(Bloomberg Opinion) -- It was always dumb for Donald Trump to take credit for the stock market, and put rising share prices at the center of his case for re-election. That should have been clear from the outset, and is beyond doubt now that U.S. stocks have sunk into a bear market only months before he must face voters.

The stock market and a president’s chances of re-election aren’t necessarily linked. But Trump’s fate is now inextricably tied to the market’s, and both are prone to the pandemic virus. As he confronts what will probably be the toughest stretch of his political career to date, he might be well advised to take stocks as a good monitor of his performance. Unless he can somehow deliver a successful response to both the human and economic effects of the coronavirus, a protracted bear market is likely. And if the market deeply dislikes measures to deal with the virus, that might conceivably be good reason to change course.

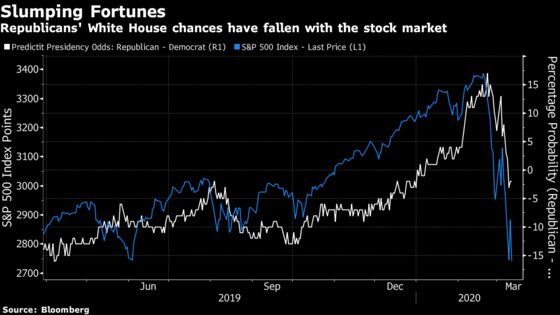

Over the past year, the link between the market and Trump’s perceived chance of re-election (which can be most easily gauged by prediction markets) is startlingly close. Stock markets tend to reflect the prevailing mood in society, so this isn’t greatly surprising, and Trump is regarded as far more market-friendly than several of his potential Democratic rivals. Over the past year, stocks rose with the growing chance of a Trump victory, as expressed by prices on the Predictit market — and in the last two weeks they have tumbled together. The Democrats are now thought slightly more likely to win:

This shows the folly of taking credit for the rally. The president cannot control the market — indeed, others have far greater influence over it. Moreover, he took office at a time when stocks were already very expensive. That made it highly unlikely that the stock market would perform well for him. Even when stocks were at their peak three years ago, the performance on his watch was nothing special.

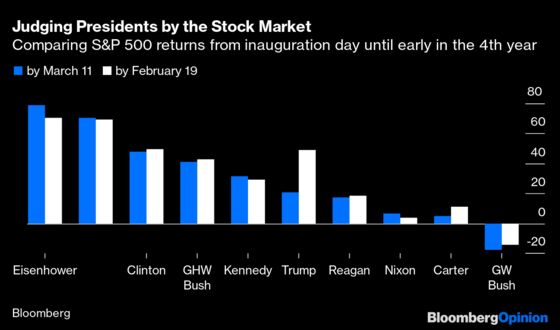

This chart shows the S&P 500 from inauguration day until Wednesday’s close, in white, and compares it with the equivalent period for the first terms of the nine other presidents to be elected since the war. (I excluded Johnson and Ford, who took over as vice presidents). Trump is in white.

As that chart looks like spaghetti, here are the returns in simple bar chart form. The blue columns show performance from inauguration day through March 11, while the white columns show performance to Feb. 19, still not even a month ago, when the S&P 500 Index made its last all-time high. At that point, Trump was roughly level with Bill Clinton and lagged only Eisenhower and Obama, both of whom took office near the bottom of major bear markets. After the sell-off , Trump has now dropped in the rankings behind the first President Bush, and JFK :

If this swift reversal of fortune doesn’t reveal the foolishness of measuring yourself by the stock market, note further that Trump still has better returns than the two Republican presidents he would most like to emulate. Presidents Reagan and Nixon both won re-election in a landslide, and both oversaw thoroughly anemic stock-market returns early in their fourth year. George W. Bush, the only president sitting on a decline in March of his fourth year (having taken office just as a speculative bubble was bursting), also won a second term.

The fact that three conservative presidents prevailed in their re-election bids despite poor stock-market performance shows that politicians shouldn’t target share prices. They aren’t, in themselves, that relevant to voters. But now that Trump has taken credit for the gains, he will find it difficult to avoid political responsibility for losses.

There is a decent chance that the market will rebound strongly into the election — that is exactly what a number of major Wall Street firms, including Goldman Sachs Group Inc. and Citigroup Inc., are currently predicting. The argument is that after the twin shocks of the virus and falling oil prices cause a profits recession in the first half, a natural rebound in earnings as life returns to normal will allow stocks swiftly to settle into a new bull market.

That scenario isn’t far-fetched, but it is hampered by the very high valuations that Trump inherited, and that have grown even higher under his presidency. Sparking a pre-election stock market revival will require a strong response to the human effects of the virus, in addition to well-targeted financial measures to prevent the twin shocks from metastasizing into a credit crisis. The American corporate sector is heavily leveraged, and credit investors are already signaling concern about the risks of bankruptcies and forced sales.

This will be difficult. The countries to have the best success in controlling the virus to date, Hong Kong and Singapore, are both cities with relatively authoritarian governments. It will be hard to copy their methods in the far larger and more democratic U.S.

When it comes to stimulating the economy, the American system of checks and balances could again put Trump at a disadvantage. The U.K. this week announced in quick succession an emergency 50-basis-point rate cut by the Bank of England, and the biggest fiscal expansion in almost three decades. That was well received by the markets.

But the U.K. has a newly elected prime minister with five years left of his mandate, and a strong majority in parliament. Policy is virtually a matter of deciding what to do and then doing it, untroubled by the opposition. Coordination is far harder in the euro zone. The European Central Bank has less freedom of movement and fiscal policy must be coordinated by a patchwork of finance ministers across the continent.

If Trump wants to spark a renewed bull market before the election, he will need to negotiate a complicated stimulus package with a House of Representatives controlled by Democrats desperate to ensure his defeat — but also desperate not to seem obstructionist. He also needs to come up with exactly the right measures to avert credit problems — a feat that proved mighty difficult in 2008.

If he can pull this off, the president should win both a V-shaped stock-market recovery and his own re-election. But he would have been better off if he had never drawn attention to the stock market in the first place.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

John Authers is a senior editor for markets. Before Bloomberg, he spent 29 years with the Financial Times, where he was head of the Lex Column and chief markets commentator. He is the author of “The Fearful Rise of Markets” and other books.

©2020 Bloomberg L.P.