(Bloomberg Opinion) -- Stock markets jumped in unison Thursday on the news that China and the U.S. have agreed to roll back tariffs on each other’s goods in phases as they work toward a broader trade deal. This makes sense, as various surveys have shown that trade uncertainty is the primary risk facing markets. But if a detente is at hand, investors must confront two critical questions they have ignored so far.

The first is whether equities can keep rising if an agreement only reinforces the notion that the Federal Reserve is done cutting interest rates and may even start talking about boosting them sooner rather than later. In the absence of earnings growth, a strong case can be made that the only reason stocks have managed to rally is because of the the Fed’s dovish pivot earlier this year and three subsequent rate cuts. In fact, rates markets are no longer convinced the central bank will ease monetary policy further any time in the next two years, according to Bloomberg News’s Vivien Lou Chen. The second question is whether the economy can pick up enough to allow companies to meet lofty earnings estimates for next year. Although analysts have slashed their fourth-quarter earnings estimates for members of the S&P 500 Index to an average decline of 0.3% from an increase of 7% in June, estimates for 2020 have barely budged, remaining stubbornly high at 9.7%.

This wouldn’t be so concerning if stocks were cheap, but they are not. The S&P 500 is trading at 17 times the following year’s projected earnings. That ratio has been higher only once since the economy began to recover from the financial crisis, and that was during late 2017, just before the S&P 500 took a nasty fall, declining 10% over the course of a couple of weeks in late January and early February 2018.

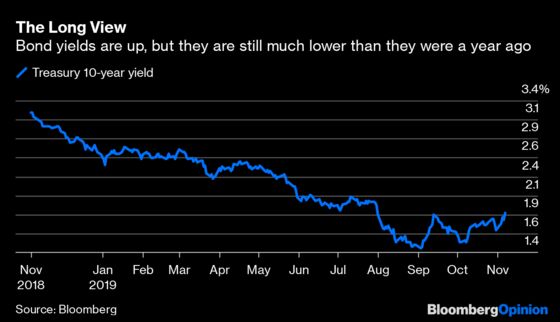

BONDS TAKE A BEATING

The news coming out of the bond market on Thursday in reaction to the trade developments seemed pretty jarring. By some measures, yields on U.S. Treasuries were up the most since the day after Donald Trump’s election as president. But at 1.94%, the yield on 10-year notes is still way down from 3.24% a year ago and is far lower than the 3.05% to 3.15% that economists predicted them to be by now at the start of the year. In other words, yields are still pretty accommodative. In the midst of the sell-off, the Treasury sold $19 billion of 30-year bonds. The takeaway was that there was plenty of demand, showing bond traders aren’t totally convinced a trade war detente will lead to a much stronger economy. That was illustrated by the strong demand from non-bond dealers. That group, unlike bond dealers, who are obligated to bid at the auctions, received 79.3% of the issue, the most since at least 2006. What many seem to be forgetting about tariffs is that they are generally deemed to be inflationary. So reversing the tariffs should lessen any inflationary pressures, which is ultimately good for bonds.

CURRENCIES ARE ACTING ODD

The broad “risk on” environment made for some odd moves in the foreign-exchange market, specifically with the dollar. The U.S. currency is generally viewed as a haven along with the yen and Swiss franc in times of turmoil. But on Thursday, the Bloomberg Dollar Spot Index managed to post its fourth consecutive daily gain while the yen and franc declined. One plausible explanation is that the easing of trade tensions makes it even less likely that the Fed cuts rates. That was certainly seen in the bond market, where Treasury yields rose to a three-month high. Higher yields tend to make a nation’s currency more attractive to international investors. That’s especially true in a world with about $13 trillion of debt yielding less than zero. The flip side is that a stronger dollar can act as a counterweight to corporate earnings. With some 30% of the revenue of S&P 500 companies coming from outside the U.S., S&P Global Ratings figures that the benchmark rises 3.7 times more from a falling dollar than a rising one. In that sense, it’s probably no mystery why the S&P 500 had one of its better months of the year in October, rising 2.04% as the Bloomberg Dollar Spot Index fell 1.89% in its worst month since the start of 2018.

COMMODITIES REACT MILDLY

The commodities market had a muted response to the trade news, with the Bloomberg Commodity Index actually falling for a second day. Of course, much of this is tied to weakness in assets such as gold as demand for havens waned, but other commodities could hardly be described as buoyant. Agricultural commodities were mostly flat to lower, which is odd given that China would most likely step up its purchases of U.S. farm goods under any trade deal. It’s always dangerous to talk about the commodities market in broad terms, even agricultural commodities given how unique each product is and how they react to factors like the weather and supply and demand. But perhaps traders figure the agriculture market in the U.S. would be better off if maintained the status quo. Almost 40% of projected farm profit this year will come from government aid related to the trade war, disaster assistance, federal subsidies and insurance payments, according to a report last week from the American Farm Bureau Federation using figures based on Department of Agriculture forecasts. That’s $33 billion of a projected $88 billion in income, Bloomberg News reported.

BRAZIL’S OIL DEBACLE

The “total disaster” that was Brazil’s largest-ever auction of oil deposits reverberated for a second day on Thursday as the nation’s currency, the real, weakened even as the broader market for emerging-market currencies rallied. The issue is that of the three oil deposits Brazil was selling, it really only received bids for one, and that was from its own state-controlled oil company. Brazil’s Economy Minister Paulo Guedes said Thursday that he’s “terrified” that the world’s biggest oil companies skipped the high-profile auction that was intended to lure billions of dollars in investments, according to Bloomberg News’s Murilo Fagundes. “We spent years talking about the transfer of oil rights, and no one showed up,” Guedes said. “We went through a lot of trouble and, in the end, we sold things to ourselves.” This is no small matter. As the strategists at Brown Brothers Harriman pointed out, Brazil could use the money. It has a current-account deficit that was 2% of its gross domestic product in September, the biggest shortfall since March 2016. Plus, its foreign-exchange reserves are shrinking, and its net international investment position expanded to a deficit of almost 40% of GDP in the second quarter, the most since 2010.

TEA LEAVES

After falling in August to its lowest level since 2016, the University of Michigan’s monthly consumer sentiment has risen for two consecutive months. Making it three in a row looks like a long shot. The university is forecast to say on Friday that its preliminary measure of sentiment was unchanged at a reading of 95.5 for November. It’s possible that the impeachment hearings in Washington have caused consumers to reassess their opinions of the economy and their personal situations. And while the unemployment rate remains near a 50-year low, job growth has slowed. Then again, the stock market has broken out of the tight range that it had been in since June, which could bolster sentiment. Either way, economists will closely scrutinize this report for clues as to how consumers are feeling heading into the all-important holiday season.

DON’T MISS

Fed’s Inflation Promise Leaves Plenty of Wiggle Room: Tim Duy

Silicon Valley Is a Born-Again Believer in Profits: Shira Ovide

The U.S. Economy Could Be Missing Over 5 Million Men: Justin Fox

Pimco Is Getting It All Wrong About Britain: Marcus Ashworth

The Amazing Affordability of Wind and Solar Power: Peter Orszag

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.