(Bloomberg Opinion) -- Expect “Pig-gate” to blow over. UBS Group AG’s ultra-rich Chinese clients are unlikely to desert the Swiss bank for local rivals, whatever the level of outrage over language used by its chief economist in a research report last week.

The bank's potential loss of Chinese share-sale mandates isn’t a critical blow: UBS ranks a distant 11th in underwriting Hong Kong IPOs in 2019. (The bank fell behind after a one-year ban by the Securities and Futures Commission over deficiencies in its work on three companies that ran into trouble after listing.) Nor is the loss of bond mandates, such as its exclusion from a sale by state-owned China Railway Construction Corp.

Wealth management is different. UBS is vying for a share of a Chinese private-banking market that was worth a record $24 trillion in 2018, according to Boston Consulting Group. The furor among local brokerages over UBS’s use of “Chinese pig” in a report on pork supply and inflation comes just as the Swiss firm and other foreign banks are muscling in on their turf. Switzerland’s Credit Suisse Group AG, Japan’s Nomura Holdings Inc., and Wall Street giants JPMorgan Chase & Co. and Morgan Stanley are among firms that have received approval to expand or are working toward taking majority stakes in China ventures.

On top of that, Chinese regulators have cracked down on high-risk wealth management products sold by local banks and brokerage firms. That’s leveled the playing field for overseas competitors, which say their stricter compliance guidelines wouldn’t allow them to offer such investments.

Still, it’s outside China where UBS has most to protect. Like all foreign banks, it’s a minnow in the mainland market. By contrast, there’s a treasure trove of Chinese money being managed offshore in cities such as Hong Kong, Singapore and New York, according to a survey by consulting firm Capgemini SE last year. Boston Consulting reckons that market is worth $1 trillion. And here, UBS is hard to beat.

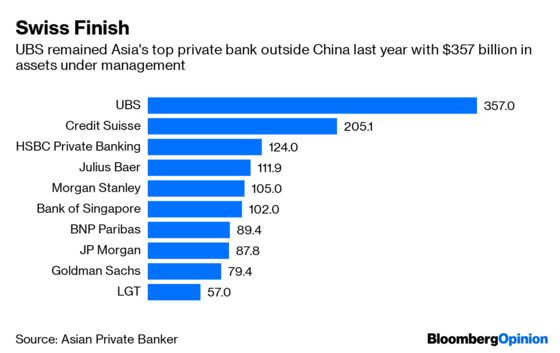

At the end of last year, the Zurich-based bank had $152 billion more in assets under management in Asia outside mainland China than Credit Suisse, its nearest rival. Chinese players don’t rank in the top 10 for bankers to well-heeled individuals in the region, according to data from Asian Private Banker.

UBS took in an unprecedented $16 billion in net new money in the first quarter, driving its Asia-Pacific assets to $405 billion. Credit Suisse collected the equivalent of $4.4 billion. UBS was also the region’s top equities trading house in the region last year, ahead of Morgan Stanley and JPMorgan, according to data from London-based analytics firm Coalition Development Ltd. It’s been Asia’s No. 1 equities house since 2010. That’s key for high-net-worth individuals looking for ideas to trade on.

Money tends to flow to where it earns the most, other things being equal. Also, many clients have bought derivatives from UBS, which can’t be unwound at short notice without heavy penalties. UBS can console itself with the thought that other foreign banks have been able to ride out similar difficulties in Asia. Time is on its side.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.