U.S. Private Debt Default Rate Fell in First Quarter

U.S. Private Debt Default Rate Falls Amid a Resurging Economy

(Bloomberg) -- Defaults in the U.S. private credit market slid in the first quarter as the nation’s abating pandemic triggered a surge in economic growth, and investors hunting for yield grew more willing to finance struggling companies.

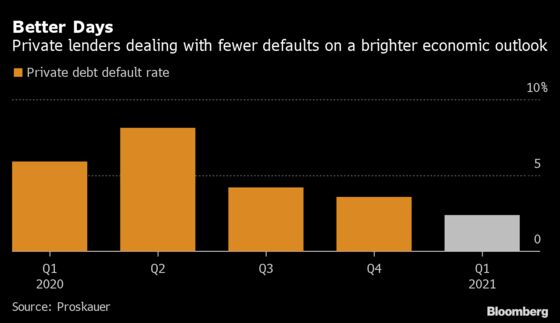

The proportion of loans that defaulted or remained in default fell to 2.4%, according to a private credit market index from law firm Proskauer. That’s down from 3.6% in the fourth quarter and a peak of 8.1% in last year’s second quarter. The index tracks the performance of over 700 active senior secured and unitranche loans representing $131.1 billion in original principal.

“The drop in the default rate this quarter from last quarter is consistent in what we’re seeing in our day-to-day,” Peter Antoszyk, co-head of Proskauer’s private credit restructuring group, said in an interview. “Deal activity is off the charts, and workout and restructuring activity has fallen off.”

As millions of Americans get vaccinated daily, consumer spending is picking up, bringing a jump in sales to companies. Investors are pouring money into private equity and private credit funds, which is helping to sustain borrowers, Antoszyk said. Firms are also seeing a positive impact on businesses that were struggling “due to the efforts that were made by management, sponsors and the private credit community to support them,” he said.

Companies that sell junk debt are seeing similar improvements in credit quality. Defaults on liquid debt for U.S. speculative grade companies, at $5 billion in the first quarter, hit their lowest level since 2018, according to a Friday report from Moody’s Investors Service.

The $975 billion global private credit market, where funds lend directly to companies that traditionally were small or mid-sized, is seeing a raft of larger transactions as money pours into funds. This year, companies including Calypso Technology Inc. and Bourne Leisure Holdings Ltd. have tapped private lenders for more than $2 billion in financing each for buyouts.

“What’s driving lenders going up market into larger deals is the amount of capital that has come into the private credit market that has to be deployed,” Antoszyk said. “Years ago fund sizes were a fraction of what they are today and consequently the deal sizes were smaller – funds now are very large and so you have to deploy capital in chunkier deals.”

©2021 Bloomberg L.P.