For First Time in 150 Years, World's Benchmark Bond Is Sub-1%

Following the Federal Reserve’s emergency rate cut, the U.S. 10-year Treasury yield dropped below 1%.

(Bloomberg) -- It is hard to exaggerate the historic significance of Tuesday’s events in the bond market.

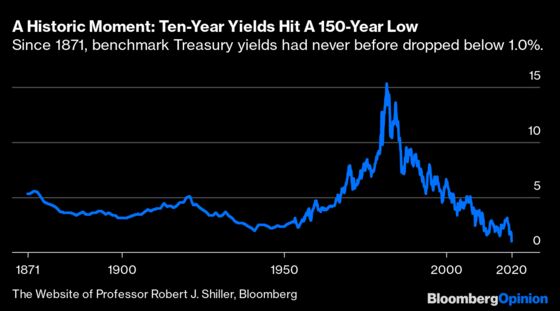

Following the Federal Reserve’s emergency cut to overnight rates, the 10-year Treasury yield — which is taken as the notional “risk-free” benchmark rate for financial transactions across the globe — dropped below 1%. According to historical work by Robert Shiller, the Nobel laureate economist at Yale University who has reconstructed the 10-year interest rates available in the U.S. back to 1871, it has never before dropped this low. Many momentous events have shaken the U.S. since Ulysses S. Grant’s presidency, but none of them were sufficient to drive long-term money down to such cheap levels:

The decision to make an emergency cut was not well-received and appears to have been interpreted by the markets as a measure of desperation. There is little history to guide us, but emergency cuts have in recent history been followed by extreme conditions in capital markets.

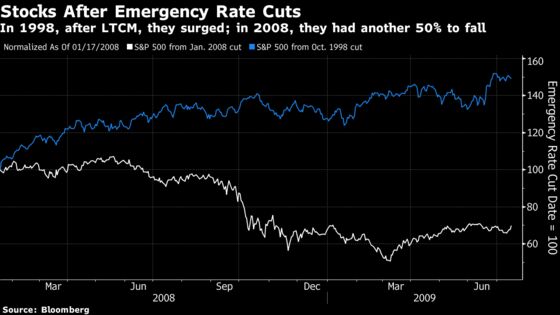

When Alan Greenspan’s Fed made an emergency cut in October 1998, in a bid to revive fixed-income markets after the meltdown of the Long-Term Capital Management hedge fund, the S&P 500 went on to gain 50% over the next 18 months. His cut has since been widely criticized as a mistake that ignited the last extreme phase of the Dot Com Bubble. Meanwhile, the emergency cut in January 2008, as the scale of the global financial crisis began to become apparent, did little or nothing to help the situation. The crisis still happened, and stocks would fall 50% before recovering:

The initial signs for the latest emergency cut are not healthy. Monetary policy cannot directly help with a public-health issue. The intention was to mitigate the financial pressures that might make the economic effect of the coronavirus more severe. The subsequent fall in stock markets suggests that these pressures have not yet been mitigated.

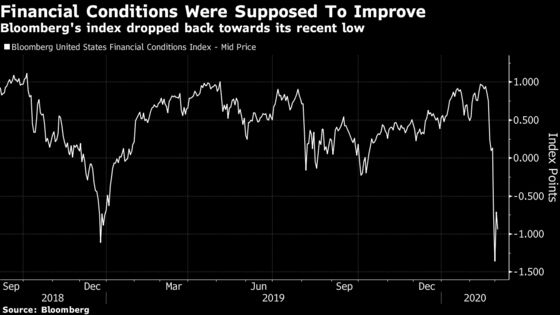

Bloomberg’s financial-conditions index, which combines nine separate measures, fell for the day after a bounce on Monday. It is now back to the low it hit during the panicked conditions of the stock market sell-off on Christmas Eve 2018. The aim would have been to engineer a sharp improvement in conditions.

In the index, figures below zero show tight conditions, while positive numbers show accommodative conditions:

The emergency cut did, however, relieve much upward pressure on the dollar, bringing the gap between similar Treasury and German bund yields back to levels not seen since the summer of 2016. This helped to drive a continued sharp weakening for the dollar — which is in line with the wishes of the U.S. administration. It also intensified the impression that U.S. financial conditions are converging with those of Japan and the euro zone, where low or negative yields have been the norm for a while.

To contact the editor responsible for this story: Melinda Grenier at mgrenier1@bloomberg.net, Jenny Paris

©2020 Bloomberg L.P.