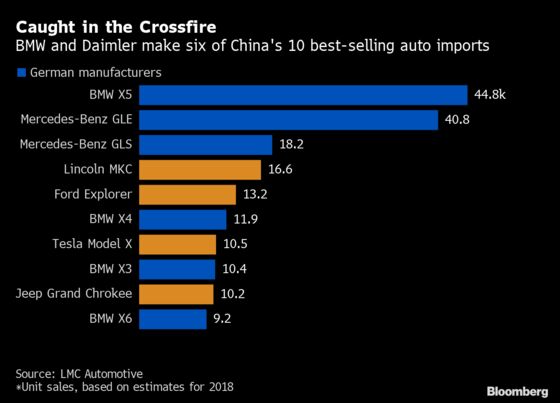

Concerns about global trade have reached nearly 10 times the peaks seen in previous decades and could shave about 0.75 percentage points off world economic growth this year, according to data compiled by the International Monetary Fund. The auto industry is particularly exposed because of its global network of assembly plants and parts suppliers. Daimler AG, for instance, makes many of its Mercedes-Benz’s SUVs in Alabama and exports them to China and other markets.

“What will happen in 2020 will very much depend on what happens with the U.S. and China in the coming weeks,” BMW AG Chief Financial Officer Nicolas Peter said in an interview with Bloomberg TV at the Frankfurt show, Germany’s premier auto exhibition. The German manufacturer assembles most of its sport utility vehicles in South Carolina.

After months of talks, the tensions between the U.S. and China remain high. Ted McKinney, the top trade official in U.S. President Donald Trump’s Agriculture Department, called Chinese President Xi Jinping a “communist zealot” in the mold of Mao Zedong. After a summer of bombast and tariff escalation, the two sides have agreed to hold face-to-face working-level staff talks in the coming weeks and a ministerial meeting in Washington in early October.

“Everyone is affected by the industry downturn, everyone is suffering,” Continental AG CEO Elmar Degenhart told reporters Tuesday in Frankfurt. Europe’s second-largest auto supplier plans to finalize a review of its sprawling global manufacturing network by the end of this year and doesn’t rule out factory closures or layoffs as part sweeping restructuring plans.

Outside the car show, other German industry leaders voiced their concerns about trade risks. Siemens AG Chief Executive Officer Joe Kaeser urged the European Union to assert its voice in the trade conflict between the U.S. and China, saying the specter of a “decoupling” of political and economic systems would break with decades of integration and ultimately risk a global slowdown.

“Europe would be well advised to avoid this bilateral decoupling, but it can only achieve this when it is heard as a third force in the world, and that’s not the case at the moment,” Kaeser told journalists in Berlin. There’s a sense that the world is reorganizing into new economic spheres, making it harder for export-oriented companies to do business and creating the risk of “having to decide between friend and foe,” said the executive, who recently returned from a trip to China with German Chancellor Angela Merkel.

‘Good Sense’ Brexit

On top of the U.S.-China spat and Trump’s recurring threat to impose levies on European car imports, the industry is bracing for the potential of the U.K. crashing out of the EU without a deal in a few weeks. BMW, which owns the British-based Mini and Rolls-Royce car brands, has set up a 300 million-euro ($330 million) fund to deal with a possible hard Brexit and would reduce output at its plant in Oxford, England, by eliminating a work shift if that happens, CFO Peter said.

“We’d have to increase prices, and we have to curtail production to react to such a development,” Peter said on BMW’s contingency preparations for a crash British exit. “The plans are in the drawer.”

In a Bloomberg TV interview, PSA Group CEO Carlos Tavares called the prospect “not acceptable” on ethical grounds and appealed to European and British leaders to show “good sense” and avoid a no-deal Brexit.

Ralf Speth, the CEO of Jaguar Land Rover, laid out the complexity of an abrupt disruption to trade flows, saying the British manufacturer needs as many 25 million parts a day to be delivered on time and requires six to eight weeks to decide on ordering components. With Prime Minister Boris Johnson insisting that the U.K. will leave the EU on Oct. 31 “do or die,” the auto industry is facing its Brexit crunch time now.

“Free and fair trade is best for society. Currently we’re falling back on that,” said Speth, who unveiled a resurrected version of the Land Rover Defender offroader in Frankfurt. “It’s so critical to prepare in the very best way for alternatives. But in the end, no one really knows.

For the auto industry, the trade squeeze clouds efforts to show off slick new models like the Porsche Taycan and VW ID.3 as German brands ramp up electric offerings to meet increasingly stringent environmental regulations. Demand disruptions threaten to squeeze profits needed to fund the high-risk rollout.

“We hope there won’t be any recession in the mid term or long term, because it would be a self-made recession,” Diess said.

--With assistance from Matthew Miller, Benedikt Kammel and Elisabeth Behrmann.

To contact the reporters on this story: Christoph Rauwald in Frankfurt at crauwald@bloomberg.net;Oliver Sachgau in Frankfurt at osachgau@bloomberg.net

To contact the editors responsible for this story: Anthony Palazzo at apalazzo@bloomberg.net, Chris Reiter, Chad Thomas

©2019 Bloomberg L.P.