Treasuries at 3%, Sell Tech: Traders Update Hawkish Fed Bets

Traders are now busy updating playbooks on what a more hawkish-than-expected Federal Reserve would mean for markets.

(Bloomberg) -- From Treasury yields hitting 3% to shorting technology stocks, traders are busy updating playbooks on what a more hawkish-than-expected Federal Reserve would mean for markets.

Mizuho Bank Ltd. is urging investors to sell bloated U.S. bond portfolios, on the risk 10-year yields climb to as high as 3%. Goldman Sachs Group Inc. strategists are favoring European stocks, while AllianceBernstein says euro corporate bonds will beat dollar ones. Invesco Asset Management sees technology shares coming under more selling pressure.

“Repositioning will be a no-brainer now with yields likely to climb higher, quantitative tightening quickening and equity sectors suffering nosebleeds as the Fed comes out swinging,” said Vishnu Varathan, head of economics and strategy at Mizuho. “The key thing to weigh here is the acceleration in the Fed’s tapering and whether markets are right with their pricing of hikes.”

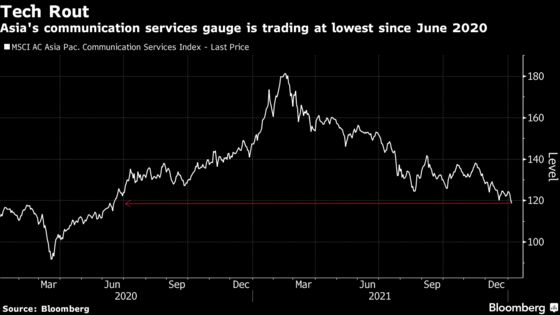

A Treasuries selloff extended on Thursday, also pushing yields from Australia to Germany higher after minutes from the Fed’s December meeting showed policymakers considering hiking earlier than expected and mulling a runoff of its balance sheet. Equities slid around the world, with high-priced technology shares absorbing the worst losses.

However, U.S. stock futures hinted that sentiment is starting to stabilize. Contracts on the S&P 500 edged higher as of 12:00 p.m. in London. The 10-year Treasury yield rose three basis points to 1.74%, its highest since April.

Market participants are zeroing in on a key component of the minutes: that policymakers discussed shrinking their balance sheet soon after the first hike. It’s a more aggressive approach than first thought, spurring re-thinks on how best to position for rising U.S. borrowing costs.

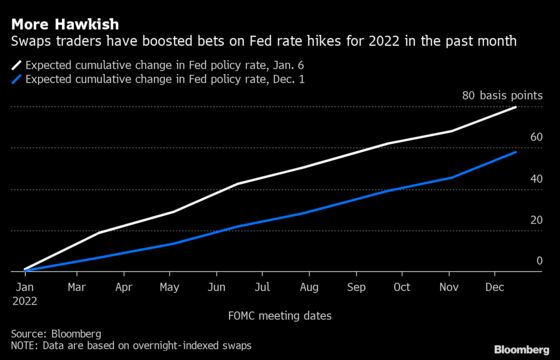

Swaps traders now see a 76% chance the Fed will raise the policy rate by 25 basis points in March, compared with just 26% at the start of December. Real yields -- those adjusted for inflation -- have also jumped 20 basis points in just four days at a pace not seen since the height of pandemic fears in March 2020.

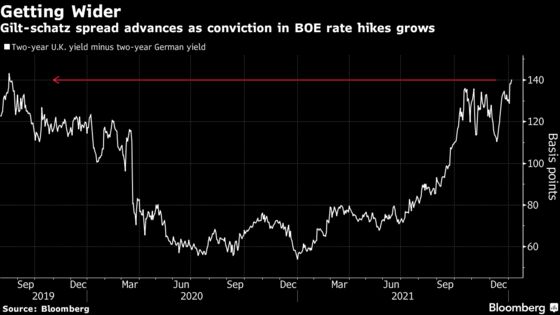

Benchmark U.S. yields should climb toward 2% as markets move into the second half of the year, said Andrew Ticehurst, a rates strategist at Nomura Holdings Inc. in Sydney. In Europe, the spread between U.K. and German short-end rates is climbing as investors expect the European Central Bank to trail the Fed and Bank of England in raising rates.

Sell Asia

Currency traders are looking to pressure points in Asia, with the Thai baht plunging 1%, while the Australian dollar tumbled. By contrast South Africa’s rand shrugged off early weakness to gain 1%.

“Emerging-market economies with lower vaccination rates, weaker external and fiscal balances like the Philippine peso, Thai baht, Indonesian rupiah, Indian rupee are likely to be at some risk,” said Wai Ho Leong, strategist at Modular Asset Management in Singapore.

More “tech-sensitive” currencies such as Korea’s won will also come under pressure given the selloff in the U.S. sector, according to Mitul Kotecha, strategist at TD Securities in Singapore.

On the fixed income front, DBS Bank Ltd. sees Thai bonds underperforming on a widening policy differential with the U.S. It likes Chinese bonds as a haven, where benchmark yields have dropped in the past month on expectations for loose monetary policy while all other Asia Pacific yields climbed.

“Thailand is expected to be one of the laggards on monetary normalization and therefore, a widening policy differential against U.S. Fed would weigh on Thai bond returns,” said DBS strategist Duncan Tan. “Indonesia bonds, being higher-beta, are typically more sensitive to increases in U.S. rates, although any weakness will likely be contained due to better defenses this time around.”

Stock Bets

Bets on equities are more varied.

Goldman Sachs strategists said European stocks are a good place to seek shelter from turmoil. While European stocks have consistently underperformed U.S. peers, now “the scales are tipping slightly in favor of Europe,” they wrote.

In Japan, higher long-term U.S. yields should have a positive impact on the nation’s banks but become a drag on companies with operations in the U.S., according to Tomo Kinoshita, a global market strategist at Invesco Asset Management in Tokyo. Technology shares could also come under selling pressure, given their past relationship with yields, he added.

Small cap companies could become targets for short sellers as funding stresses from higher U.S. interest rates mount.

“The risk is palpable if the Fed is seen as tightening the screws too quickly,” said Ilya Spivak, head of greater Asia at DailyFX.

Others are jumping on the opportunity to buy beaten-up names.

“I still like select industrials in Japan that are underappreciated beneficiaries in automation, electric vehicles etc,” said Joshua Crabb, a portfolio manager at Robeco in Hong Kong.

For HSBC Holdings Plc’s Herald van der Linde, Asia Pacific head of equity strategy, rotating into China and Indonesia makes sense because “valuations are low and we see good growth in 2022.”

European Credit

The different trajectories of the European and U.S. central bank is also driving sentiment in European corporate bonds.

“Euro-denominated credit looks more attractive than U.S.-dollar credit,” said John Taylor, a portfolio manager at AllianceBernstein in London. “The fundamentals are fairly solid, so this isn’t a question of default rates suddenly spiking, more that general credit spreads could adjust wider as the central banks are less friendly.”

©2022 Bloomberg L.P.