The Ringgit Is at Risk From Falling Oil and Slowing Growth

The Ringgit Is at Risk From Falling Oil and Slowing Growth

(Bloomberg) -- Malaysia’s ringgit has navigated the virus outbreak and a slump in crude prices with a measure of resilience. But its fortunes may soon reverse.

A widening fiscal deficit and rising political risks are set to test the currency after it outperformed peers including the Indonesian rupiah and Thai baht in the first quarter. Falling global demand and a possible contraction in Malaysia’s economy will add to the headwinds.

A weaker ringgit could undermine confidence and pose a test for Prime Minister Muhyiddin Yassin, who is seeking to keep the economy afloat while consolidating power after the controversial exit of his predecessor Mahathir Mohamad. A subdued currency could also limit room for the central bank to ease again to shore up slowing growth.

The currency’s main source of pressure will emanate from a prolonged period of depressed oil prices, which may erode government revenues. This in turn could worsen the budget deficit which is forecast to reach 4% of gross domestic product this year, the widest since 2012.

The central bank expects crude to trade at $25 to $35 a barrel in 2020. Brent crude has more than halved to around $30 since the start of the year.

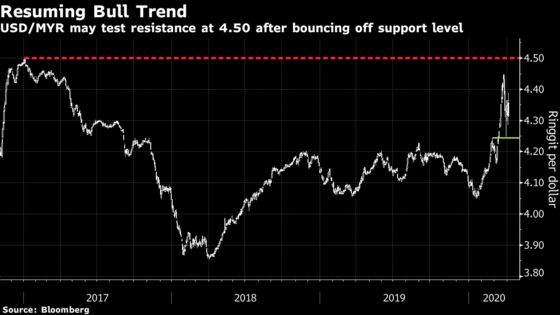

The ringgit slid to 4.4490 per dollar in March, near the 4.5002 level reached in early 2017, which was the lowest in almost two decades.

The dollar-ringgit pair’s bullish momentum remains intact as support around 4.25 held after being tested on March 27. As a result, the pair may test initial resistance at 4.4490, its March 23 high, in the near term. If that level is breached, it may approach the 2017 peak of 4.5002.

Trade Slump

A weakening domestic outlook could also undermine the currency. The forecast for the economy in 2020 is between a contraction of 2% and expansion of 0.5% due to the virus outbreak and low commodity prices, Malaysia’s central bank said last week.

Foreign-exchange reserves data for end-March due this week may provide an idea of Bank Negara Malaysia’s capacity to defend against further ringgit weakness. Holdings dropped to $103 billion as of March 13, the lowest since September.

Politics could be another challenge. PM Muhyiddin may face a confidence vote when parliament resumes in May, with shifting alliances among lawmakers a risk to the new administration.

That’s not to say everyone is pessimistic. The ringgit could strengthen to 4.20 per dollar by year-end, according to the median forecast of seven economists surveyed by Bloomberg from March 20. A key catalyst for the turnaround could be a recovery in oil prices, with risks tilted to the upside once global demand recovers.

Below are the key Asian economic data and events due this week:

- Monday, April 6: India Markit Composite and Services PMI

- Tuesday, April 7: South Korea current account, Philippines inflation, Thailand inflation, Australia trade balance, Reserve Bank of Australia decision, Malaysia foreign reserves

- Wednesday, April 8: Philippine trade, Taiwan trade and inflation, Japan core machine orders and current account

- Thursday, April 9: Bank of Korea decision, India industrial production

- Friday, April 10: China inflation, Japan producer price index

©2020 Bloomberg L.P.