Corporate Bottom Lines Can’t Escape Trade War Pain

(Bloomberg Opinion) -- Corporate America avoided an earnings recession in the first quarter. But the escalation of the U.S.-China trade war most likely means that it won’t be able to rely on a repeat performance in the second quarter, and the rest of the year could be a struggle as well.

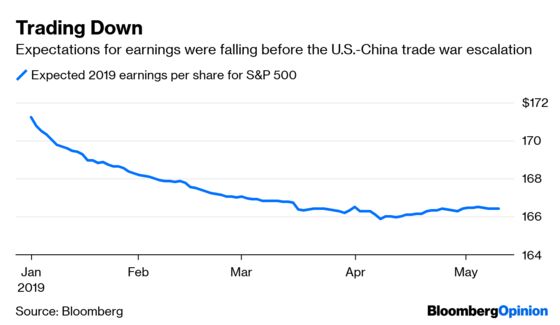

Net income for the S&P 500 rose 0.6% in the first quarter, according to Bloomberg Intelligence, despite predictions from many that they would fall from a year ago. The stock market, however, has slumped lately and was down more than 2.5% on Monday after China said that it planned to retaliate with tariffs of as much as 25% on $60 billion of American imports. The U.S. raised levies on Chinese imports late last week after trade talks collapsed.

Despite the seemingly outsized presence of China in the U.S. economy and the recent focus on trade with the country, sales of American goods there are relatively small, just $130 billion of U.S. exports out of a $19 trillion economy. Tariffs on Chinese imports could slow the economy by raising prices and lowering the sales on other goods, but the impact there is still muted. That’s led some, including me, to conclude that the roughly $1.1 trillion loss in market value of the companies in the S&P 500 has been overdone.

The real problem, though, is not what tariffs will do to sales but to profits. That’s because the globalism and relative free trade of the past two and a half decades has substantially bolstered the bottom lines of corporate America. From the mid-1990s to the mid-2000s, the average net profit margin of U.S. companies was 7.6%. Since then, the bottom lines of corporate America have averaged 10.8% of sales. Some of that increase in profitability came from innovation and lower interest costs. But a good portion of that margin increase, or 2.2 percentage points, is due to free trade and lower taxes, according to an estimate by strategists at Bank of America.

Net profit margins are even higher than that today and are expected to be just more than 12 percent in 2019, largely because of last year’s tax cut. What’s more, Bank of America estimates that lower tax bills overseas account for about 0.7 percentage points of the margin increase. Given the drop in U.S. taxes, that tax savings most likely won’t disappear because fewer companies will have to go overseas to lower their government levies. A full-blown trade war with China will not cut off U.S. companies’ access to lower-cost production countries, either.

But it will certainly hit profits this year, and potentially for the next few if companies are forced to readjust supply chains and reorient to a revamped trade regime. Take away the 1.5 percentage points in profit margins that Bank of America attributes to free trade, and the S&P 500 earnings would fall to $148 a share in 2019. That’s $20 lower than analysts’ current estimates. And that’s if sales don’t fall as well. Not all of globalization’s profit benefit is likely to erode in the next year, and not all of it because of China. But based on that number, and the market’s forward earnings multiple of 16.4, shares could tumble an additional 14%. Trades wars are not only hard to win, they are also, at least for investors, painful to fight.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.