Turkey Burns Bridges With Markets as Costs of Lira Defense Mount

Turkey Burns Bridges With Markets as Costs of Lira Defense Mount

(Bloomberg) -- Turkey is paying the price for its pre-election efforts to tinker with the markets.

As a controversial vote rerun looms, a barrage of interventionist policies by President Recep Tayyip Erdogan’s government has backfired, starving the economy of investment, fueling demand for foreign currency among households and businesses and further undermining the lira.

Despite repeated assurances that capital controls aren’t an option, Turkey has sought to stabilize its currency by reintroducing a tax on foreign-currency sellers and imposing a settlement delay for purchases by individuals of more than $100,000.

“I can’t see any significant flows returning until policy makers become more market-friendly,” said Win Thin, global head of currency strategy at Brown Brothers Harriman & Co. “Turkey has already shown that it doesn’t care if real money can’t hedge properly.”

To stem a run on the Turkish currency without resorting to another interest-rate increase before March elections, authorities made it harder for foreign investors to access lira funding while squeezing the local bond market and leaning on state banks to keep borrowing costs low.

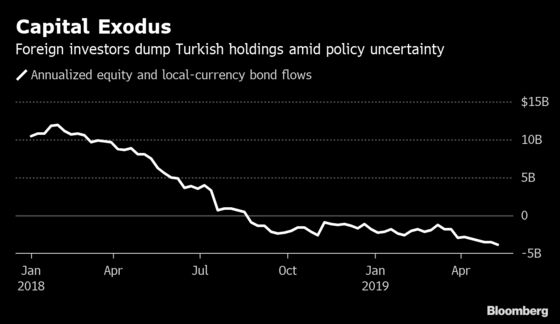

While the measures briefly kept the lira in check after an unexpected drop in central bank reserves, they left investors in a bind: unable to access lira funding to maintain their positions, some foreign investors dumped stock and bond holdings. Others balked at the prospect of runaway inflation.

Since the squeeze, foreign investors have withdrawn close to $2.5 billion dollars from Turkish capital markets, taking this year’s exodus to a net $1.8 billion, the most since 2015.

That’s piling further pressure on the lira, which slumped to a fresh eight-month low against the dollar this month. The currency is continuing to depreciate after wobbling on Tuesday when the central bank rolled back a limited tightening of policy it delivered almost two weeks ago.

The government has also suppressed local-currency borrowing to keep yields in check -- it hasn’t sold a 10-year bond in almost a year despite a ballooning deficit. Instead, it’s loaded up on short-dated lira and foreign-currency debt. Some of the nation’s primary dealers have also been asked to buy more government bonds in debt auctions, according to three people with direct knowledge of the matter.

With the central bank’s reserves running low, Turkey has few options should investors turn decisively against it. Erdogan has ruled out going to the International Monetary Fund.

“The trouble with these measures is that they are stopgap in nature and are not part of a coherent and comprehensive macro-economic program to deal with the country’s economic woes,” Desmond Lachman, a former IMF official who’s now a resident fellow at the American Enterprise Institute, said by email. “As such they do little to restore investor confidence.”

| Read more on recent Turkish policies: |

|---|

At least in public, officials continue to invoke free markets. Treasury and Finance Minister Berat Albayrak has said the liquidity shortage in the swaps market wasn’t engineered by the government. And some analysts remain confident that Turkey’s economy will adjust, despite the political challenges, and investor confidence will eventually return.

Still, Erdogan, who once called himself an “enemy of interest rates,” is increasingly falling back on invective that demonizes banks and foreign investors. Before the March election, he said the currency fluctuation was “a U.S.-led operation by the West to corner Turkey.”

Although he’s eased off pressure on the central bank since its dramatic rate hike of 625 basis points in September, Erdogan said this month he was determined “to reduce exchange rates, interest rates and inflation.”

With markets warped, some investors are now worried Turkey may struggle to attract the funds it needs. As of February, the nation had over $177 billion of foreign-currency debt to roll over during the next 12 months.

The lira has weakened almost 8% against the dollar this quarter, the most in emerging markets, extending its losses for the year to over 12%. Earlier this month, benchmark government bond yields flirted with record highs, approaching levels not seen since a rout in August.

The latest bout of depreciation shows just how damaging the government’s tactics have become, complicating Turkey’s economic adjustment after years of credit-fueled growth. Economists now say this year’s nascent recovery from the first recession in a decade may be short-lived.

“That the currency weakened so much despite a better current account position is a strong sign of the confidence erosion on the part of investors -- both foreign and domestic,” said Inan Demir, an economist at Nomura International Plc in London.

The signs are clear: foreign ownership in the local-currency government bond market tumbled to an all-time low as liquidity dried up. The share of non-residents in the market was at above 13% in early May, down from a peak of more than 28% in 2013, central bank data show.

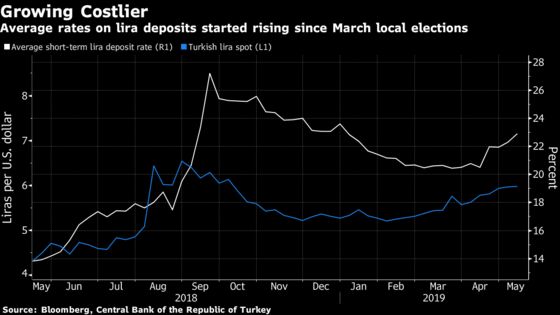

Meanwhile, households and companies seeking a hedge against inflation and political uncertainty rushed to convert their lira savings into dollars and euros. In the three months before the March 31 vote, they bought $20 billion of hard currency, driving holdings to a record.

Several of Turkey’s largest private banks have begun boosting the interest they pay on lira deposits. But after four weeks of selling dollar and euros, households and companies are buying again, a sign the dollarization trend could be hard to reverse.

Despite the fallout, the economy is getting enough of a reboot to eliminate some imbalances -- such as in the current account -- amassed during years of big spending.

“The economic adjustment is happening,” said Viktor Szabo, fund manager at Aberdeen Standard Investments in London. “Many policy errors were made, but I still don’t see Turkey doomed.”

--With assistance from Taylan Bilgic.

To contact the reporters on this story: Cagan Koc in Istanbul at ckoc2@bloomberg.net;Constantine Courcoulas in Istanbul at ccourcoulas1@bloomberg.net

To contact the editors responsible for this story: Onur Ant at oant@bloomberg.net, ;Lin Noueihed at lnoueihed@bloomberg.net, Paul Abelsky

©2019 Bloomberg L.P.