(Bloomberg Opinion) -- The U.S. Federal Reserve’s next meeting is still five weeks away, and President Donald Trump is already talking the economy into a recession in his campaign for lower interest rates. Markets shouldn’t take his latest salvo too seriously.

The Treasury Department formally labeled China a currency manipulator for the first time since 1998 after Trump took to Twitter to castigate the country for allowing the yuan to weaken beyond the psychologically important level of 7 per dollar. S&P 500 futures dropped as much as 1.9% after the decision, with the index having closed 3% lower in regular trading.

It’s not hard to understand why Trump is feeling vexed. Since Treasury spared China the currency-manipulator tag in late May, the yuan has weakened 2.2%, the most among countries on a U.S. watch list. But even he must know that this politically charged label is all bark and no bite.

All Treasury Secretary Steven Mnuchin can do is to engage with the International Monetary Fund to eliminate the “unfair competitive advantage created by China’s latest actions.” Trump has already slapped higher tariffs on Chinese imports.

The IMF won’t be enthusiastic to take action. The yuan is broadly fairly valued, according to the fund’s latest external sector report published in July, which found that the U.S. dollar is indeed the most expensive among the two dozen or so currencies it considers. If the U.S. is really looking for a manipulator, Mnuchin had better give Singapore a call.

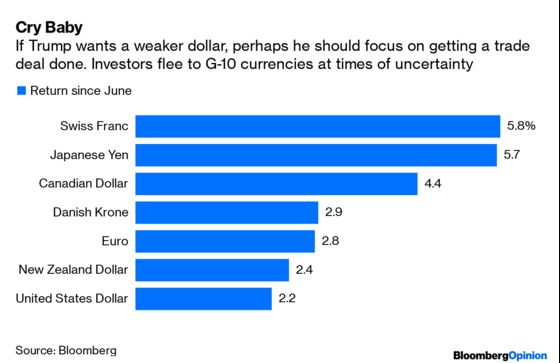

Truth is, global investors naturally flee to the haven of developed-nation bonds when the trade war escalates. If Trump is feeling the pinch from a stronger dollar, then what about the Swiss franc or the Japanese yen? Since June, they’ve appreciated more than 5% against the yuan. What’s more, the People’s Bank of China has been conspicuously absent in the world’s race to cut interest rates. Things could have been a lot worse.

What the president can do is use the currency-manipulator label and ensuing market jitters as a tool in his drive for rate cuts. Traders now see 44% probability of a half-percentage point cut at the Fed’s Sept. 18 meeting, up from only 15% a week ago. A mild, “mid-cycle adjustment” like last week’s 25-basis-point cut isn’t what Trump wants. Just read his social media posts: The president’s first response to the yuan slipping past 7 to the dollar was to berate the Fed.

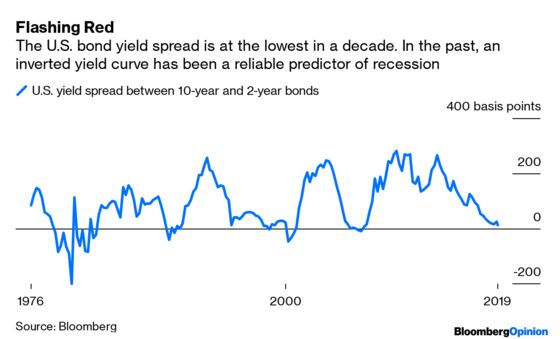

The Fed has become hostage to politicians and traders. With the spread between U.S. two-year and 10-year bond yields at its lowest since 2007, a recession is looming, traders say.

For China’s part, it absolutely doesn’t care about the new label. As I’ve written, the government has wised up after almost two years of trade war and now questions how sincere Trump is about reaching a deal. Beijing has many tools to shore up the currency’s value if it wants: Issuing higher-yield bonds, for example, is a well-tested tactic to pull the offshore yuan higher. All China wanted to do with Monday’s weak fixing was to send a warning shot to Trump.

As Beijing well knows, sometimes a leader’s belligerence toward other nations is really aimed at an audience at home.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.