Top Turkey Bankers Say They Were Fired on Regulators’ Orders

The bankers paint a picture of a government that relies increasingly on pressure tactics and legal threats.

(Bloomberg) -- Turkish authorities have extended their campaign against perceived political enemies into the $750 billion financial industry.

Eleven former senior executives of non-state banks told Bloomberg News they were dismissed in the past two years on orders from banking regulators, who are overseen by Berat Albayrak, the president’s son-in-law, who has been treasury and finance minister since July 2018.

Fearing further repercussions, all spoke on condition of anonymity -- except one. “It’s time for me to speak up,” said Kerim Rota, 55, who is turning to politics as a member of the opposition now that his three-decade run, capped by his role as deputy chief executive officer of Akbank TAS, is over.

To report this story, Bloomberg reviewed, and followed up on, two years of stock-exchange filings by the 30 biggest non-government banks in Turkey. The disclosures are required for changes at the level of chairman, CEO and deputy CEO.

In a statement Sunday, the Banking Regulation and Supervision Agency, known as the BDDK, called the claims unfounded and vowed to take legal action, saying its role in the hiring of top bankers is in line with best practices. Policy makers led by Albayrak have previously said that their management helped Turkey recover from a targeted financial attack in mid-2018, when the lira weakened as much as 45% against the dollar.

Economic Turmoil

Two senior government officials say the stewards of the economy are looking to eliminate what they call economic “traitors” in both the public and private sector, especially in the wake of the 2018 collapse in the lira. One of the two officials attributed the firings to a desire to find scapegoats. Others have been fired for personal vendettas over their political views, the person said.

The bankers paint a picture of a government that relies increasingly on pressure tactics and legal threats, as well as political loyalists, to enact its economic program. They say the private sector is no longer free to act without interference. The bond and currency markets themselves have been weakened by state intervention, they say.

Crossing a Line

While the financial market has long been a battlefield for President Recep Tayyip Erdogan, who railed for years against what he called an “interest-rate lobby” that drove up the nation’s borrowing costs, the intervention into bank hiring and firing decisions broke new ground. Even during a 2013 crackdown responding to anti-government protests and two years of emergency rule that followed a failed coup in 2016, bankers and bond dealers remained relatively untouched.

That changed with Rota’s dismissal in late 2017 when tensions with western allies were unnerving investors and roiling markets. Since then, one executive was ousted in early 2018; another six, between August and October 2018, the height of the crisis spawned by a collapse in the lira. Three bankers have been forced out in 2019. Those targeted include both men and women.

The most recent involved the downfall of a deputy CEO, according to multiple people who have direct knowledge of the matter. It followed a September meeting with an International Monetary Fund delegation when he told the visitors the banking regulator’s estimate of non-performing loans was too low, according to three people familiar with the matter. A government representative was also there.

The response from the regulator came a few days later, demanding the ouster of the executive. The IMF declined to comment.

Broken by State

Albayrak, 41, was named to his economy post weeks after his father-in-law won an election that gave him sweeping new powers over previously independent institutions like the central bank.

He clamped down almost immediately. Banks were ordered to limit swap transactions, making it virtually impossible to bet against the currency. Traders believed there was also intervention in government bond auctions; when Turkey sold debt at below-market costs, Albayrak commented, “I guess some financial institutions in the market are a little bit disturbed by our new Treasury strategy.”

Price controls, raids on shops over spiraling food prices, and orders to lenders to keep credit flowing followed. Turkey started a probe into a JPMorgan Chase & Co. unit for a report highlighting undercover intervention in the lira market.

The banking regulator also opened a probe into Bloomberg News’ reporting on the lira crash and consequent economic turmoil in the summer of 2018. It has resulted in a court case in which two Bloomberg reporters have been indicted and face as much as five years in prison.

Debt Strain

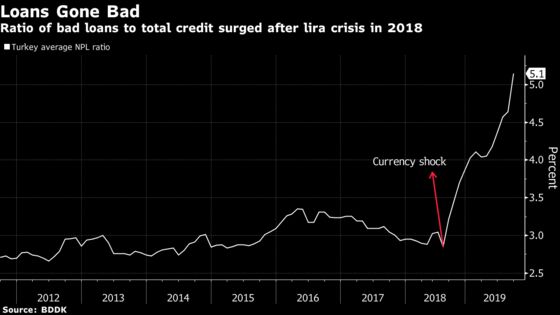

As the pile of foreign-currency debt surged with the lira’s decline, getting lenders to cooperate was critical to keeping the economy functioning, according to the former executives. While the currency has stabilized this year, weakening about 8% against the dollar after 2018’s 28% plunge, banks are struggling to reduce their non-performing loans.

A senior loan officer says he was forced out of his job after the currency crash. He was never given a reason. He said he was invited to a patisserie by the CEO, who then told him that the BDDK had singled him out, demanding his access to the bank be denied and his email account shut down immediately.

The banker told Bloomberg that once he and others dealing in lending decisions were fired the way was clear for pro-government companies to access the credit they needed. He says the intimidation worked: debt-restructuring demands he described as “ridiculous” were quickly approved as others saw his firing as a message.

Another executive says colleagues were surprised when he quit because he seemed to be in the prime of his career. Speaking on condition of anonymity, the banker told Bloomberg he resigned after the BDDK told the bank’s owner to fire him.

One of the ex-bankers left Turkey, saying he was unable to find work after losing his job. Another said the aftermath of the dismissal has been an “extremely difficult process for me both emotionally and financially” because the job supported the banker’s extended family.

Keeping the Flow

Other bankers said that lower-level managers were also ousted, but there’s no way of knowing how many because the lenders aren’t obliged to report such removals.

Another banker said he was fired due to his activities in financial markets. The government chased him out even after his removal and had him sacked from a private-sector company as well, he said.

Rota says he suffered the same fate. Speaking to Bloomberg in October, two months before he emerged Dec. 13 as a founding member of former Prime Minister Ahmet Davutoglu’s Future Party, Rota said he suspected the BDDK intervened to prevent a foreign-owned bank from hiring him.

The end of his career started with what was supposed to be a promotion. In October 2017, he was offered the CEO post at Odea Bank AS, a unit of Lebanon’s Bank Audi SAL. He resigned from Akbank, one of the largest lenders by market capitalization, expecting to start his new job in December.

All he needed was the expected rubber stamp from the BDDK, which must confirm the qualifications of high-level banking hires. That’s when the trouble started.

Rota’s Application

BDDK told Odeabank not to file his application, according to the bank’s account in a lawsuit brought by Rota for allegedly breaching its promise of employment. At a follow-up meeting, BDDK repeated the warning to Odeabank executives against Rota even seeking their approval, the lender’s court filing said. While the BDDK statement didn’t name Rota, it said no bank has ever applied to get the necessary regulatory approval to hire him. Odeabank declined to comment.

No reason was ever given, but Rota said he was told by a senior government official that it was Albayrak’s order. That struck him as odd because the future finance minister was still the energy minister.

Rota attributes the banishment to his pessimism about the economy and the Akbank trading desk he oversaw, which was known for its aggressiveness. “I never knew for sure, but I think it was about my market-making role in the bond market,” Rota said.

“In a way I was the lucky one,” Rota says now. “I’ve already raised my kids, earned my life, and I don’t need to worry about money. I am speaking today because I see them doing it to other people. Most of these people are young, so once their careers are wrecked, their life might be destroyed as well.”

©2019 Bloomberg L.P.

With assistance from Bloomberg