Putin’s Financial Isolation by World’s Powerful Is a Cautionary Tale for Xi Jinping

The speed of Russia sanctions are a cautionary tale, and a reminder of why China is so desperate to break the dollar's hegemony.

(Bloomberg) -- It's the dominant geopolitical narrative of our era: The global economy is cleaving into two blocks as an ascending China and declining U.S. clash over trade, technology and the pandemic.

After Vladimir Putin’s invasion of Ukraine and the sanctions it provoked from the U.S. and allies, that divide appears sharper than ever — but the contest also looks more uneven. The economic isolation imposed on Russia has been a stark reminder of the persistence of American power.

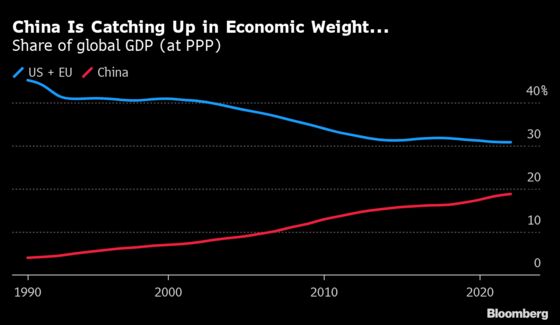

China is catching up to the U.S. in terms of gross domestic product, and already eclipsed it in trade and manufacturing. But when it comes to the architecture of money that underpins the world economy, America and its dollar-led system remains the undisputed leader.

“The locus of financial power still remains very firmly in the hands of the West,’’ says Eswar Prasad, a Cornell University economist who’s spent years studying China’s challenge to the greenback.

That’s been apparent as the U.S. and its allies in Europe and Asia coalesced around an ever-tighter series of sanctions after Putin sent his troops into Ukraine. They’ve severed Russia from the world economy so profoundly that the effects may be felt for years.

The ruble collapsed, the central bank lost access to a large chunk of its foreign-currency savings, the government had to impose capital controls, and giant international companies from Apple Inc. to Royal Dutch Shell Plc raced each other out of the country.

For China’s President Xi Jinping, who just weeks ago declared a no-limits friendship with Moscow, the speed with which Russia has been cut off is a cautionary tale – and a reminder of why China’s leaders are so desperate to develop an alternative to U.S. dollar hegemony. It may yet motivate Beijing to speed up that project.

Read more: Bloomberg Economics on Russia Sanctions and China Blowback

In Washington, meanwhile, U.S. leaders have trumpeted the display of U.S. money power.

“When the history of this era is written, Putin's war on Ukraine will have left Russia weaker and the rest of the world stronger,’’ said President Joe Biden in his State of the Union address this week. In what may have been a barb at China, he noted that “in the battle between democracy and autocracy, democracies are rising to the moment.’’

It’s early for anyone to declare victory. The shockwaves from Russia’s war in Ukraine are only just beginning.

Oil prices above $110 a barrel already threaten to push inflation, driven to multi-decade highs in the pandemic, even higher. That spells danger for Biden, whose popularity has already been eroded by soaring gasoline costs, and for leaders in Europe, whose economies still depend on Russian energy.

‘Stopped Clock’

Investors have rushed to price in a more divided global economy. In the U.S., defense stocks have been on a tear after European countries like Germany — long resistant to allocating more cash to their military forces — suddenly pledged to ramp up spending. And in China, companies linked to the payments system that the country has been seeking to build as an alternative to Western ones, have seen their shares soar.

Plenty of economists agree that the polarization is real. Adam Posen, president of the Peterson Institute for International Economics, calls it the “corrosion of globalization.’’ He says it began with President Donald Trump’s trade war with China, and continued through the pandemic as economies turned inward. Now it’s accelerated.

“Everybody has been talking for a long while about blocs and the global economy splitting up,’’ says Posen.

He was skeptical before. Now, he thinks, “the stopped clock is finally right’’ — and the eventual result will be a global economy that’s less productive and innovative as it turns combative, with consumers everywhere paying a price.

But in the near term, at least, there are reasons to think China won’t be in a hurry to take Russia’s side in all-out economic confrontation with the U.S. Indeed, Xi is treading a fine line so far.

While China has declined to slap financial penalties on Russia and will likely help it weather the sanctions storm by buying oil, gas and wheat, limits to the “no limits’’ friendship already appear to be emerging. Political leaders have talked of the need for a quick cease-fire and some big Chinese banks have restricted access to financing purchases of Russian commodities.

That pattern has been apparent in the past: China may disagree with the political goals of Western sanctions, but it has tended to avoid confronting them head on. Even Chinese state-run banks, for example, have complied with past U.S. curbs on Hong Kong. Carrie Lam, the territory’s Beijing-friendly chief executive, said in 2020 that she was collecting “piles of cash” at home because the U.S. measures barred her from basic banking services.

“The Chinese banks are actually quite leery of running afoul of the U.S. Treasury,’’ says David Dollar, a senior fellow at Brookings and former Treasury representative in Beijing. “The big Chinese banks are among the largest in the world, they're deeply integrated with the global system. So they're going to be careful.’’

‘Bad News’

The fundamental reason for this caution: Xi presides over an economy that’s much more deeply intertwined with the world than Putin’s — in fact more so than it has ever been, after largely shrugging off any effects of the Trump trade war.

Chinese exports broke records during the pandemic. An analysis by HSBC economists found that over the past three years — when talk of decoupling and a brewing economic Cold War was rife — China’s trade grew about five times faster than the global average, while foreign direct investment there increased even as it was falling elsewhere.

Giving up all that to join Russia in an economic fight with the West right now “would be bad news for China,’’ says Hui Feng, a senior lecturer at Griffith University in Queensland, Australia and co-author of “The Rise of the People’s Bank of China.” “It will be supplied with cheap Russian oil and other energy products. But it will suffer from a structural decoupling in technology and investment.’’

That doesn’t mean China will back away from its long-term goal of challenging U.S. financial supremacy. The past week's events may speed up that campaign, Federal Reserve Chair Jerome Powell told a Senate committee Thursday.

A degree of financial decoupling has been occurring on some fronts for years. The U.S. has taken a dim view of Chinese acquisitions in key American industries. Under Trump, it cracked down on Chinese firms listing on U.S. markets. Some firms that managed to do so are reconsidering.

Chinese ride-hailing giant Didi Global Inc., which pulled off a $4.4 billion initial public offering in New York last year (against Beijing’s wishes), plans to transfer its stock-market listing to Hong Kong. Insurer FWD Group Holdings Ltd has filed an IPO application in the same city, after U.S.-China tensions squashed plans for an overseas debut.

From Opinion: Did Xi Jinping Get Played by Putin on Ukraine?

Low Base

Meantime, Beijing is beefing up its economic defenses. Xi has ordered an acceleration of the drive toward self-reliance in key industrial components like semiconductors. For years, Chinese firms have bought up deposits of strategic minerals such as cobalt.

On the financial front, China has set up a digital currency that may soon be ready for cross-border use, and a payment system known as CIPS that offers an alternative to the Swift mechanism that Russia has been partially cut out of.

Those would help Chinese companies and others circumvent the dollar-based system in the event of a sanctions onslaught, which would be likely should Chinese forces attack Taiwan, for instance.

CIPS may get more use soon, as China-Russia transactions increase. But it’s currently a limited vehicle for avoiding sanctions, with just 75 participants — all of them overseas branches of Chinese banks — and no equivalent of Swift’s interbank messaging system, Rhodium Group analysts said in a report Thursday.

The People’s Bank of China has also sought to diversify its foreign-exchange reserves and reduce the weight of U.S. Treasuries, though it remains the world’s second-biggest holder with $1.1 trillion of them.

In all of this, though, the problem for China is that it’s starting from a very low base.

Efforts to build a rival system to the dollar-led one and to encourage broader use of its currency haven’t had much success. The renminbi accounts for just over 3% of global payments via Swift and a mere 2.7% of official foreign-exchange reserves.

Edwin Lai, professor of economics and director of the Center for Economic Development at the Hong Kong University of Science and Technology, says it’s not clear what China can do to speed up the process.

“The international monetary system has a lot of inertia,’’ said Lai, who wrote a book on the yuan titled “One Currency, Two Markets: China’s Attempt to Internationalize the Renminbi.’’

Divided World

Politically, the U.S. and its European allies have mustered plenty of global support for their diplomatic and financial campaign against Russia. In this week’s emergency United Nations debate, 141 voted to condemn Putin’s invasion while 35 countries abstained. Only Belarus, Syria, North Korea and Eritrea voted with Russia, while the rest abstained.

Singapore’s government said it would impose unilateral sanctions against Russia, the first time in decades that the city-state and financial center censured a foreign nation without UN Security Council backing. Traditionally neutral Switzerland has done so as well.

But there are important dissenters. Major emerging-market economies like Mexico and Turkey have declined to sanction Russia. Oil-rich Persian Gulf states like Saudi Arabia are seeking to stay neutral. So is India, the world’s fastest growing major economy, which has long relied on Russia as a weapons supplier.

During Putin’s visit in December, India committed to tripling trade between the two countries, and Russian state oil giant Rosneft signed a major oil supply deal.

That neutral status could bring a payoff for financial centers that manage to stay outside a contest between the West and its main rivals, according to Branko Milanovic, an economics professor at the City University of New York and author of ``Capitalism, Alone: The Future of the System that Rules the World.’’

He argues that the conflict in Ukraine, and the Western response, point toward a fragmentation of capital -– a world in which money can’t move as freely as it has over the past half-century or so. Businesses and the super-rich, along with central banks, will be looking for safe places to store assets — out of reach of governments fighting a financialized war.

Top of Milanovic's list is a place like Mumbai. “It's a big financial center. India is a democratic country. India doesn't have any history of seizing money, nor do they have any incentive to do that. They are not part of the West and, as we see in the Russia crisis, the U.S. cannot dictate India's policy.’’

Ties that Bind

Another view is that it’s precisely the deep economic ties between the U.S. and China that will prevent a wider financial or even military conflict between them.

That’s the case made by Angela Zhang, a law professor and expert on China's legal system at the University of Hong Kong. China has been forced to confront the reach of U.S. sanctions before and has figured out ways to withstand their impact, she says, citing the blacklisting of telecommunications equipment makers Huawei and ZTE who fell afoul of Washington’s sanctions against Iran and North Korea.

China has its own economic ties with U.S. allies. It’s central to a major trade deal, the Regional Comprehensive Economic Partnership, which includes Japan, Australia and New Zealand — but excludes the U.S.

U.S. companies like Apple and Tesla will still want to sell their products in China’s fast-growing consumer markets. Intertwined supply chains — even after recent snarls and the inflation they fueled — illustrate U.S. reliance on China. Mutual need means things shouldn’t escalate too far.

“The Sino-U.S. economic interdependence will be the best safeguard for peace,’’ says Zhang.

‘Significant Blunder’

Some in Washington reckon that China made a miscalculation in aligning itself with Russia – and has been shocked by the force of the U.S.-led countermeasures.

“China has clearly made a very significant geopolitical blunder by throwing its lot in with Moscow on the eve of this catastrophic invasion,’’ says Jude Blanchette, a China expert at the Center for Strategic and International Studies in Washington. “Their ham-fisted response over the past week and a half indicate just how lost they are.”

Others see risks in America’s assertion of its money power. While the U.S. and its allies have wielded “the heaviest financial hammer that we can think of,” it hasn’t stopped Russia’s military attack, says Josh Lipsky, director of the Atlantic Council’s GeoEconomics Center.

The risk in the longer term, Lipsky says, is that the war could end with Russia occupying all or part of Ukraine and installing a puppet government. That would raise questions about how effective this week’s display of American financial might really was.

There are historical reasons for the world to fear economic division into rival camps: It’s what happened in the 1930s, presaging World War II. With the fighting in Ukraine becoming fiercer by the day and Russia threatening to mobilize its nuclear arsenal, discussions of future financial arrangements remain overshadowed by events around Kyiv and Ukraine’s other beleaguered cities.

“Everyone is caught in the geopolitical tensions,” says Andrew Sheng, chief adviser to China’s Banking and Insurance Regulatory Commission. “We are all losers from the present trajectory.”

©2022 Bloomberg L.P.