The Rich World’s Canaries Are Starting to Look Sickly

(Bloomberg Opinion) -- It’s always worth keeping an eye on events in the South Seas to see where the world economy is headed.

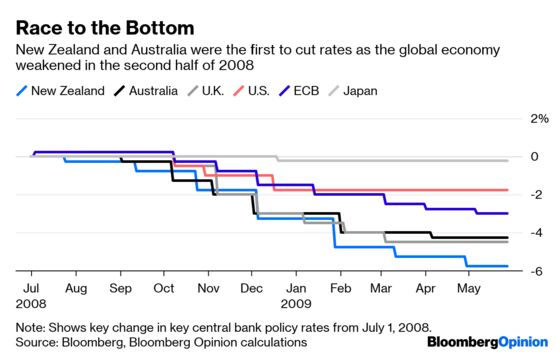

Thanks to their small, trade-dependent economies and open capital markets, ripples from Australia and New Zealand are often some of the earliest signs of trouble emerging in major northern hemisphere countries. In late 2008, the savage rate cuts by the country’s central banks in response to the developing global financial crisis were an early indicator of the rich world’s plummet toward a zero interest-rate policy. Now’s another time to watch what’s happening down under.

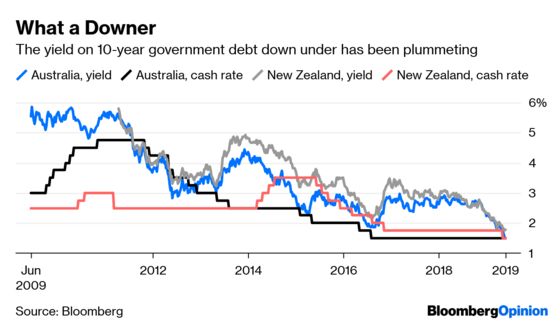

New Zealand’s 10-year government bond rate dropped to a record low of 1.719% Wednesday morning, following heavy bond buying in the northern hemisphere overnight which further inverted a key piece of the U.S. yield curve. Just a few minutes later Australia’s 10-year yield slipped below the Reserve Bank of Australia’s cash rate target for the first time since 2015, a strong indicator that investors are counting on the rate cuts that RBA Governor Philip Lowe all but promised in a speech last week.

In some ways this shouldn’t surprise. New Zealand’s sovereign yields have been on a fairly consistent downward trend ever since those interest-rate cuts in late 2008. Australia’s have been slumping for six months, barely interrupted by a victory for the right-of-center Coalition in elections this month. Australian three-month overnight interest swaps – in effect, the market’s bet on the medium-term cash rate target – are sitting at 1.1695%, suggesting good odds that benchmark rates will be cut by 0.5 percentage point over the next 10 weeks.

At the same time, the speed of the latest leg down should be cause for concern.

“What’s interesting about last night was that there was no particular catalyst” for the rally in bond markets, according to Su-Lin Ong, head of fixed income strategy at Royal Bank of Canada in Sydney. “That raises the question of whether markets are not yet positioned for this reassessment.”

That certainly seems to be the case when you look at equity indexes. Those in Australia and New Zealand are just off record long-term highs, with robust valuations indicating investors are still betting on growth despite the darkening macroeconomic picture from the looming trade war and faltering Chinese economy. Should investors get cold feet and switch to bonds in greater numbers, expect to see those yields heading still lower.

China is a particular concern. Australia is the G-20 economy most exposed to Chinese exports; were New Zealand in that grouping, it would come third after South Korea, where government bond yields are also tracking toward their lowest level in almost three years.

As my colleague Daniel Moss has written, the image of Australia as a recession-proof economy badly needs to be marked to market, especially now that per-capita growth has been falling for two consecutive quarters. So far, the country has been spared the worst effects of the slowdown in China. Despite Chinese purchasing managers’ indexes that are struggling to stay in positive territory, short supplies of iron ore mean that prices for this key export have been strong, cushioning the economy thanks to its robust terms of trade.

Don’t count on that holding out indefinitely. Only demand-driven prices can be counted on for the long term. In both China and the world, that’s looking increasingly shaky. Australia and New Zealand may seem like small canaries in the context of an $80 trillion global economy. When they stop cheeping, though, it’s time to watch out.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.