Treasuries Rally, Risk Suffers After Virus Panic Overshadows Fed

Treasuries Lead Rally With Fed, BOJ Raining Cash Across Markets

(Bloomberg) -- Treasuries rallied and riskier bonds slumped with stocks after the Federal Reserve’s slashing of interest rates to near zero did little to placate markets.

The surprise policy move by the Fed led an effort by global central banks to provide liquidity for stressed markets. Yet in Europe, Germany’s haven bunds failed to gain traction, while Italian and Spanish bonds slid. The region’s equity markets slumped to their lowest in more than seven years, adding to a sense of panic among investors trying to gauge to scale of the economic impact of the coronavirus.

“The market’s initial response to this shock-and-awe panoply of policies has, however, followed the now familiar pattern of deeming these actions to be more symptomatic of the seriousness of the threat rather than promising anything in the way of a solution,” said strategists at Rabobank International, including Richard McGuire, in a client note Monday.

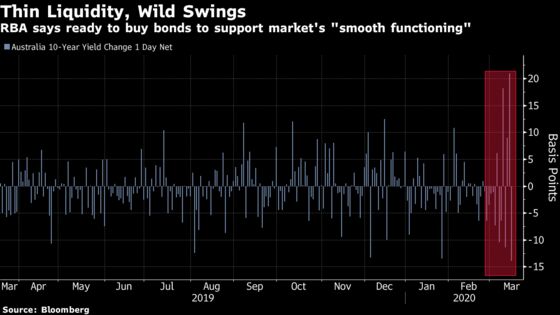

Just hours after the Fed’s second emergency rate-cut this month, the Bank of Japan announced plans to buy more corporate bonds and commercial paper, while the Reserve Bank of Australia said it stands ready to buy government securities. The Bank of England is ready to take further action whenever needed, its new Governor Andrew Bailey said Monday.

The efforts, coming after a statement on Sunday by major central banks, underscored how the coronavirus pandemic is leading to worries about a repeat of the last financial crisis. The question is whether these moves will be enough to ease a global credit crunch and keep markets functioning.

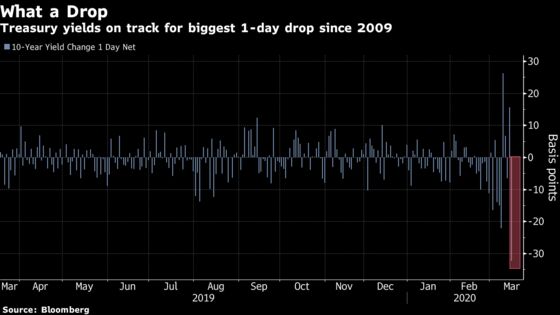

Treasury 10-year yield plunged by as much as 34 basis points to 0.62%. New Zealand’s yields also sank after the central bank slashed its rates by 75 basis points in an emergency move. Italy’s 10-year yield climbed as much as 32 basis points to 2.1%, while the German equivalent was little changed.

Read: Funding Market Stress Worsens Despite Emergency Fed Action

The premium to borrow dollars in some cross-currency markets briefly spiked higher on Monday. The dollar-yen three-month cross-currency basis swap, an indication of how much it costs to borrow the greenback, surged to its widest on record, before paring the move in European hours, according to data going back to 2011 compiled by Bloomberg.

“They can’t allow funding problems and liquidity to seize up in credit markets, which can turn into a financial crisis if left unchecked,” said George Boubouras, head of research at K2 Asset Management. “They’re desperate to stop it.”

The Fed’s key rate is now in a range of 0% to 0.25%, matching a record low last seen in 2015. Along with other measures, the U.S. central bank also pledged to boost its bond holdings by at least $700 billion.

“The Fed measures make it easy for depository institutions to access very cheap credit, but it is unclear how much this credit easing will extend to corporates and households,” said Steven Englander, Standard Chartered Plc’s head of North America macro strategy.

The BOJ, which kept its rates unchanged, said it will raise the upper limit to buy commercial paper and corporate bonds by two trillion yen ($19 billion), while giving zero-interest loans against corporate debt. The RBA will be conducting one-, three- and six-month repurchase operations for as long as markets needed, it said. It also plans to introduce more policy measures on Thursday.

Other Asian central banks also jumped into action. The Bank of Korea cut rates by 50 basis points, while the Reserve Bank of India is injecting liquidity into markets.

The bond market is coming off one of its wildest stretches ever, featuring a dive to record low Treasury yields and the widest weekly range in 30-year rates in the past two decades.

It also featured indications of severely impaired market liquidity including wide bid-offer spreads for all but the newest Treasuries, and broken relationships between cash bonds and the futures contracts that reference them.

Following the Fed cut, the potential for U.S. bonds to join the world’s almost $12 trillion pile of negative-yielding debt now looms large. Yields on Treasury bonds expiring in the next three months were getting quoted at slightly negative levels during Asia hours.

“U.S. bond yields are at risk of going to zero, and Australia could test negative levels too,” said Shane Oliver, head of investment strategy at AMP Capital Investors Ltd. Central banks “can’t do anything to stop the coronavirus from disrupting the economy -- it’s all about keeping markets functioning as best they can.”

The Fed acted aggressively last week to ease strains in the Treasury market through massive injections of liquidity and broader purchases of U.S. securities, in a measure reminiscent of the quantitative easing it used during the financial crisis.

“My initial take is that the QE measures ought to significantly help liquidity in the Treasury market, which has no doubt been struggling of late,” said Jonathan Cohn, a rates strategist at Credit Suisse Group AG. “The knock-on effect will be lower rates and significant richening in cash versus swaps and futures.”

--With assistance from Emily Barrett, Elizabeth Stanton, Chikafumi Hodo and Stephen Spratt.

To contact the reporters on this story: Ruth Carson in Singapore at rliew6@bloomberg.net;Liz Capo McCormick in New York at emccormick7@bloomberg.net;Anooja Debnath in London at adebnath@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, ;Benjamin Purvis at bpurvis@bloomberg.net, Tan Hwee Ann, Neil Chatterjee

©2020 Bloomberg L.P.