The Pros and Cons of a PBOC Rate Cut as China's Economy Slows

The yuan strengthened against the dollar slightly last month, the first monthly appreciation since March.

(Bloomberg) -- A decision on cutting interest rates in China weighs the need to bolster the slowing economy with the objectives of curtailing the debt buildup and preventing a slump in the currency.

After still-more disappointing economic data and fog around the trade war with the U.S., investors are upping their bets that more stimulus is on the way. The People’s Bank of China could reduce the one-year lending rate, sending borrowing costs lower across the economy, or focus on driving down inter-bank lending rates through reverse repurchase agreements.

Among economists surveyed by Bloomberg, the consensus forecast sees the benchmark one-year rate remaining on hold for at least the next year. But a debate is raging.

Here are considerations on both sides of the rate-cut debate.

The Case for A Cut

The argument that China needs more aggressive stimulus measures is gaining pace, as many economic indicators hover at multi-year lows in spite of earlier easing.

Ming Ming from Citic Securities Co. and Lu Zhengwei from Industrial Bank Co. say a cut in the benchmark rate or the open market operation rates is needed to encourage credit and lower funding costs. Goldman Sachs Group Inc. have said they expect interbank rates to be manged lower to help growth recover.

External pressure preventing much looser policy is declining, particularly amid signs that the Federal Reserve is turning more dovish. An easing of downward pressure on the yuan, which has declined about 6 percent this year, would mean much greater room for policy makers to cut the cost of borrowing without fear of accelerated declines or even capital flight.

The yuan strengthened against the dollar slightly last month, the first monthly appreciation since March.

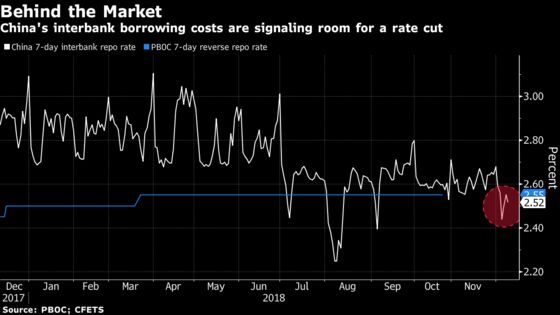

The PBOC also seems to be acquiescing in lower borrowing costs. Since December, the 7-day repo rate has stayed around, and sometimes below, the central bank’s 7-day reverse repurchase rate. That means the interbank rate is close to its bottom -- a further decline in the cost would require a rate reduction.

What Our Economists Say... |

| Anecdotal evidence suggests that private companies aren’t feeling much policy support yet. Clearly, there’s a big risk that tight liquidity and poor sentiment deter private investment -- dragging down growth and worsening the mix. -- Chang Shu, chief Asia economist. Read the full note here. |

The Case Against a Cut

There’s a but. Room for rate cuts is still limited, as top leaders still see a long-running financial cleanup as one of their policy priorities -- and lower borrowing costs fly in the face of that.

Morgan Stanley economists including Robin Xing say China is in a different kind of easing cycle, focusing more on private sector and fiscal stimulus, and economists from China International Capital Corp say rate cuts aren’t the most appropriate approach to guide the effective funding cost lower.

"Cutting benchmark rates may not shore up the economy and could still cause other problems like further inflation of the property bubble, increasing capital flight and worsening income distribution," Lu Ting, chief China economist at Nomura International Ltd., wrote in a recent report.

And while cutting the 1-year rate may be powerful, it would set back China’s transition to a system where it’s short-term market rates that count.

--With assistance from Tian Chen.

To contact Bloomberg News staff for this story: Yinan Zhao in Beijing at yzhao300@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, James Mayger

©2018 Bloomberg L.P.

With assistance from Bloomberg