Trump’s Trade War Revives Xi’s Silk Road

China’s global infrastructure initiative was in trouble a year ago, but emerging countries are signing on again.

(Bloomberg Opinion) -- China’s Belt and Road Initiative is seeing a revival lately, after a year of rumblings from developing nations that President Xi Jinping had set them a debt trap in the guise of funding massive infrastructure projects.

In the first half of this year, Commerce Ministry data show, Beijing signed about $64 billion in new, mostly construction contracts, a jump of 33% from 2018. Back then, Malaysia was complaining of deals reached under a scandal-stricken ousted leader and Indonesia was gearing up for elections in which both sides played up nationalist credentials.

And now? Emerging markets are coming back to the negotiating table. Malaysia restarted the $20 billion East Coast Rail Link in July, reversing a decision to terminate it. In Indonesia, the controversial Jakarta-Bandung high-speed railway plan is back on track after more than two years of delays, and new power plant and housing projects have been approved.

What caused this change of heart?

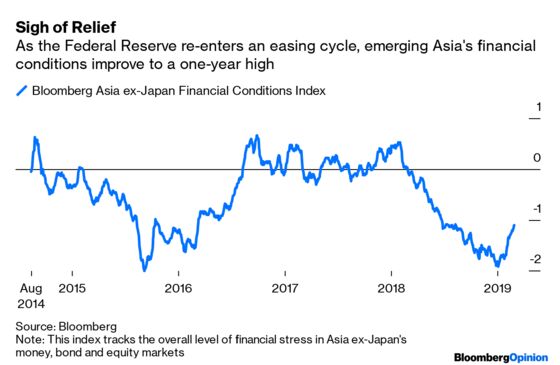

For a start, financial conditions in emerging Asia, which still follows the Federal Reserve’s easing cycle, have improved to a one-year high. With the Fed cutting interest rates again, emerging markets can feel a bit more relaxed about taking on more debt.

More importantly, as world trade growth plunges to a decade low, infrastructure spending is the only way left to lift emerging economies. Where will the money come from? China is offering.

Beijing was lucky that its economy blossomed in an era when international trade was barely challenged as a global policy. At its peak in 2007, China’s current account surplus exceeded 10% of GDP. Despite all that net income from abroad, China still had to pile trillions of dollars of debt on state-owned enterprises to get to its glitzy high-speed trains and skyscrapers today.

Beijing had no choice but to deploy some of its excess capital abroad. By 2014, the year China started to spend money on BRI, credit creation had become so inefficient at home that to generate $1 in GDP, China had to spend $9 in new fixed-asset investment, by the National Bureau of Statistics’ estimates. The incremental-capital-to-output ratio should be somewhere between 2 and 4.

Much of the emerging world wasn’t as lucky in its timing as China. As the trade war escalates, even Vietnam, seen as one of the main beneficiaries, hasn’t gained much. Last year, its current account surplus came in at just 2.7%, below 3% in 2016. Large-scale financing is even more more difficult for countries with twin current-account and fiscal deficits such as Indonesia.

The U.S. likes to portray China’s globe-encircling infrastructure ambition as building a new empire, and it may look that way if you go by the sprawling map of countries included in Xi’s blueprint.

But given an option, China would have much preferred investing in the U.S. instead of, say, Pakistan. At its 2016 peak, the U.S. accounted for roughly one-third of China’s overseas investments, according to China Global Investment Tracker, which looks at deal sizes of $100 million and above. Since President Donald Trump took office, though, Chinese investments in the U.S. have plunged as Washington took a more skeptical view of acquisitions from the country.

Money speaks volumes. In a January survey of more than 1,000 respondents, mostly academics and bureaucrats in Southeast Asia, 73% believed that China held the most economic sway in the region. Close to half considered China as having the most political influence in Southeast Asia versus 30% for the U.S.

Washington likes to think it still wields influence in the geopolitical domain, but it’s increasingly seen as indifferent to the wider world. As easy money starts flowing again and Trump shifts policies, the U.S. is losing key emerging markets allies.

Back in April, in its second Belt and Road Forum, President Xi sounded chastened about his China Dream ambitions to make the country great again. But he may soon be feeling triumphant.

To contact the editor responsible for this story: Patrick McDowell at pmcdowell10@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.