Rates Volatility Lacks Optimism on Global Reflation Trade

Rates Volatility Lacks Optimism on Global Reflation Trade

(Bloomberg) -- U.S. volatility markets are showing a lack of confidence in the global bond reflation trade.

After a huge rally over the first eight months of the year gave way to a sell-off on trade optimism, bond markets are yet to see a decisive turning point in the economic data. Recent moves are being driven by sentiment rather than a definitive trend in fundamentals.

The signals from options pricing highlight the lack of conviction on whether yields will break out in either direction, pointing to broader ranges being maintained for now.

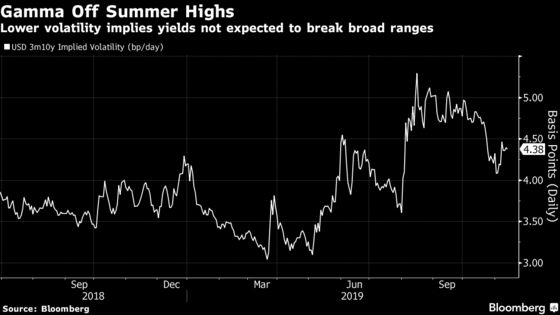

- Volatility across the swaption grid has fallen over the last month, indicating the potential for a range-bound yield environment.

- Implied volatility on the 10-year swap rate is suggesting a potential move of around 28 basis points in either direction over the next three months, which leaves the expected moves trading within broader ranges.

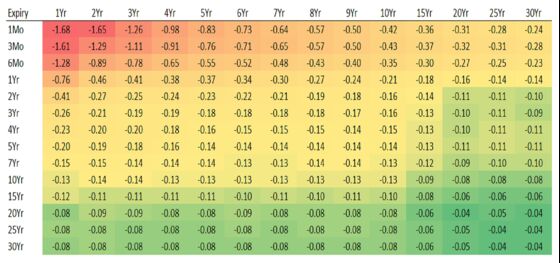

- The 1y10y vol roughly implies a 68% chance of 10-year Treasury yields between 2.5% and 1.2% in one years’ time, which isn’t particularly irrational over that timeframe.

- Without clear signals on where the economy is going, broad ranges are likely to be maintained.

- The upper-left side of the swaption grid, which is more sensitive to monetary policy, has been dumped with the Fed now on hold.

- The right-side has outperformed given the recent large realized moves in long-end rates on trade optimism and likely pickup in convexity hedging needs.

- In terms of the Fed outlook, the market will trade from the position that further rate cuts are more likely to follow disappointing data, compared with the chances of a rate hike on positive data surprises.

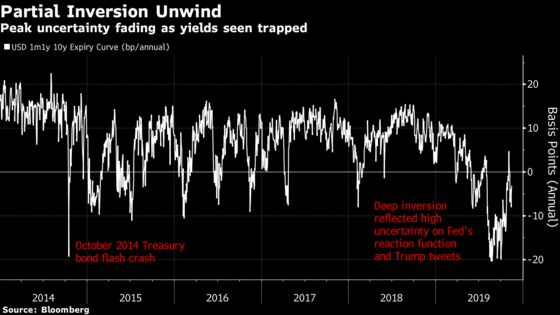

- The deep inversion of the expiry curve seen in recent moves has nearly unwound. The expiry inversion went to levels not seen since the flash crash in Treasuries in October 2014.

- This inversion highlights the poor risk/reward on taking a view with high conviction, given the level of uncertainty around Donald Trump’s tweets and the Fed’s reaction function.

- There have been a number of false positives in the U.S.-China trade saga, and optimism of a phase one deal is largely reflected in the price.

- A more extensive deal or positive economic data triggers are needed for a further sell-off to drive 10-year Treasury yields up to the 2.1%-2.3% zone seen in the summer.

- A tactical limited sell-off view may be expressed via 3m10y payer spreads funded by front-end payers given the high bar for a Fed hike, which has a net short payer skew and short vol exposure.

- The asymmetry exists in the volatility skews toward lower yields. OTM receivers are trading at a premium to OTM payers across the surface on higher concerns over a worsening global growth outlook. That has somewhat corrected recently on trade optimism.

- Any sell-off in duration will be limited by demand from yield-hungry investors, with foreign money from the likes of Japanese accounts buying Treasuries on an unhedged basis.

- NOTE: Tanvir Sandhu is a global fixed income and derivatives strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

To contact the reporter on this story: Tanvir Sandhu in London at tsandhu17@bloomberg.net

To contact the editors responsible for this story: Paul Dobson at pdobson2@bloomberg.net, Neil Chatterjee, William Shaw

©2019 Bloomberg L.P.