The Times America Went Big and Flooded Economy With Federal Cash

The Times America Went Big and Flooded Economy With Federal Cash

(Bloomberg) -- Fear and panic spread through financial markets Monday in what’s set for the biggest crash since 2008 -- and so did pleas for the U.S. government to deploy all its spending power against the economic threat posed by the coronavirus.

It wouldn’t be the first time America has resorted to large-scale fiscal stimulus in a peacetime emergency.

The New Deal of the 1930s, a response to the Great Depression, is probably the most far-reaching example. But on other occasions too, policy makers have wielded the power of the purse to protect or provide jobs, encourage corporate investment -- or substitute for it -- and strengthen safety nets for the public and businesses.

President Donald Trump and his economic team will weigh measures later Monday to contain the fallout from coronavirus and a sudden crash in oil prices, with funding for a temporary expansion of paid sick leave and aid for battered U.S. energy producers among possible steps.

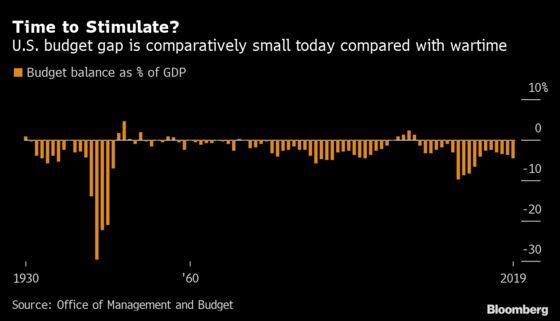

While the administration was talking Friday about “micro-measures,” investors and economists are urging them to go big -- especially as the Federal Reserve is constrained by already-low interest rates. It’s still not certain yet if the virus will cause a recession, but it’s so far hobbled supply chains and caused travel spending to dwindle.

Here are some episodes from U.S. history where fiscal policy has stepped in to the rescue.

The New Deal

The biggest restructuring of the economy in the past century was carried out on a wave of government money. The Great Depression pushed unemployment to at least 25% and millions of Americans lost their life savings after a run on the banks (which didn’t insure deposits at the time).

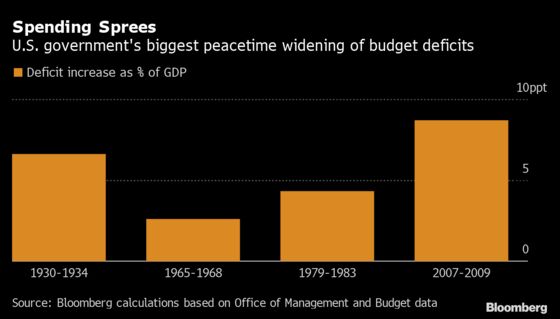

President Franklin D. Roosevelt’s New Deal funneled cash to infrastructure and other public works, and social programs. The federal budget went from a surplus of 0.8% of gross domestic product in 1930 to a deficit of 5.8% in 1934, according to historical data from the White House.

The fiscal intervention was even more decisive than those numbers suggest, because safety-net programs like unemployment insurance and social security barely existed. Nowadays, those so-called “automatic stabilizers” kick in during a crisis and allow deficits to expand without the government making any specific decisions to spend.

Big infusions of government cash often come together with new regulations, and that happened during the New Deal too. Industrial and labor rules granted more power to unions, and allowed governments some control over important prices. Banking reforms helped stabilize the financial system and gave additional powers to the Fed, including centralizing power with officials in Washington.

The Great Society

Unlike other big infusions of government spending, President Lyndon B. Johnson’s Great Society program wasn’t a response to a financial crash. When it got under way in the mid-1960s, the U.S. economy was growing and unemployment was near all-time lows.

Johnson’s policies were focused on eliminating poverty and lowering inequality, by providing job training and employment opportunities in poor regions and ramping up spending on education. Its legacies include programs relied on by millions of Americans today: Medicare and Medicaid, the Elementary and Secondary Education Act (which provided greater access for disadvantaged students), the Department of Housing and Urban Development, and food stamps.

Results included a drop in poverty rates by more than one-third. Bigger fiscal deficits, combined with a U.S. trade gap, also put the dollar’s link to gold under pressure and helped trigger the shift to fiat money a few years later. Fiscally conservative Republicans still criticize some of the programs.

The Reagan Deficits

President Ronald Reagan won election in 1980 on a program that said government was the problem, not the solution, but in his early years in office Reagan oversaw a sharp increase in federal deficits to pull the economy out of recession. His team embraced an idea known as “supply-side economics” which has adherents in the Trump administration.

Its main claim is that even if cutting taxes leads to budget shortfalls in the near term, the measures will ultimately pay for themselves because they’ll juice the economy and eventually allow the government to collect more taxes. Few economists agree, and the 1980s record shows that while deficits shrank from their Reagan-era peak of 5.9% of GDP, they didn’t return to below 3% during his term.

Growth did accelerate though, and the Reagan deficits weren’t all about tax cuts. Government spending rose too, partly driven by a military buildup in the last phase of the Cold War that took defense spending back above 7% of GDP after a decade of declines.

The 2008 Crash

The American Recovery and Reinvestment Act of 2009, the first year of Barack Obama’s presidency, was the largest influx of federal cash to the U.S. economy since the 1930s, costing a total of $840 billion -- or $2,740 per citizen. Adjusted for prices, that’s probably about half the size of the New Deal measures.

It passed Congress with the support of only a handful of Republicans. Early in 2008, before the collapse of Lehman Brothers sent world markets into a full-scale collapse, the Economic Stimulus Act -- a smaller package worth about $150 billion -- was passed with bipartisan support and approved by President George W. Bush.

Both measures focused on job creation and social programs, with increases to unemployment benefits, job training, food stamps and welfare payments, and funding for bridges and roads. Tax credits formed one of the largest components of the Obama bill, aimed at encouraging businesses and consumers to keep spending and investing.

Despite the size of the stimulus, economists including Nobel laureate Paul Krugman argued that it wasn’t big enough and criticized the prioritizing of tax cuts over direct spending. Obama aides including Larry Summers have defended the effort on the grounds Congress would have balked at anything bigger.

--With assistance from Scott Lanman.

To contact the reporter on this story: Katia Dmitrieva in Washington at edmitrieva1@bloomberg.net

To contact the editors responsible for this story: Scott Lanman at slanman@bloomberg.net, Ben Holland

©2020 Bloomberg L.P.