The Oracle’s Mea Culpa Rebuffs Powell Blues: Taking Stock

The Oracle’s Mea Culpa Rebuffs Powell Blues: Taking Stock

(Bloomberg) -- The obvious macro overhang this morning will be payrolls data at 8:30am, and we do this every month. But that’s part of the fun right?

Most of the mega-caps have reported results, so much of the action today should be driven by this key data input -- from the health of hiring (watch out for census hiring impacts) to inflationary pressures in the hourly earnings data. We’ll see if there can be an unwind of the defensive stance the SPX has taken over the past five sessions. Health care, financials, real estate and consumer staples are far and away the leaders (but since the FOMC meeting, its just real estate and health care in the green).

If the macro isn’t your style, there are some smaller pockets of activity this morning, which themselves seem to be responsible for the majority of the upswing in S&P futures (not to mention there are likely some dip buyers out there search for post FOMC scraps). Warren Buffett’s admission that he is now a buyer of Amazon stock (shares are up 2.5% in the pre-market) is almost entirely responsible for the boost in the QQQs (AMZN accounts for ~10% of the holdings for what it’s worth). Those early buyers of Amazon stock may have a nice smirk on their face about how "late" Buffett is to the party, but the Oracle of Omaha himself said he was "an idiot" for not investing. Let’s all remember he was "late" to Apple and you can see how that turned out -- his investment is likely up by 100% over the span of 3 or so years (he disclosed the stake in 2016).

In addition to watching other members of the QQQs today, like Apple, Facebook and Alphabet, whose shares are also higher (FB is 5% of the QQQs, GOOGL is 4.4% and Apple is more than 10%), the video games sector is also in focus following Activision Blizzard’s results. Shares are down more than 4 percent in the pre-market. Cowen wrote that their core franchises continued to struggle, while Piper in a note ahead of results noted that their "TwitchAdviser" indicated viewership for some of their top games had declined q/q, but an in-line result had still been expected.

ATVI’s peer Electronic Arts is feeling the pain, after getting a downgrade by MKM, which wrote that they were now "less enthusiastic" about the incremental drivers of the stock, calling the initial success of Apex Legends a “head fake.” Piper wrote that the contribution from Apex would likely be offset by the launch of Anthem, which Piper deemed “somewhat disappointing.” Electronic Arts results are due next week.

On Tap for Next Week

The earnings flood has now passed, but that’s not to say the waters will recede -- hundreds of the smaller, non-mega caps are due to report. These smaller names will also be more heavily geared to the U.S. economy, as they tend not to be multinational in nature, providing insight into growth. You also can’t ignore the trade talks issue on a macro scale, which are due to resume next week when Chinese President Xi Jinping’s top trade envoy, Liu He, returning to Washington for what could be a closing round of discussions.

But before you get to wade into those financials, you’ll need to kick back with a mint julep and split screen Saturday with Berkshire’s annual meeting taking place in Nebraska, and the Kentucky Derby. The former is being live streamed (found here), and its likely Buffett will speak on TV at length on Monday.

Also Monday, the Sohn conference gets underway, where commentary from some of the heaviest hedge fund hitters has the potential to move stocks. If you want inspiration, Tim Ferriss will also be speaking, but for our purposes some of the biggest names include Glenview’s Larry Robbins (largest holdings include IQV, FMC, FDA, HCA, DXC), Doubleline’s Gundlach and Greenlight’s Einhorn (largest holdings include GM, GRBK, AER, BHF, CCR).

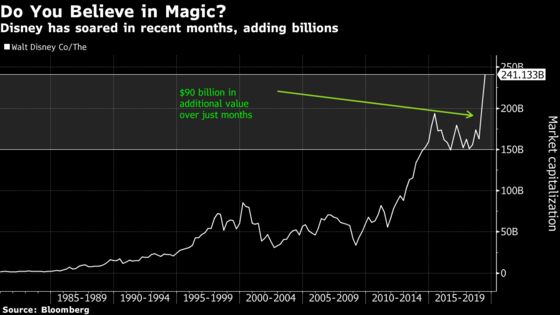

From a larger earnings perspective, Mickey Mouse’s big cheese, Disney, is on the docket -- serving up a certifiable cornucopia of moving targets, be it the details on its smash hit Avengers, its extraordinary share move following the investor meeting in mid April (before the 4-day losing streak through Thursday’s close, the entertainment giant added 40% to its market value over period 4 months--just 0.5% of its history as a public company. Excluding the 4Q meltdown, its up 16% over 5 months), and further details on the new streaming service. JD.com, an e-commerce giant in China, is also due to report (VIPS is a peer), and may provide some insight into the state of play for tech overseas. Results also precede those for the “BATs” -- Baidu, Alibaba and Tencent -- which come the following week.

From a different earnings perspective, we’ll have a few IPO-related names to watch. Tyson Foods, which recently sold out of its Beyond Meat stake (was that stake a “mistake”?) will report, and analysts will likely be chomping at the bit to inquire as to some of the strategic rationale behind that action. Executives may have to answer for it after the substitute meat company staged the best IPO debut since the financial crisis (a rundown can be found here).

Recent IPO and ride-sharing company Lyft is also due to report, nicely coinciding with the week that competitor UBER is set to debut. Its unclear to what extent Lyft could have an impact on the process (given the fact that the business models do not entirely overlap), but a knee jerk reaction to pricing the IPO wouldn’t be out of the question should Lyft shock in some respect.

Sectors in Focus Today

- Recent IPOs remain in focus (LYFT, ZM, PINS, SILK, SWAV) after Beyond Meat’s stunning debut, nearly tripling on day 1. Its higher by another 11% this morning

- Semiconductor manufacturers after UCTT beat on the top and bottom line (watch MKSI, LRCX, KLAC)

- Networking names (CSCO, JNPR) after Arista’s forecast fell short of expectations

- Apple suppliers and peers (SWKS, AVGO, CRUS, QRVO, OLED, MXIM, NXPI) as smartphone supplier OLED soared following their results

- Flooring names (LL, HD, LOW) after FND dropped nearly 20% after missing its forecasts

- Consulting names after CTSH soured the sentiment, cratering INFY, ACN, WIT

- Video games makers as ATVI results disappointed following positive results from Zynga earlier in the week (EA reports next week)

Notes From the Sell Side

Pharmaceutical giant Bristol-Myers is on the receiving end of an upgrade by Barclays this morning, going to overweight from equal-weight as Geoff Meacham weighs in on the Celgene deal he feels has an increasing chance of successfully closing. The combined company “looks attractive” at the current levels, he writes, as he downgrades Celgene given the thesis has “largely” played out. His call is part of a broader idea that fundamentals remain strong following 1Q earnings in the segment and new drugs are in the early innings for the sector.

Fluor’s disaster day on Thursday (closed down 24% in its worst ever performance) has prompted analysts to come out of the woodwork on both sides of the equation. Macquarie now feels the time is right to get long, raising the rating to outperform given where the stock is currently trading. Analyst Sameer Rathod sees “all options on the table" to transform the oil and gas infrastructure construction services provider. Canaccord analysts downgraded the name, and MKM lowered their estimates. MKM’s Daniel Scott sees margin impacts into 2020 and says the company will now be in “prove-it” mode going forward.

Tick-By-Tick to Today’s Actionable Events

- KBR investor conference

- 8:30am -- Fed holds second public meeting on BB&T/SunTrust deal in Atlanta

- 8:30am -- March Prelim. Wholesale Inventories

- 8:30am -- April Change in Nonfarm Payrolls, Change in Mfg Payrolls, Unemployment Rate

- 9:45am -- April Final Markit US Services, Composite PMI

- 10:00am -- April ISM Non-Mfg Index

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.