There Were Warnings on the Banks. Nobody Listened: Taking Stock

There Were Warnings on the Banks. Nobody Listened: Taking Stock

(Bloomberg) -- It may be tiresome to read day in and day out, but everything seemed to stall the second the S&P 500 came within a couple of points from touching the ~2,600 resistance line.

The brakes aren’t strictly being pumped on the post-Christmas rally -- it’s also the volumes: Aside from that Christmas Eve session to remember, the last two days have seen the lowest trading action on the consolidated tape since late November.

That’s probably a result of general market fatigue from what has been an unusually eventful couple of months, especially through the holidays. It’s also a function of a ton of Fed speak having been priced into the market over the past few weeks, a prevailing atmosphere of uncertainty in regards to the trade war and trade impact in general, a "What Me Worry?" reaction on Wall Street to the record-setting government shutdown, and this in-between state when macro news is beginning to cede to micro as earnings season gets underway.

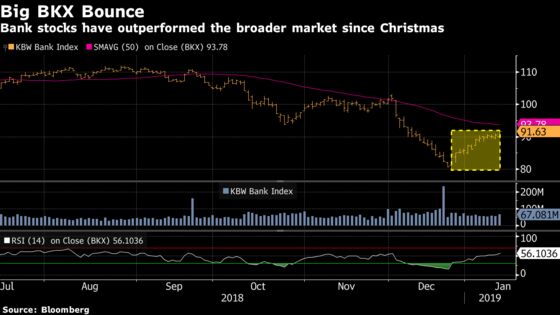

Banks had a good start with Citi -- the BKX rose 1.2% Monday while the broader financials group was the sole S&P 500 sector in the green Monday -- but that might not last long as JPMorgan shares are already fading ~2% in the pre-market after a slew of headline misses, from adjusted EPS to FICC sales/trading and investment banking revenue.

It’s not like this wasn’t telegraphed by the Street.

Wolfe Research talked about the low quality beat and negative read-across in both FICC and ECM for a few peers, including JPMorgan. Macquarie went a step further, as my colleague Felice Maranz pointed out earlier, warning about the spillover throughout the entire space:

"Citi should not have been the first bank to report earnings this quarter because the better earnings were largely driven by Citi-specific factors such as higher card yields, lower tax rate, lower preferred costs and lower credit costs in its legacy portfolio. These factors should drive up consensus for Citi; however, disappointing trading and deteriorating deposit mix are negative read throughs for the industry."

Elsewhere, tech was weighed down by the semiconductors, with the SOX notching its worst loss since the day Apple cut its sales outlook. You can blame a couple of sell-side shops for putting pressure on the space yesterday, and now Deutsche Bank is piling on the semicap equipment names with a cut to its wafer fab equipment spend view (now -16% y/y vs prior -6% and memory WFE -30% vs prior down 10%-20%).

Retail didn’t fare much better, getting minimal budge from Lululemon’s forecast boost; the XRT has now fallen nearly 2% in the past three days versus a relatively flat tape as the ICR conference rolls on.

Utilities, and a whole lot of shareholders, got wrecked on the back of the PG&E bankruptcy filing, with shares having tanked 66% in just over a week. Hedge funds owned close to 20% of the outstanding shares as of the most recent filing in Sept., according to Bloomberg data, and you can see a list of the top holders from that date in the graphic below.

Seth Klarman’s Baupost Group, the top name on the list, also held $1 billion of legal claims that gave the fund the right to recover losses incurred from the wildfires, according to our scoop yesterday. The WSJ has a fresh take on the impact to Wall Street, noting that some hedgies have exited their losing PG&E trades in recent weeks while others (Avenue Capital, Elliott Management, King Street Capital) bought corporate bonds on Monday.

Sectors in Focus Today

- Banks after JPMorgan’s miss; Wells Fargo reports later this morning

- Airlines may be weak after Delta’s EPS view trailed estimates

- Managed care after UnitedHealth reported a beat

- Autos with a couple of sell-side conferences kicking off today; see our big preview of the plethora of industry events coinciding and the tick-by-tick agenda at the bottom of this column for presentation times for some of the bigger companies in attendance

- Semicap equipment stocks, like Applied Materials and Lam Research, after Deutsche Bank slashed wafer fab equipment spend estimates, as mentioned above

- Lithium names with Nomura Instinet downgrading Albemarle and Livent Corp. on expectation that price data points will "surprise negatively in coming months"

- Pot stocks given the Tilray lockup (they announced a marketing pact with Authentic Brands in conjunction) and a continued rip in Canopy Growth (up 58% year-to-date)

Notes From the Sell Side

Morgan Stanley has a wide-ranging 2019 outlook note on the Attractive-rated software sector. Top picks are Microsoft (new price target matched Street high $140), Palo Alto Networks, and Salesforce. The analysts upgrade Akamai, New Relic, DocuSign, Tenable, Five9 to overweight, downgrade VMware, Oracle, Autodesk, Nuance to equal-weight and cut Atlassian, Zscaler, and Yext to underweight.

Baird has two calls worth mentioning this morning: 1) Reiterating outperform on Tesla and expecting Model 3 demand to remain robust after hosting tours of the company’s West Coast factories; 2) Cutting estimates on Carvana as data points suggest the firm isn’t immune to the holiday spend slowdown; note this comes after shares fell 3.5% yesterday on a brutal initiation from Morgan Stanley.

Deutsche Bank is out with a new catalyst call, recommending clients sell shares of U.S. Steel ahead of 4Q results on the expectation that 2019 Ebitda guidance will disappoint: "Despite the 10% revision the past month, we believe, the current consensus of ~$1.6bn is still high (DBe $1.2bn), with spot US HRC/CRC pricing ~$110/st below the 2018 average (2018E EBITDA guide $1.8bn)."

Tick-by-Tick Guide to Today’s Actionable Events

- Today -- FDA briefing documents for LXRX/Sanofi’s sotagliflozin

- Today -- IPO lockup expiry: TLRY, ALLK, MYFW, CNST, ESTA

- 8:00am -- WFC, FRC earnings

- 8:30am -- Empire Manufacturing, PPI

- 8:30am -- JPM, SNV earnings call

- 8:30am -- URBN at ICR conference

- 8:30am -- Top Live for Ford, Volkswagen CEOs updating on alliance talks

- 8:30am -- GPRE CEO Todd Becker on Bloomberg TV

- 8:45am -- UNH earnings call

- 9:00am -- M at NRF retail conference

- 9:30am -- BJ, SHAK at ICR conference

- 10:00am -- ECB’s Draghi presents annual report

- 10:00am -- WFC, FRC, DAL earnings call

- 10:00am -- CMG, AEO at ICR conference

- 10:30am -- PLNT at ICR conference

- 10:30am -- WTW at NRF retail conference

- 10:40am -- WWE at Needham growth conference

- 11:00am -- Top Live with GM CEO and CFO at Detroit Auto Show

- 11:00am -- GM at Wolfe Research global auto conference

- 11:05am -- TM keynote at Deutsche Bank auto conference

- 11:30am -- Fed’s Kashkari on regional economy at Minnesota event

- 11:30am -- FTCH, DENN at ICR conference

- 11:50am -- LEA at Wolfe Research global auto conference

- 11:50am -- VC at Deutsche Bank auto conference

- 12:30pm -- Green Growth Brands at ICR conference

- 12:35pm -- GT at Deutsche Bank auto conference

- 1:00pm -- Fed’s Kaplan and Fed’s George speak at separate events

- 1:00pm -- DPZ, OLLI at ICR conference

- 1:20pm -- TEN, CTB at Deutsche Bank auto conference

- 1:30pm -- TLRY at ICR conference

- 2:00pm -- Top Live for U.K. Parliament voting on Brexit deal

- 2:00pm -- CROX at ICR conference

- 2:10pm -- DAN, ABG at Wolfe Research global auto conference

- 2:50pm -- NIO, VNE at Deutsche Bank auto conference

- 2:55pm -- AXL, LAD at Wolfe Research global auto conference

- 3:30pm -- MDB at Needham growth conference

- 3:40pm -- MGA, VC at Wolfe Research global auto conference

- 4:00pm -- CRON, TUP at ICR conference

- 4:00pm -- WFC CFO John Shrewsberry on Bloomberg TV

- 4:15pm -- UAL earnings

- 4:25pm -- F at Wolfe Research global auto conference

- 4:30pm -- API oil inventories

- 8:30pm -- China New Home Prices

To contact the reporter on this story: Arie Shapira in New York at ashapira3@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.