The Transitory Inflation Question Is Coming for the ECB

The Transitory Inflation Question Is Coming for the ECB

(Bloomberg) --

The European Central Bank’s biggest decision this week is to decide if it can still call the current inflation spike “transitory.”

The answer will have a huge bearing on the euro-area economy, which is already dealing with resurgent coronavirus infections, new restrictions and lockdowns, and uncertainty about the omicron variant.

A wrong call would have grave consequences. Keeping monetary policy expansionary for too long could allow inflation to get out of control, forcing more abrupt tightening later that chokes off growth. But scrapping the term could signal a faster stimulus exit, sparking a potential sell off in peripheral bonds along with tighter financial conditions that risk bruising the economy right now.

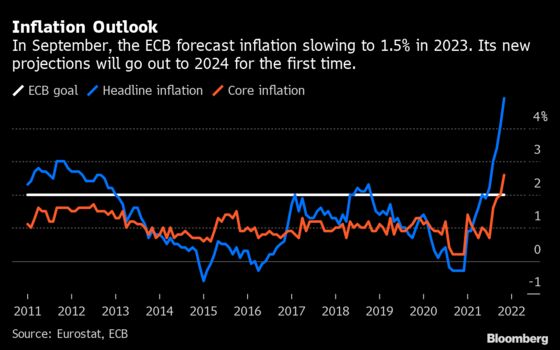

In its Thursday decision, the Governing Council will be able to lean on new forecasts through 2024. President Christine Lagarde is convinced that consumer-price growth — currently at a record 4.9% — will eventually return below the ECB’s 2% goal. Her deputy Luis de Guindos is concerned that inflation “will not go down as quickly and as much” as predicted, and Executive Board member Isabel Schnabel is seeing upside risks.

Federal Reserve Chair Jerome Powell has already dumped the transitory description, and many others have disputed the term’s validity. The ECB may have reasons to keep it — beyond fear that a change in tone could lead to a damaging market reaction — such as labor market slack and relatively low underlying inflation.

Here’s a look at what’s driving inflation in the 19-country region and how those factors will evolve.

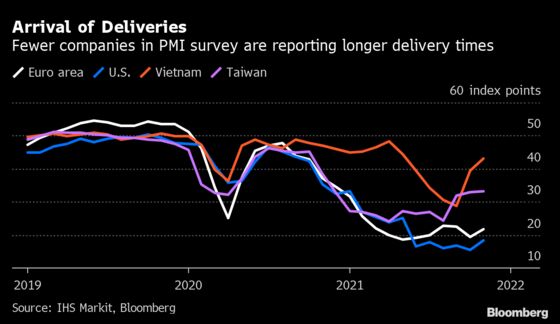

Supply Chains

Global shortages of parts and raw materials are lasting longer than expected, though businesses expect them to ease “gradually” through 2022. Economists at JPMorgan Chase & Co. agree, citing evidence such as declining shipping prices that show problems are “abating across a broad range of indicators.”

According to recent surveys, fewer companies are battling with longer delivery times, although the situation remains tense in the euro area and the U.S. The Bank for International Settlements has said that some price trends “could even go into reverse” when companies stop precautionary hoarding.

The pandemic remains a risk. For example, Asian countries tend to have a low tolerance for higher infection rates, meaning a fresh spike in cases could well lead to new production disruptions that would ripple through the global economy.

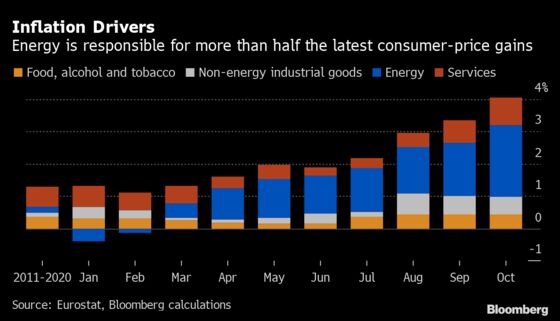

Energy Effects

The commodity rally has been a key driver of inflation, with energy responsible for more than half of the latest rate. Oil prices in Europe are up 48% this year while the cost of natural gas increased five-fold.

Bank of America Corp. says prices have even further to go, with average crude oil seen rising to $85 a barrel next year from $70 this year. For natural gas, the energy transition to net zero could mean prices stay high, and volatile.

Most energy price forecasts only go out about a year or two in advance. Clouding the picture for Europe is a cocktail of global factors — tension with Russian President Vladimir Putin over Ukraine, oil stocks being released in the U.S. or colder weather — that could impact prices.

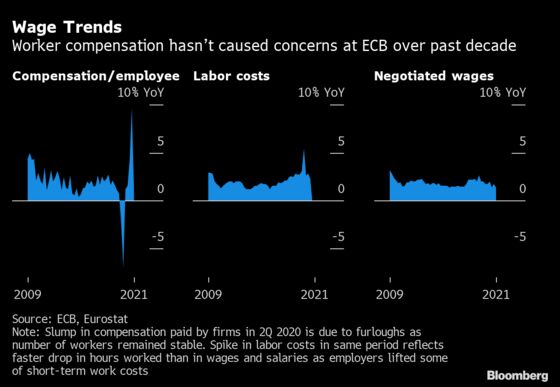

Wage Growth

Europe’s labor market is recovering, and economists including Anna Titareva at UBS AG see wage growth returning to around 2.5% by the end of 2023. She and her colleagues estimate that each 1% increase boosts the core rate by some 0.3 percentage point.

In Germany, the minimum wage is set to rise by 25% — a one-time adjustment UBS argues could create broader pay pressures in the economy. Compensation in France will likely be held back by significant labor-market slack as well competitiveness concerns. Wage growth in Spain may settle around 2% next year and 3% in 2023.

Bloomberg Economics says there’s no evidence of overheating. And while higher inflation and a tighter labor market could lead to annual pay growth of as much as 3%, that’s “not of a scale that would concern the ECB,” according to Philippe Gudin of Barclays.

Consumer Demand

The inflation spike has been partly attributed to a shift in consumer spending from services — closed for long periods during lockdowns — to goods. The demand overwhelmed factories that were grappling with restrictions of their own.

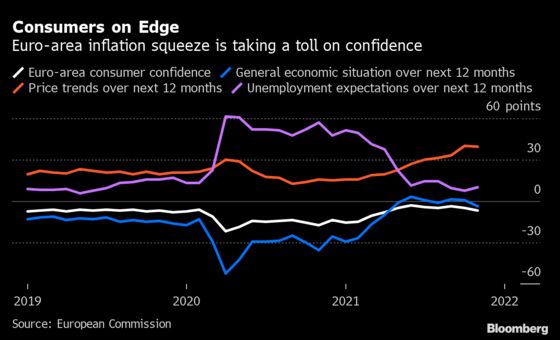

Households still have hundreds of billions of euros in excess savings that could be splurged, though an ECB analysis has concluded that there’s “limited” likelihood of all that money quickly flowing back into the economy. In addition, resurgent infections and the inflation squeeze are denting the consumer mood.

Statistical Quirks

The biggest relief for euro-area inflation will come from Germany, when the impact of lower value-added taxes in the second half of 2020 and a surge in carbon taxes fall out of the equation. The Bundesbank estimates that the former alone has boosted consumer prices in the country by more than 1 percentage point, while Berenberg predicts that the expiration of both effects could reduce euro-area inflation by 0.4 percentage point in January.

Yet changes to the basket of goods and services used to calculate inflation — the previous year’s spending patterns matter — could delay a slowdown in prices in the second half, according to Bloomberg economist Maeva Cousin.

What Bloomberg Economics Says…

“If HICP weights return some way toward their 2020 pattern, the statistical effect would reverse relative to this year, pushing up headline inflation over the summer of 2022, and delaying the decline in price growth from mid-2022.”

— For full note, click here

Euro-area inflation will reach a trough of around 1.5% next November, said Berenberg’s Holger Schmieding. “Thereafter, an uptick in wage costs, the costs of the green transition, a restructuring of global supply chains and increased government interventions into the economy could underpin a slow but sustained uptrend in inflation for years to come.”

Read More:

©2021 Bloomberg L.P.