Ultraloose ECB Monetary Policy Signals Faster Tightening Ahead

Ultraloose ECB Monetary Policy Signals Faster Tightening Ahead

(Bloomberg Markets) -- The European Central Bank announced in June that it would soon end its asset purchase program. It also indicated that the first rate hike will come after summer 2019. Our estimates of the neutral policy rate suggest the second increase shouldn’t be too far behind.

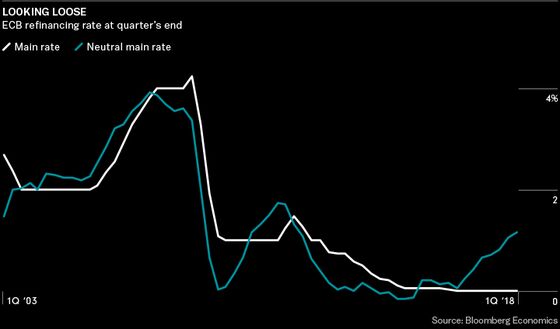

Monetary policy is looser than called for at this stage of the economic cycle, according to our analysis. Given the ECB’s enormous stock of asset purchases, the refinancing rate might need to be 1.25 percentage points higher to keep the euro-area economy on trend. If the stance of policy prompts overheating, the ECB may find it has some catching up to do.

What Is the Neutral Rate, Again?

For each economy, there’s a neutral rate that will keep aggregate demand expanding at its potential rate once the output gap—the difference between actual and potential output—has been eliminated. In other words, it’s an interest rate that’s just right—neither so low that the economy overheats nor so high that it cools.

How Do We Measure It?

The neutral rate can’t be observed directly. So we have to work it out by looking at actual interest rates and taking the economy’s temperature. When the economy has overheated, that suggests policy was too loose—interest rates were below the neutral rate. Conversely, if the economy is operating with spare capacity, actual rates may have been above the neutral rate. And because we think we know how much lower borrowing costs boost the economy (or how much higher costs hurt it), we can infer what the neutral rate might be. In normal times, it would be surprising if the neutral rate were to move suddenly. So we can assume that it evolves slowly unless there’s a big shock.

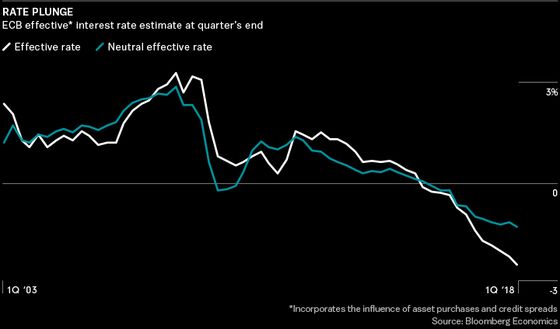

To estimate the neutral rate, we adapt a Federal Reserve Bank of San Francisco paper by Thomas Laubach and John Williams. In addition, we also take into account the influence of asset purchases and credit spreads, creating a measure called the effective interest rate. And we use the modeling framework to estimate its counterpart, the effective neutral interest rate.

What Does History Tell Us?

Charting our estimates shows that the effective and neutral rates weren’t too far apart in the early days of the euro area. Then, during the global financial crisis, the neutral interest rate plunged, reflecting weaker trend growth and a widening of credit spreads. As spare capacity opened up, effective rates remained above the neutral rate, suggesting the crisis could have been less severe if policy had been more responsive.

The same seems to have been broadly true during the euro crisis and its aftermath. Since then, the neutral effective interest rate has continued to fall, and the ECB has pushed the actual effective rate down further by purchasing assets. In short, policy has become much more accommodative. At the same time, the margin of spare capacity in the economy has shrunk—we estimate slack will be almost completely used up by the end of the year.

At that point, the effective interest rate ought to be raised to the neutral effective interest rate. But our estimates suggest the gap will still be very wide—about 125 basis points. Our model suggests policy is ultraloose.

Asset purchases will end this year, possibly later than necessary. In fact, the last rounds of asset purchases may not have been needed at all. Still, the ECB clearly thought the insurance against the possibility of deflation was necessary. It was a reasonable position to take, but the central bank may have to play catch-up if inflation begins to accelerate more than expected. In the meantime, it has the luxury of remaining cautious.

With quantitative easing no longer the active instrument of monetary policy, it’s worth thinking about what all this means for the main policy rate. Given the amount of QE in the system, the neutral policy rate is now much higher than the current zero percent refinancing rate.

When Will the First Hike Come?

When the ECB kept rates unchanged in June, President Mario Draghi said, “We expect them to remain at their present levels at least through the summer of 2019.” In July, he reiterated the guidance. That likely means the deposit rate will be increased by 15 basis points in September of next year. Such a small increase, to -0.25 percent from the current -0.40, would restore normality to the ECB’s interest rate corridor—the bank’s three rates had previously been 25 basis points apart. Financial markets are indicating the same thing: The euro overnight interest-rate swap curve has priced in 10 basis points of tightening in one year.

And the Next One?

The second rate increase may follow rather quickly, given the modest nature of the deposit rate hike. Financial markets have priced in an additional 25 basis points of tightening from 12 months to 24 months but provide little clarity as to when. Surveys of economists point to first quarter 2020. We forecast one 25-basis-point hike every six months after the first increase. That reflects the ECB’s cautious approach to policy making.

This analysis suggests the risks to that expectation are skewed to the upside. If growth keeps chugging along and inflation accelerates faster than forecast, the ECB may find itself behind the curve. Rates could rise at a quicker pace, especially if Jens Weidmann, the Deutsche Bundesbank’s hawkish president, takes the helm at the ECB when Draghi’s term ends in November 2019.

Powell, Murray, and Hanson are economists at Bloomberg Economics in London.

To contact the editor responsible for this story: Jon Asmundsson at jasmundsson@bloomberg.net

©2018 Bloomberg L.P.