Trump May Have Made Himself the Recession's Scapegoat

(Bloomberg Opinion) -- The markets have spoken. If they are to be believed, the potential for a U.S. recession has never been greater in the post-crisis era than it is right now.

That’s a problem for President Donald Trump because after the events of the past few days, it should be clear that he has effectively forfeited the ability to use the Federal Reserve as a scapegoat for any economic slowdown, an angle he was clearly prepared to play.

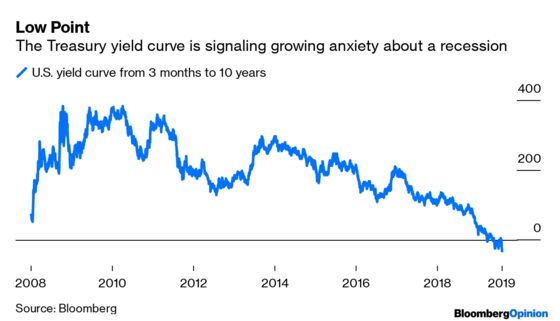

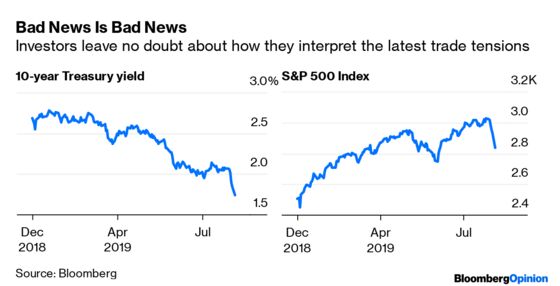

Consider the three-month, 10-year U.S. yield curve, which, when inverted, is widely considered a signal of an impending recession. It inverted by as much as 32 basis points on Monday, the most since 2007. But what’s more notable is how it got there. On July 31, when the Fed decided to lower its benchmark short-term rate for the first time in more than a decade, the spread only moved a few basis points. But on Aug. 1, when Trump announced additional tariffs on Chinese goods, it spiraled down about 14 basis points. On Monday, as China detailed plans for retaliation, it fell as much as 10 basis points.

Moves of that magnitude don’t happen often. Meanwhile, the benchmark 10-year yield itself tumbled 14 basis points to the lowest level since before Trump was elected, while the S&P 500 fell the most this year. Clearly, the latest escalation in the U.S.-China trade war has spooked investors. Some even fear that easier monetary policy from the Fed won’t be enough to reverse the damage, given the already shaky status of corporate earnings.

It truly didn’t have to be this way. Fed Chair Jerome Powell was convinced that the central bank’s rate cut was a mere “mid-cycle adjustment” that made sense as an offset to trade tensions, which he said were causing “ongoing uncertainty” among the central bank’s business contacts. In his opening statement, he said: “After simmering early in the year, trade policy tensions nearly boiled over in May and June, but now appear to have returned to a simmer.”

Less than 24 hours later, Trump ratcheted up the temperature. That fueled speculation that he made the move in response to the Fed cutting interest rates by less than he wanted. If this was a calculated move on Trump’s part, he might have underestimated how his decision could backfire.

To many market observers, the Fed didn’t have to lower interest rates last month. Powell even said that the central bank was as close to its dual-mandate of low unemployment and stable prices as ever. I argued that officials cherry-picked their data, but coming out of the Federal Open Market Committee decision, it seemed quite clear that the rate cut was mostly meant as a way to neutralize any lingering effects of Trump’s various trade skirmishes on business confidence.

Trump should have taken the victory. After all, he had spent months hammering the Fed for raising interest rates too quickly and for continuing with “quantitative tightening,” which the central bank also ended last week. He got what he wanted, all the while preserving his argument that the economy would be doing even better if Powell hadn’t fumbled it. He had his scapegoat.

Now, Trump risks absorbing all that blame himself. To be sure, it’s still too soon to say a U.S. recession is coming anytime in the near future. And while stock markets took a serious beating on Monday, the S&P 500 is still up more than 20% from its lowest point on Dec. 26. There’s no way to know for sure that this round of tariffs is “the one” that topples the global economy. The number of head fakes, both positive and negative, is too high to count at this point. Plus, investors have it in the back of their minds that Trump will strike some semblance of a deal before November 2020 to boost markets — and his re-election prospects.

That’s a dangerous scenario to count on, especially because it takes two to strike a deal. China may see little upside to giving Trump a victory ahead of the presidential elections or might even prefer to gut it out and negotiate with a potential Democratic successor. This has always been a risk, of course. But as Powell pointed out, it had seemed as if the two sides were coming closer to an agreement. Trump shattered that illusion in one fell swoop. To escalate things further, the U.S. Treasury Department, "under the auspices of President Trump," officially labeled China a currency manipulator late on Monday.

My Bloomberg Opinion colleague Ramesh Ponnuru made the point recently that the Democratic presidential candidates faced a challenge in talking about the economy because it has been so strong. On top of that, as Powell likes to point out, sustaining the expansion has allowed the recovery to reach a broader subset of Americans.

Trump’s decision to impose further tariffs on China provides an opening for Democratic candidates. Indeed, California Senator Kamala Harris already did so, before this latest escalation. “Jerome Powell just dropped the interest rates and he admitted why — because of this so-called trade policy that this president has, that has been nothing more than the Trump trade tax,” she said on July 31. The president could have easily brushed off the attack at the time. But now?

One bad day in the markets doesn’t mean a recession will follow. But it does speak to whom investors fear the most when it comes to mishandling the economy.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.