Tide Is Turning for Indian Bonds on RBI’s Liquidity Bonanza

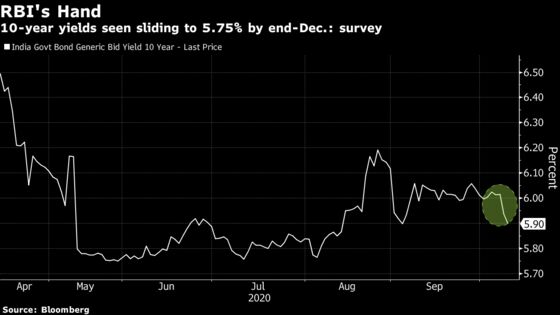

Yield on India’s benchmark 10-year bond fell about 13 basis points over the past month to 5.9%, making it Asia’s best performer

(Bloomberg) -- India’s sovereign bonds are turning a corner as a supply overhang dissipates following a raft of liquidity measures from the central bank. Early signs of economic revival are also spurring hopes of an improvement in government finances.

The yield on India’s benchmark 10-year bond fell about 14 basis points over the past month to 5.9%, making it Asia’s best performer, with the bulk of its decline coming in after the Reserve Bank of India announced steps including doubling the size of its bond purchases in a policy address last week.

The expectations are for the 10-year yield to drop further to 5.75%, a level last seen in July, according to a median estimate of 15 traders surveyed by Bloomberg. That’s compared to forecasts of around 6% just two weeks ago amid concern that the administration may further hike its 12 trillion rupees ($163.8 billion) bond sale target for the year.

“The RBI in one shot has cleared all the uncertainty about the heavy borrowing program and we could see bonds gaining from here on,” said Anoop Verma, senior vice president at DCB Bank Ltd. in Mumbai.

Bonds were primed for gains even before the RBI announcement as data showed a manufacturing index rose to the highest in more than eight years, while goods and services revenues improved, spurring optimism the government may not increase its borrowing target further after a 54% hike in May. The government said in late September it will leave its October to March issuance plan unchanged at 4.34 trillion rupees.

However, the RBI still faced ire from bond traders for not doing enough to shoulder the government’s unprecedented debt issuance.

The RBI has resisted calls for direct debt monetization like that done in Indonesia and the Philippines but it sporadically purchased bonds via open market operations and conducted Federal Reserve-style Operation Twist, by buying and selling notes simultaneously. Still underwriters have had to rescue four of the recent seven bond sales and the 10-year yield rose by the most in over two years in the quarter ended September.

The RBI responded by announcing additional liquidity steps last week including raising the size of open-market purchases to 200 billion rupees, stepping in to buy state debt, and supporting corporate bonds via one trillion rupees of long-term repo operations.

RBI’s measures will “soothe market concerns on demand-supply dynamics and should lead to a gradual reduction in term premiums,” said Dhawal Dalal, Mumbai-based chief investment officer for fixed income at Edelweiss Asset Management Ltd. Rising economic activities should also help in higher tax collections, he said.

Inflation Threat

Bonds also received a boost after the RBI Governor Shaktikanta Das said the monetary authority sees the recent surge in inflation as transient and that the central bank will keep its stance accommodative at least through the current financial year and into the next year to revive growth.

Still data on Monday showed consumer prices accelerated more than estimated in September, capping gains in long-end bonds.

“The unresolved question is whether there is potential for more than tactical gains at the long end,” said Suyash Choudhary, head of fixed income at IDFC Asset Management in Mumbai. “The RBI’s approach is to keep yields stable in the face of the extraordinary bond supply that needs absorption, rather than to actively engineer a large rally.”

©2020 Bloomberg L.P.