The Most Momentous Rate Decision This Month Isn’t at Fed or ECB

The Most Momentous Rate Decision This Month Isn’t at Fed or ECB

(Bloomberg) -- Explore what’s moving the global economy in the new season of the Stephanomics podcast. Subscribe via Apple Podcast, Spotify or Pocket Cast.

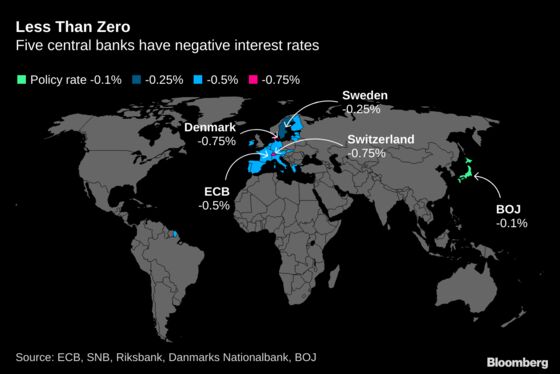

The world’s oldest central bank stands to be the most significant this month as it pioneers a shift away from negative interest rates.

Sweden was among the handful of economies that reduced key interest rates half a decade ago below zero. Now officials at the Riksbank -- founded in 1668 -- insist the policy has done its stimulus work, so their so-called repo rate can stop being negative.

That puts the rich Nordic country in the spotlight of global monetary policy as counterparts watch nervously to see how easy it is for the experiment of subzero rates to be unwound. While the Federal Reserve has firmly resisted U.S. President Donald Trump’s calls to venture into negative territory, officials in the euro zone, as well as Switzerland, Denmark and Japan, all find themselves in the same boat as Sweden.

“A Riksbank hike in December would be a signal that central banks admit that there’s a downside to too-low interest rates,” said Thomas Elofsson, a portfolio manager at Catella in Sweden. “It will be interesting to follow how the SNB and the ECB communicates and acts with this new mindset.”

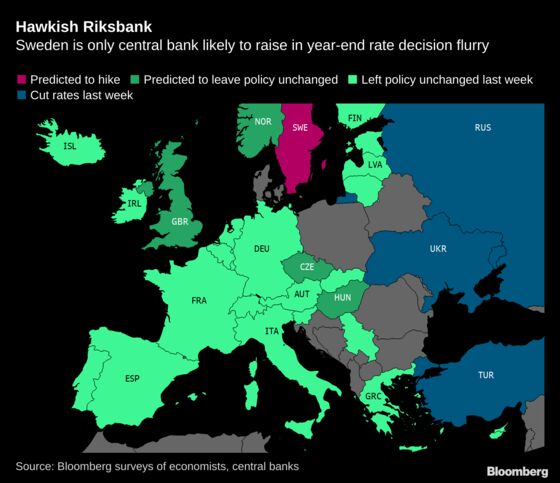

The Riksbank decision on Dec. 19 promises more monetary action than central banks in the U.S. and the euro zone delivered last week. All 16 economists surveyed by Bloomberg predict a quarter-point increase in Sweden’s main policy rate from the current minus 0.25%.

The Fed on Dec. 11 signaled an extended pause, while the next day, Christine Lagarde, at her first press conference as European Central Bank president, emphasized an upcoming review of the institution’s strategy rather than any impending policy moves.

Sweden’s shift is taking place against a global backdrop of worries about the harmful effects of subzero policy. Complaints by banks about profit margins have grown louder, while both the Riksbank and the ECB were among central banks warning last month about the financial stability risks.

A key idea behind subzero policy is that it should stimulate growth by encouraging financial institutions to lend money rather than hoarding it. But ECB officials have noticeably cooled on the measure since they cut their deposit rate further in September to minus 0.5% to shore up a slowing economy. They increasingly cite the harmful effects, even though they’re not yet close to reversing course.

ECB officials “will certainly be watching” said Hetal Mehta, senior economist at Legal & General Investment Management Ltd. in London. “Seeing Sweden come out gradually -- that has some people on the Governing Council hoping the ECB can follow suit. But it’s just going to be a long way away.”

Swiss officials claim that their policy can’t be compared to the Swedes’. Changing rates in Sweden has a “very different macroeconomic effect” because the krona isn’t a haven currency like the franc, SNB President Thomas Jordan said last week in Bern.

The Riksbank’s key rate followed the ECB and the Swiss into negative territory in February 2015. But it took two years, and three additional cuts, to bring inflation up to the 2% target, and another two years for officials to feel confident enough to start venturing back toward zero. Rising consumer prices may have bolstered that view.

What Bloomberg’s Economists Say

“Sweden’s November inflation data accelerated by enough to cement a Riksbank rate hike next week. We expect Governor Stefan Ingves and his colleagues to deliver a quarter point rate increase on Dec. 19 -- leaving negative rates behind after almost five years. After that, interest rates are likely to remain on hold through 2020.”

-Johanna Jeansson. See her SWEDEN REACT and SWEDEN INSIGHT

Quickening inflation has allowed rate setters in Stockholm to argue that the policy has worked. Markus Brunnermeier, a professor at Princeton University who pioneered the notion that negative rates hurt economies at some point, suggests that view is fair.

“It’s very specific to the country -- some can go more negative, some cannot go negative at all,” he said. “If it were counterproductive, then inflation should not have gone up.”

Others may be more skeptical. The best-known critic is former U.S. Treasury Secretary Larry Summers, who signed on to a paper using Swedish data that labeled negative rates “at best irrelevant” and possibly “contractionary.” The Riksbank contested that study.

Summers’s co-author, Brown University’s Gauti Eggertsson, says it’s hard to draw any firm view about the efficacy of the policy, but he’s doubtful.

“We came to the conclusion that the last two cuts did not add much,” he said.

Should Sweden go ahead and hike, it will be doing so just as its export-oriented economy shows signs of slowing amid fallout from the global trade dispute.

That raises the prospect that the move might prove abortive, evoking memories of its heavily criticized tightening that started in 2010, later reversed. Nobel Laureate Paul Krugman derided that policy as “sadomonetarist.” Such a prospect would be poignant too for the ECB, which tried raising a year later, under then-President Jean-Claude Trichet.

Former Swedish policy maker Lars E.O. Svensson says the danger of such an error is real.

“This appears to be a rate normalization of the same kind as in 2010,” he said. In other words, “a similar mistake. But luckily on a smaller scale.”

--With assistance from Love Liman and Zoe Schneeweiss.

To contact the reporters on this story: Catherine Bosley in Zurich at cbosley1@bloomberg.net;Niclas Rolander in Stockholm at nrolander@bloomberg.net

To contact the editors responsible for this story: Fergal O'Brien at fobrien@bloomberg.net, Craig Stirling, Paul Gordon

©2019 Bloomberg L.P.