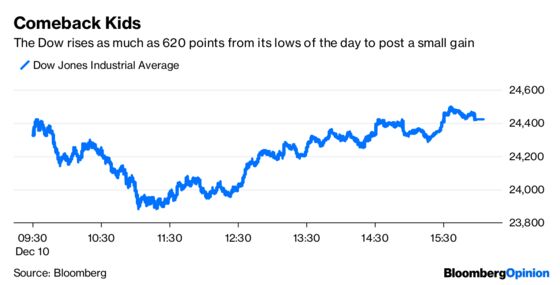

(Bloomberg Opinion) -- Some of the smartest people in the world work on Wall Street, but that doesn’t mean that markets can’t “overshoot.” In other words, the economy is never really as good nor bad as markets suggest, and right now they are sending a pretty dire message. But there’s good reason to think that markets have perhaps tilted too far to the downside after the S&P 500 Index fell almost 2 percent Monday to its lowest since April only to snap back to end little changed.

On a day when there was no shortage of research notes calculating the odds of a recession over the next 12 months, some influential firms went out on a limb to say such mental gymnastics are premature. JPMorgan said the correction in U.S. stocks have “overpriced” risk of a recession, while Goldman Sachs said a rare divergence has opened up between the market’s performance and economic data, according to Bloomberg News’s Lu Wang. The Institute for Supply Management said last week that both its manufacturing and services indexes remained at levels that correlate to strong economic growth. On Monday, a government report showed that the job-openings rate for the durable-goods manufacturing industry reached 4 percent in October, a record in data back to 2000. There are reasons beyond the economic data that should give bulls hope, according to DataTrek Research. For one, the Federal Reserve is sounding less hawkish, suggesting it will not keep hiking interest rates blindly until some notion of “neutral” has been reached. Also, the big drop in Treasury yields over the last month should help support equity valuations. Plus, the dollar has stopped appreciating and has largely moved sideways in the past month, which should help exporters; 37 percent of S&P 500 revenues come from non-U.S. sources.

If anything, Monday’s comeback in equities should be an encouraging sign, especially because it followed the news over the weekend that the escalating trade tension between the U.S. and China isn’t likely to end soon. Perhaps now that the S&P 500 is trading at about 15.4 times forecast earnings as measured by Bloomberg Intelligence, about 7 percent below the average over the past five years, it makes sense to nibble. A survey by Bloomberg News at the end of November found that the average estimate among strategists forecast the S&P 500 to climb to 3,056 by the end of next year, a rise of about 17 percent from recent levels.

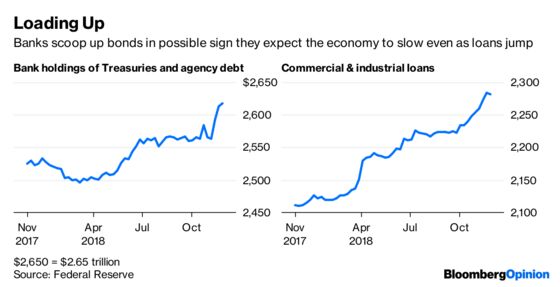

BANKS GORGE ON BONDS

It makes a lot of sense to watch what banks are saying and doing because, more than any other business, they have their fingers on the pulse of the economy. They get to see what corporate America is doing in real time, without waiting for stale government data that is often released with a one- or two-month lag. What’s interesting — or concerning — is that U.S. banks have been loading up on supersafe Treasuries and other government bonds. The latest Fed data released late Friday afternoon showed that banks bought $55.1 billion of such securities in the three weeks ended Nov. 28, bringing their holdings to $2.62 trillion. The increase was the most over a three-week period since mid-2012 and has paid off as yields on Treasuries of all maturities have dropped to an average of 2.80 percent from this year’s high of 3.12 percent on Nov. 8. One way to interpret this is that banks are suddenly more concerned about the economic outlook, that the turbulence in markets of late is more than just a passing blip and feel a better use of their money would be to buy bonds rather than lend it out. Perhaps, but the other side of the argument is that the U.S. is selling more bonds to finance a growing budget deficit, so it makes sense that banks would be stepping up their purchases. The loan data tend to support that notion. Despite a small dip last week, the Fed data also show that outstanding commercial and industrial loans at banks expanded by $27 billion last month to $2.28 trillion. But that increase may just reflect the closing of loan commitments made months earlier, which makes the data in coming weeks all the more important.

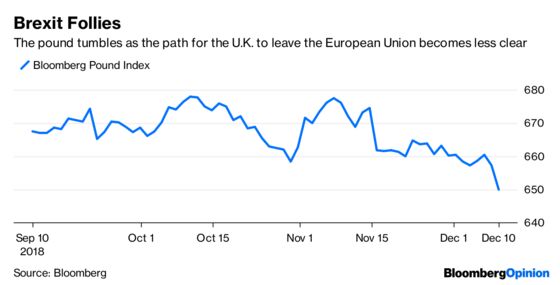

CHAOS RULES THE POUND

Those who say politics don’t matter when it comes to markets haven’t been paying attention to the U.K., where it’s nothing short of chaos. Faced with a humiliating defeat on her Brexit deal, embattled U.K. Prime Minister Theresa May announced to the House of Commons she would defer a vote and return to Brussels to seek “assurances” from European Union leaders. The Bloomberg Pound Index, which measures sterling against its chief peers promptly sank as much as 1.61 percent to its lowest level since the start of 2017. The drop in sterling has all sorts of implications for the U.K. Although the political chaos has investors tamping down their bets for future interest-rate hikes by the Bank of England, which lifted the U.K. bond market Monday, the longer-term concern is that the rapidly falling pound may dissuade foreign investors from putting money to work in the U.K. After all, who wants to own assets in a depreciating currency? Any drop in demand for bonds from foreign investors could push up borrowing costs in the U.K. regardless of what the BOE does with rates. “The market clearly believes she will not get anything material enough from the EU to turn that scale of opposition around, so even if the vote is delayed it’s going to end in the same way — with a big defeat for the government,” John Wraith, head of U.K. macro rates at UBS Group AG, told Bloomberg News in reference to May.

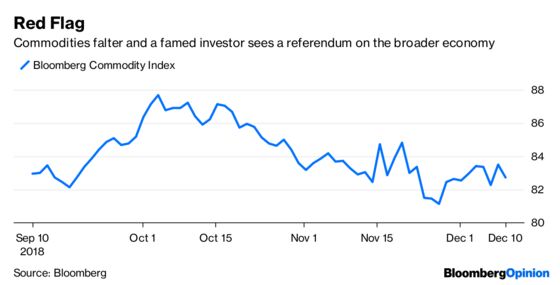

COMMODITIES SIGNALS WORSEN

Paul Tudor Jones is one of those legendary figures on Wall Street. He has a fortune that the Bloomberg Billionaires Index puts at $3.3 billion. That all started in 1976 in the pits of the New York commodity exchanges. So when Jones says, as he did Monday, that the commodities “are a great leading indicator,” it pays to listen. The Bloomberg Commodity Index of 22 raw materials fell on Monday, bringing its loss since early October to a bit more than 5 percent. It was just a couple of weeks ago that the gauge closed at its lowest level since mid-2017. Yes, oil and other energy-related commodities have led the charge lower, but other key raw materials such as copper and aluminum are down as well. For this reason, and the resulting deflationary pressures, Jones told CNBC that he doesn’t think the Fed will boost interest rates in 2019. Oil slipped on Monday despite last week’s agreement among OPEC and its allies to cut output. To many, the decline in oil to about $51.50 a barrel on Monday from almost $77 in early October reflects diminished global demand, which is a down arrow for the economy and speaks to Jones’s concern. As for copper, it extended a two-week slide on Monday as China’s monthly imports fell in November from a year earlier for the first time in 2018.

THERE’S A JOB OPENING IN INDIA

India has been at the forefront of the relative strength in emerging markets, which have held up admirably even as developed-market equities and currencies tank. India’s benchmark Sensex index of equities rose 6.97 percent between late October and the end of last week, compared with a 4.45 percent gain for the MSCI Emerging Markets Index. From early October through last week, the rupee appreciated 5.06 percent, compared with 1.52 percent for the MSCI EM currency index. As one of those nations that is dependent on imported oil for its energy needs, the big drop in crude has certainly added to the brighter outlook in India. But some new developments Monday threaten to overshadow the benefits from lower oil prices going forward. Both the Sensex and rupee fell in some of the biggest moves in emerging markets after Reserve Bank of India Governor Urjit Patel quit unexpectedly. Although Patel cited personal reasons for the decision, some investors took the news as evidence of a new fissure in the RBI’s relationship with Prime Minister Narendra Modi’s government. “Our immediate concern is that if the resignation was influenced by the government’s interference with the central bank’s independence, it would obviously have very damaging consequences for RBI’s credibility,” said Anders Faergemann, a fund manager at PineBridge Investments. Traders were already reeling from state exit polls that showed Modi’s Bharatiya Janata Party facing a tight contest, sending Indian shares to their worst session in two months.

TEA LEAVES

There’s been no shortage of reasons for the pressure on stocks the last couple of months. One of those at the top of the list is the prospect of slower corporate earnings growth, which includes shrinking profit margins as wages and other input costs rise. But on Tuesday, there may be talk of such concerns being overblown. That’s when the government releases its monthly Producer Price Index report. This measure of what companies pay for goods has been hovering around its highest levels since 2011 all year. In the last month, however, some key input costs such as oil have declined. As such, the report is forecast to show that producer prices rose 2.5 percent in November from a year earlier, compared with 2.9 percent in October and matching the smallest increase since last December. To be clear, this report will have no bearing on whether the Fed raises interest rates when policy makers next week, but at least equity investors may be able to breathe a sigh of relief.

DON’T MISS

Fed Gets Pulled in Different Directions: Mohamed A. El-Erian

Wall Street Needs More Market Indexes. Seriously: Eric Balchunas

May’s Delay Reveals a Government in Name Only: Therese Raphael

Tying Infrastructure to Pensions Is Too Much: Brian Chappatta

India's Bank Governor Goes Far Too Quietly: Andy Mukherjee

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.