U.S. Exceptionalism Begins to Wane in Markets

A role reversal’s potential ripple effect leads market commentary. Plus, swings in sterling, FOMO in China and more.

(Bloomberg Opinion) -- Equity markets in the U.S. soundly outperformed the rest of the world last year, and that trend carried over into 2019. But lately, they’ve ceded ground. If it continues, the implications may be significant.

The MSCI USA Index surged 11 percent between the start of the year and mid-February, compared with a 7.35 percent advance for the MSCI All-Country World Index excluding the U.S. Since then, the USA index has risen just 0.60 percent, versus a 1.39 percent gain for the All-Country index. The amounts aren’t huge, but it’s the shift that’s important, and the timing. It comes amid reports that President Donald Trump is pressing his trade negotiators to come up with a deal with China sooner rather than later, thinking it would give the stock market a boost. But the longer U.S. stocks lag, the more China may feel it has additional leverage in the talks, knowing that Trump is closely watching the stocks market as a scorecard. “As soon as these trade deals are done, if they get done, and we are working with China, we’ll see what happens, but I think you’re going to see a very big spike,” Trump told reporters at the White House on Friday.

Besides the trade implications, global stocks are just more attractive than their U.S. counterparts these days in that they have more potential upside if the recent prognostications by a few prominent Wall Street firms, including Goldman Sachs, that the slowdown in global growth has bottomed prove true. At about 13.3 times this year’s projected earnings, the MSCI All-Country index excluding the U.S. is trading at much cheaper multiple than that 16 times earnings of the MSCI USA Index.

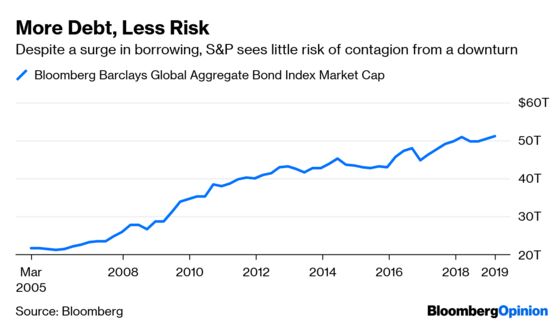

DEBT-CONTAGION RISK DIMINISHES

The amount of total debt outstanding worldwide has surged about 50 percent since the financial crisis. S&P Global Ratings estimates that debt-to-GDP ratios have surged to 231 percent from 208 percent in June 2008, but don’t think the next crisis will be remotely as bad as the last one. For one, contagion risk is lower, according to the ratings firm. It notes that the increase in debt levels has largely been fueled by sovereign borrowing in advanced economies and domestic-funded Chinese companies. “Despite higher leverage, the risk of contagion is mitigated by high investor confidence in major Western governments' hard currency debt,” S&P noted in a research report. “The high ratio of domestic funding for Chinese corporate debt also reduces contagion risk, because we believe the Chinese government has the means and the motive to prevent widespread defaults.” Of course, the ratings firms got it wrong during the last crisis, but there’s reason to believe that the next debt downturn won’t be as severe. New rules and regulations designed to make the financial system safer have largely worked. Outside of the relatively small corporate loan and collateralized loan obligation markets, there hasn’t been a boom in esoteric securities and derivatives such as “CDO squareds,” stuffed with junk-rated debt twice over and even credit-default swaps on that debt. To be sure, there will be a downturn at some point and it will be painful, but the financial system is better equipped to handle it than ever before.

TRADING THE POUND IS FUN

Volatility in the global foreign-exchange market has fallen back to around its lowest levels since 2014. As any good trader will say, it’s hard to make money in such an environment. Then there’s the British pound. A measure of volatility in sterling has shot higher this month, to some of its highest levels since 2016, when the U.K. voted to leave the European Union. Daily swings of greater than 1 percent in the Bloomberg British Pound Index have become commonplace at a time when such moves are almost unheard of among developed-market currencies. The index on Tuesday went from being up 0.77 percent to down 1.01 percent. The volatility is likely to continue after Prime Minister Theresa May’s Brexit deal was rejected once again by Parliament, throwing the country deeper into political crisis. Currency volatility isn’t just important to traders. Excessive volatility can hurt an economy by making it harder for business owners and corporate executives to plan ahead with any confidence. The Organization for Economic Cooperation and Development last week slashed its 2019 growth forecast for the U.K. to 0.8 percent from 1.4 percent as it singled out Brexit as one of the persistent threats facing the U.K. If the U.K. doesn’t secure a deal, it sees a risk of a near-term recession, with “sizeable negative spillovers” on other countries. Purchasing-manager surveys point to growth of 0.1 percent this quarter, matching the weakest pace in more than six years.

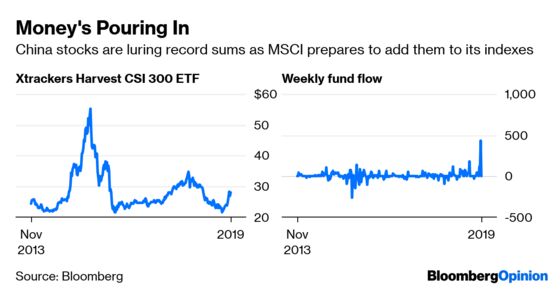

FOMO HAS REACHED CHINA

As stunning as last year’s 25.3 percent drop in China’s CSI 300 Index of equities was, this year’s 24.7 percent rebound is even more jaw-dropping. The question now is, which move was more emblematic of China’s fortunes? History will answer that question, but it’s notable that the Xtrackers Harvest CSI 300 China A-Shares exchange-traded fund just drew its biggest inflow on record, attracting $428 million, according to Bloomberg News’s Srinivasan Sivabalan and Aline Oyamada. At first glance, this may suggest a tremendous vote of confidence in China. A closer look, however, probably suggests the inflow is little more than a case of “FOMO,” or fear of missing out. In what some investors including UBS Group AG describe as the “biggest capital-market change of our lifetime,” China is being co-opted into the global equity and bond markets as the country reforms its previously closed economy. While Bloomberg Barclays Indices is in the process of adding China to its bond measures, MSCI is already stepping up the country’s weighting in its emerging-market indexes after adding mainland shares to the emerging-market category for the first time last year. The increase will occur in three steps this year beginning in May, with the weighting of Chinese A shares ultimately rising to 3.3 percent of the MSCI Emerging Markets Index in November from 0.72 percent now.

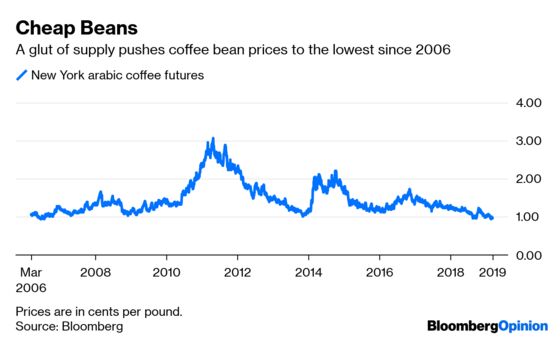

COFFEE IS COLLAPSING

There may soon be relief for coffee lovers after futures dropped as much as 2.6 percent Tuesday to the lowest since 2006 in New York amid a global oversupply. Arabica coffee, favored for specialty drinks such as those made by Starbucks Corp., has been one of the worst-performing commodities in the past year, dropping about 20 percent. Much of the slump has been driven by top producer Brazil, which harvested a record amount of coffee in 2018 and is preparing to collect another big crop this year, according to Bloomberg News’s Nicholas Larkin and Áine Quinn. Heavy rains have replenished soil moisture in the southeast region of Brazil, a top shipper of coffee beans, and helped the nation’s crops while the outlook for output in other producing nations continues to be positive. The U.S. Department of Agriculture in December raised its outlook for world coffee inventories, forecasting stockpiles will rise by 24 percent in 2019.

TEA LEAVES

There has been some concern lately that the Fed may be willing to let inflation run hot for a period of time to make up for all the times it fell below the central bank’s target. Such worries can be seen in the long end of the yield curve, where the difference in yield between bonds due in 10 years and those due in 30 years – a part of the curve that’s less influenced by Fed policy – is the widest since 2017. The Treasury Department’s auction of $19 billion in 30-year bonds on Wednesday may go a long ways toward revealing just how deep the concern about inflation is among bond traders.

DON’T MISS

The U.S. Bull Market Actually Isn’t 10 Years Old: Barry Ritholtz

The Fed's Failures Are Mounting: Danielle DiMartino-Booth

Bond Market Watchmen Keep an Eye on Each Other: Brian Chappatta

Economics 101 at Harvard Will Never Be the Same: Noah Smith

What China's $30 Trillion Credit Pile Won't Say: Anjani Trivdi

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.