Tsunami of Fund Inflows Seen Helping Mortgage Debt Fight the Fed

Tsunami of Fund Inflows Seen Helping Mortgage Debt Fight the Fed

(Bloomberg) -- Money managers have been a major source of demand for mortgage-backed securities over the last two years -- and the cash their funds have pulled in this year may help offset the impact of the Federal Reserve’s decision to reduce its holdings of the bonds.

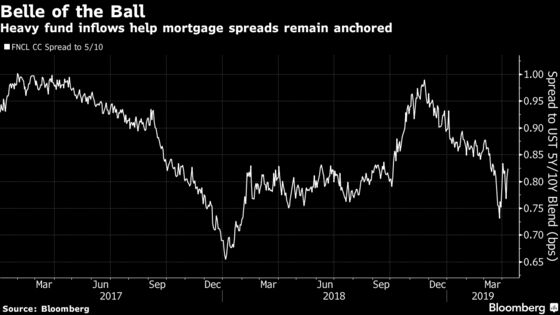

These heavy inflows “make money managers forced buyers, not outright relative value driven, and acts as a counter against the Fed MBS runoff while helping anchor mortgage spreads,” Satish Mansukhani, the leader of Bank of America Corp.’s MBS strategy team, said in an interview with Bloomberg.

Mortgage-related funds have seen inflows of cash for thirteen straight weeks, the longest stretch since the 24-week run that ended in June 2016, according to Lipper U.S. Fund Flows data. That’s given money managers at least $6.32 billion more to invest so far this year, a shift from the $7.61 billion that was pulled out of their funds in 2018 when investors were concerned about the potential impact of rising interest rates.

Such money managers hold about 14 percent of the outstanding mortgage-backed securities, according to Bank of America. Due to the multiplicity of different funds and mandates, most analysts “back into” their money manager forecasts for their aggregate demand, factoring in available data for other MBS holders. So even with the inflows, Mansukhani estimates money managers will only buy about $248 billion in 2019, down from $275 billion last year.

“The reduced forecast does not mean we feel there will be less sponsorship, but that there is not enough product for them to buy, which means spreads should remain anchored,” he said.

Since money manager demand “is always a tricky thing to gauge” because some funds are not solely mortgage-focused, Matthew Jozoff’s MBS team at JPMorgan Chase & Co. focuses on the top fourteen funds that are primarily devoted to the sector and view their weightings versus the Bloomberg Barclays U.S. Aggregate bond index.

“Money managers are pretty overweight at the moment, with a 35 percent weighting in mortgages versus 28 percent in the index, the most since around 2012” and they may not be inclined to add more, he said in an interview with Bloomberg.

A bright spot is for potential MBS buying from real-estate investment trusts, Jozoff said, as they have “issued new equity and they may be one of the most favorable of all demand sources, though they are still a relatively small source of demand.”

In fact, during the first quarter REITs issued about $2 billion in equity with estimated net MBS purchases of about $10 billion, according to Barclays Capital. Its analysts recently wrote they would not be surprised if REITs continue to tap the equity markets and as such, expect them “to continue to be net buyers of MBS over the next few months.”

Yet, because REIT demand is materially smaller than money managers it is the latter that is depended upon to fill the demand void left by the Federal Reserve’s withdrawal from the mortgage sector.

“Money manager demand should remain strong although slightly down from what we saw in the first quarter. We still have a favorable outlook on mortgages,” Dan Hyman, a managing director at Pacific Investment Management Co. said in an interview with Bloomberg.

To contact the reporter on this story: Christopher Maloney in New York at cmaloney16@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, William Selway, Rizal Tupaz

©2019 Bloomberg L.P.