Trade Wars Suggest We May Be Forgetting the Economic Lessons of 2016

Trade Wars Suggest We May Be Forgetting the Economic Lessons of 2016

(Bloomberg) --

The big political economy lesson of 2016 was to beware of the aggregate numbers. Any economy can look OK at the top level. But down below someone somewhere is probably hurting and getting grumpy about it. And in politics — and particularly American politics — when you marry grumpiness and geography it can be more consequential than top-line economic numbers.

That case of “regional disparities” was the common explanation offered for political earthquakes from Brexit to Donald Trump’s election in 2016, and why “elites” in distant capitals were caught wrongly shrugging off the sharpening of the pitchforks in places like Sunderland and Youngstown. It’s why we now have so many conferences about “inclusive” growth.

But in the U.S. in particular it’s worth asking whether that lesson has been forgotten by some in the current ruling class. More pertinently, the question is are Trump and his aides falling into the same trap they accurately identified and exploited in 2016?

That’s why this week’s grim ISM number, which showed U.S. manufacturing contracting at its worst rate in a decade thanks in large part to Trump’s trade wars, matters so much and why markets were right to be so unnerved by the data.

Trump may repeatedly insist the U.S. economy is the greatest it has ever been, but the manufacturing sector is currently in a de-facto recession. More importantly it’s a sectoral recession that many economists believe the president’s trade policies contributed to, and that’s starting to affect the labor market in important swing states like Pennsylvania and Wisconsin.

It’s still early, of course, and the impeachment inquiry launched in recent days may upend everything anyway. But if the U.S. economy — or key components of it at least — continue on the track they are on now that could have consequences for Trump and his re-election bid in 2020.

Which makes what’s happening in U.S. manufacturing arguably the most consequential issue now facing the world’s largest economy and why it’s the subject of the first episode of the new season of Stephanomics, the podcast of Bloomberg Economics head Stephanie Flanders.

You can also read the Bloomberg Businessweek feature on which it was based here.

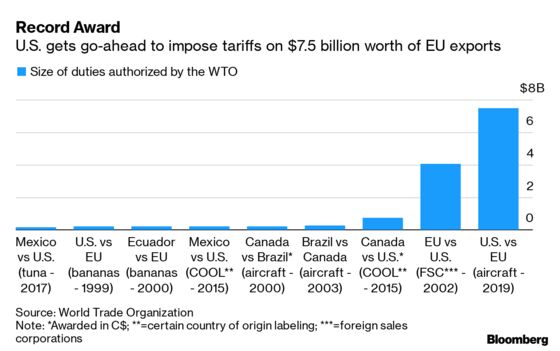

Charting the Trade War

The World Trade Organization gave Trump the go-ahead to impose tariffs on as much as $7.5 billion worth of European exports annually in retaliation for illegal government aid to Airbus. Wednesday’s award is the largest in WTO history — nearly twice as large as the previous record of $4.04 billion set in 2002.

Today’s Must Reads

- Cheese fallout | The price of Scotch, French wine, cheese and other European exports is about to go up in the U.S. after the Trump administration announced new tariffs on billions of dollars of EU products because of the Airbus ruling.

- Alabama spared | Airbus itself was spared the full impact of U.S. import tariffs as Trump took steps to exempt planes built at the company’s Alabama plant from the 10% duty.

- Soy signals | Chinese firms have been snapping up U.S. soybeans this week, but don’t mistake this as a sign of buyer confidence in upcoming trade talks.

- China capital pain | Trump administration pressure on China’s access to U.S. capital markets is likely to intensify, according to several analysts.

- Brexit plan doubters | Boris Johnson presented a new Brexit plan and is optimistic he’s got enough support from Tory hardliners to win the backing of lawmakers. In Brussels, however, officials said Johnson’s proposals are still unacceptable.

Economic Analysis

- Swedish sorrow | The latest survey data suggest Sweden’s production is shrinking fast and manufacturing will probably weigh on growth in the fourth quarter. Sweden has advantages compared with other exporters, but the slowdown is here.

- Dismal Britain | The composite PMI continued to paint a dismal picture in September. Hard data for 3Q may be more upbeat, but the outlook is likely to darken quickly if the U.K. exits the EU early next year without a deal.

Coming Up

- Oct. 4: U.S. trade balance

- Oct. 8: Japanese, South Korean, French trade balance

- Oct. 10: German, U.K. trade balance

- Oct. 10-11: U.S.-China talks in Washington

To contact the editor responsible for this story: Zoe Schneeweiss at zschneeweiss@bloomberg.net, Fergal O'Brien

©2019 Bloomberg L.P.